Global KYC & AML Regulations Part 2: What Regulators Expect | Bureau

Global KYC & AML Regulations Part 2: What Regulators Expect | Bureau

Global KYC & AML Regulations Part 2: What Regulators Expect | Bureau

Translate global KYC and AML regulatory expectations into practical controls by aligning fraud risk management with compliance programs. - Part 2

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

The post “Global KYC and AML Regulations: Part 1 - What Regulators Really Expect” of this 2-part blog series, explored how global regulators are shifting from procedural compliance to outcome-driven supervision. It explained how and why traditional KYC and AML approaches increasingly fall short.

Part 2 below, focuses on execution. It attempts to translate regulatory direction into practical best practices. It also discusses how leading institutions are aligning KYC, AML, fraud risk management (FRM), and device intelligence to execute proactive controls.

Fraud, account takeover, mule activity, and identity abuse follow almost similar patterns around the world. What changes is the speed at which those patterns emerge and the regulatory context within which businesses operate.

Regulatory language varies by geography. Risk does not.

Fraud adapts faster than regulation. It exploits gaps between onboarding and monitoring, between channels, and even between teams. Therefore, for institutions that treat KYC, AML, and fraud as separate functions, the chances of finding gaps is an uphill task.

Regional regulatory expectations and risk priorities

Regional regulatory expectations and risk priorities differ across major regions. These include:

India

India has context-aware risk-based controls. The regularity emphasis is on three major points:

Risk-based authentication

Transaction-level scrutiny

Reduced friction for low-risk users

Also, Indian regulators increasingly expect businesses to differentiate between low-risk and high-risk activity in real time, instead of relying on uniform controls.

Related Read: Risk-Based Authentication: How Can It Help Your Business?

There are several factors that have led to this regulatory stance. In India, the population exhibits several common traits such as:

SIM recycling and rapid number churn

Device sharing across individuals

Layered mule activity spanning accounts and apps

This makes static KYC insufficient to capture fraud complexity. Without device intelligence and behavioral context, businesses struggle to distinguish legitimate reuse from coordinated abuse. Identity assurance must, therefore, extend beyond documents to ongoing context.

Southeast Asia

One of the key traits of Southeast Asia is its rapid fintech adoption. However, it also suffers from inconsistent identity standards across countries. As a result it has high exposure to organized mule networks.

The current regulatory direction focuses on building stronger onboarding controls and putting in place stringent post-onboarding monitoring.

Related Read: What is a money mule?

In SEA markets, regulators increasingly recognize that identity verification at entry is necessary, but also insufficient. Risk commonly occurs way past the onboarding stage, as accounts are repurposed or recruited into fraud networks.

Financial institutions that want to win must focus on risk continuity: connecting identity signals across sessions, devices, and behaviors as users move quickly across platforms.

Middle East

The Middle East attracts a huge population of immigrants seeking employment opportunities in its developing real estate and energy sector. As a result, most of its risk exposure revolves around:

Cross-border payments and remittances

New digital rails and real-time settlement

Expanding attack surface tied to rapid digitization

Also, the Middle East has a progressive stance towards adopting AML frameworks.

As financial infrastructure modernizes, regulators expect risk controls to improve with it. Businesses are under pressure to demonstrate that faster payments and broader access do not come at the cost of increased financial crime exposure.

European Union

In the EU, effectiveness alone is not enough. Businesses must show how decisions are made, why certain signals were used, and how customer rights are respected throughout the process.

The regulatory environment has strong data protection requirements and zero tolerance for opaque or non-explainable decisions. Violations of GDPR can attract hefty penalties, such as in 2023, when approximately €2.1 billion in fines were imposed.

Region | Regulatory Focus | Primary Risk Drivers | Supervisory Expectations | Control Implications |

India | Context-aware, risk-tiered controls | Device reuse, SIM churn, mule layering | Real-time risk differentiation; adaptive controls | Continuous authentication, behavioral and device intelligence |

Southeast Asia | Identity continuity at scale | Fragmented ID systems, organized mule networks | Strong onboarding plus persistent monitoring | Cross-session identity linking and post-onboarding surveillance |

Middle East | Secure modernization of financial rails | Cross-border flows, rapid digitization | Crime controls that scale with payment speed and access | Real-time transaction monitoring and cross-border risk visibility |

European Union | Privacy, explainability, and accountability | Data misuse, opaque automation | Transparent, auditable decision-making | Explainable models, strict data governance, rights-preserving controls |

Best practices for KYC, AML, and FRM to adopt in 2026-27

Across regions, regulators are converging on the common principle that risk controls must be adaptive, continuous, and accountable.

How can businesses embrace these values for better KYC, AML, and FRM? These best practices show the way:

Move from document checks to identity assurance

Checklists confirm the existence of controls. Unfortunately, they do not confirm control.

Modern identity assurance treats trust as an ongoing state, not a one-time event. It continuously evaluates whether the same legitimate user remains in control of the account across sessions, devices, and behaviors.

This shift is critical for detecting account takeover, mule reuse, and synthetic identity abuse that documents alone cannot reveal.

Treat device intelligence as a first-class signal

Device intelligence is particularly necessary in environments where credentials are easily compromised or shared.

Devices carry more truth than credentials. They reveal certain traits that can be used to reveal underlying fraud patterns.

Often, without realizing, most users reveal:

Stability over time

Ownership patterns

Signs of manipulation or spoofing

Tracking and observing these signals are critical to identifying fraud signals before they snowball into full-sized catastrophes.

Use behavior to detect intent early

Fraud intent starts appearing way before fraud transactions happen. There are specific behavioral signals that, combined together, can help anticipate risk. These include:

Navigation patterns

Interaction timing

Environmental anomalies

These signals operate independently of transaction monitoring and provide an early-warning layer that traditional AML systems miss.

Connect identity across sessions and channels

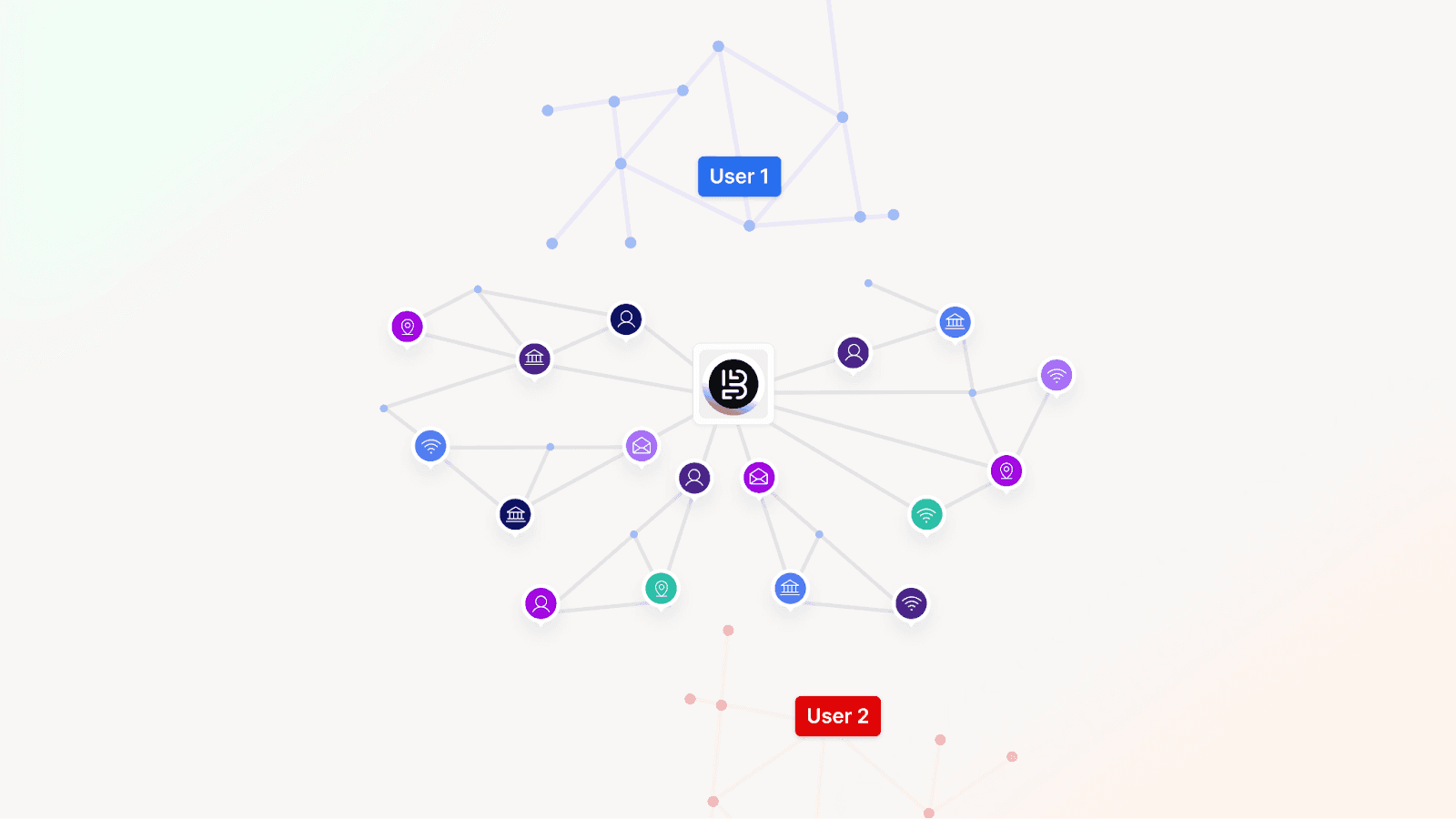

Fraud rarely happens in isolation. It is usually orchestrated as part of a bigger plan, a sequence of events, and interdependent factors.

Attackers reuse devices, rotate credentials, and distribute activity across accounts and channels. Businesses that evaluate risk one session or one transaction at a time, miss the bigger picture.

Network-level intelligence which connects identities across time and touchpoints is far more effective than evaluating individuals in silos.

Reduce reliance on static rules

Static thresholds create blind spots, especially as attackers learn to operate just below them. Over time, rules accumulate, alerts increase, and effectiveness declines.

Modern risk programs rely on adaptive signals and decisioning frameworks that evolve with behavior, rather than chasing it.

Build explainable, auditable risk decisions

When fraud is discovered, knowing the cause and effect is insufficient. Businesses must dig deeper to understand the reason behind the fraud.

Unearthing the “why” behind the fraud will prove helpful in:

Regulatory audits

Internal governance

Cross-team trust

Clear decision flow such as the signals used, logic applied, outcome reached, and so forth, turns advanced risk intelligence into something regulators and executives can actually stand behind.

Related Read: Why the Future of Financial Crime Prevention Is Collaborative

Shift teams from alert handling to risk prevention

Smart security teams reduce operational burden by preventing risk earlier, rather than reacting to it later. This allows them to focus on control design, risk analysis, and continuous improvement, instead of manual firefighting.

The way forward: From compliance to confidence

KYC and AML remain essential foundations of trust and compliance. However, fraud risk management is the true differentiator.

Businesses that unify identity, device, behavior, and transaction intelligence move beyond just compliance to active risk prevention. They operate with the assurance that controls are effective, decisions are defensible, and customers are protected without unnecessary friction.

Modern risk management isn’t about more checks. It’s about making better decisions earlier, and with confidence.

Where Bureau fits in this FRM evolution

Bureau is built for businesses navigating the shift from procedural compliance to continuous, outcome-driven risk management. It acts as a unifying risk intelligence layer that connects identity, device, behavior, and transaction signals across the customer lifecycle.

By enabling context-aware decisioning, network-level visibility, and explainable risk outcomes, Bureau helps teams operationalize modern KYC, AML, and FRM principles without adding friction or complexity.

Move Beyond Compliance. Operate with Confidence.Discover how modern KYC, AML, and fraud risk teams are building adaptive, explainable, and continuous risk controls with Bureau. |

The post “Global KYC and AML Regulations: Part 1 - What Regulators Really Expect” of this 2-part blog series, explored how global regulators are shifting from procedural compliance to outcome-driven supervision. It explained how and why traditional KYC and AML approaches increasingly fall short.

Part 2 below, focuses on execution. It attempts to translate regulatory direction into practical best practices. It also discusses how leading institutions are aligning KYC, AML, fraud risk management (FRM), and device intelligence to execute proactive controls.

Fraud, account takeover, mule activity, and identity abuse follow almost similar patterns around the world. What changes is the speed at which those patterns emerge and the regulatory context within which businesses operate.

Regulatory language varies by geography. Risk does not.

Fraud adapts faster than regulation. It exploits gaps between onboarding and monitoring, between channels, and even between teams. Therefore, for institutions that treat KYC, AML, and fraud as separate functions, the chances of finding gaps is an uphill task.

Regional regulatory expectations and risk priorities

Regional regulatory expectations and risk priorities differ across major regions. These include:

India

India has context-aware risk-based controls. The regularity emphasis is on three major points:

Risk-based authentication

Transaction-level scrutiny

Reduced friction for low-risk users

Also, Indian regulators increasingly expect businesses to differentiate between low-risk and high-risk activity in real time, instead of relying on uniform controls.

Related Read: Risk-Based Authentication: How Can It Help Your Business?

There are several factors that have led to this regulatory stance. In India, the population exhibits several common traits such as:

SIM recycling and rapid number churn

Device sharing across individuals

Layered mule activity spanning accounts and apps

This makes static KYC insufficient to capture fraud complexity. Without device intelligence and behavioral context, businesses struggle to distinguish legitimate reuse from coordinated abuse. Identity assurance must, therefore, extend beyond documents to ongoing context.

Southeast Asia

One of the key traits of Southeast Asia is its rapid fintech adoption. However, it also suffers from inconsistent identity standards across countries. As a result it has high exposure to organized mule networks.

The current regulatory direction focuses on building stronger onboarding controls and putting in place stringent post-onboarding monitoring.

Related Read: What is a money mule?

In SEA markets, regulators increasingly recognize that identity verification at entry is necessary, but also insufficient. Risk commonly occurs way past the onboarding stage, as accounts are repurposed or recruited into fraud networks.

Financial institutions that want to win must focus on risk continuity: connecting identity signals across sessions, devices, and behaviors as users move quickly across platforms.

Middle East

The Middle East attracts a huge population of immigrants seeking employment opportunities in its developing real estate and energy sector. As a result, most of its risk exposure revolves around:

Cross-border payments and remittances

New digital rails and real-time settlement

Expanding attack surface tied to rapid digitization

Also, the Middle East has a progressive stance towards adopting AML frameworks.

As financial infrastructure modernizes, regulators expect risk controls to improve with it. Businesses are under pressure to demonstrate that faster payments and broader access do not come at the cost of increased financial crime exposure.

European Union

In the EU, effectiveness alone is not enough. Businesses must show how decisions are made, why certain signals were used, and how customer rights are respected throughout the process.

The regulatory environment has strong data protection requirements and zero tolerance for opaque or non-explainable decisions. Violations of GDPR can attract hefty penalties, such as in 2023, when approximately €2.1 billion in fines were imposed.

Region | Regulatory Focus | Primary Risk Drivers | Supervisory Expectations | Control Implications |

India | Context-aware, risk-tiered controls | Device reuse, SIM churn, mule layering | Real-time risk differentiation; adaptive controls | Continuous authentication, behavioral and device intelligence |

Southeast Asia | Identity continuity at scale | Fragmented ID systems, organized mule networks | Strong onboarding plus persistent monitoring | Cross-session identity linking and post-onboarding surveillance |

Middle East | Secure modernization of financial rails | Cross-border flows, rapid digitization | Crime controls that scale with payment speed and access | Real-time transaction monitoring and cross-border risk visibility |

European Union | Privacy, explainability, and accountability | Data misuse, opaque automation | Transparent, auditable decision-making | Explainable models, strict data governance, rights-preserving controls |

Best practices for KYC, AML, and FRM to adopt in 2026-27

Across regions, regulators are converging on the common principle that risk controls must be adaptive, continuous, and accountable.

How can businesses embrace these values for better KYC, AML, and FRM? These best practices show the way:

Move from document checks to identity assurance

Checklists confirm the existence of controls. Unfortunately, they do not confirm control.

Modern identity assurance treats trust as an ongoing state, not a one-time event. It continuously evaluates whether the same legitimate user remains in control of the account across sessions, devices, and behaviors.

This shift is critical for detecting account takeover, mule reuse, and synthetic identity abuse that documents alone cannot reveal.

Treat device intelligence as a first-class signal

Device intelligence is particularly necessary in environments where credentials are easily compromised or shared.

Devices carry more truth than credentials. They reveal certain traits that can be used to reveal underlying fraud patterns.

Often, without realizing, most users reveal:

Stability over time

Ownership patterns

Signs of manipulation or spoofing

Tracking and observing these signals are critical to identifying fraud signals before they snowball into full-sized catastrophes.

Use behavior to detect intent early

Fraud intent starts appearing way before fraud transactions happen. There are specific behavioral signals that, combined together, can help anticipate risk. These include:

Navigation patterns

Interaction timing

Environmental anomalies

These signals operate independently of transaction monitoring and provide an early-warning layer that traditional AML systems miss.

Connect identity across sessions and channels

Fraud rarely happens in isolation. It is usually orchestrated as part of a bigger plan, a sequence of events, and interdependent factors.

Attackers reuse devices, rotate credentials, and distribute activity across accounts and channels. Businesses that evaluate risk one session or one transaction at a time, miss the bigger picture.

Network-level intelligence which connects identities across time and touchpoints is far more effective than evaluating individuals in silos.

Reduce reliance on static rules

Static thresholds create blind spots, especially as attackers learn to operate just below them. Over time, rules accumulate, alerts increase, and effectiveness declines.

Modern risk programs rely on adaptive signals and decisioning frameworks that evolve with behavior, rather than chasing it.

Build explainable, auditable risk decisions

When fraud is discovered, knowing the cause and effect is insufficient. Businesses must dig deeper to understand the reason behind the fraud.

Unearthing the “why” behind the fraud will prove helpful in:

Regulatory audits

Internal governance

Cross-team trust

Clear decision flow such as the signals used, logic applied, outcome reached, and so forth, turns advanced risk intelligence into something regulators and executives can actually stand behind.

Related Read: Why the Future of Financial Crime Prevention Is Collaborative

Shift teams from alert handling to risk prevention

Smart security teams reduce operational burden by preventing risk earlier, rather than reacting to it later. This allows them to focus on control design, risk analysis, and continuous improvement, instead of manual firefighting.

The way forward: From compliance to confidence

KYC and AML remain essential foundations of trust and compliance. However, fraud risk management is the true differentiator.

Businesses that unify identity, device, behavior, and transaction intelligence move beyond just compliance to active risk prevention. They operate with the assurance that controls are effective, decisions are defensible, and customers are protected without unnecessary friction.

Modern risk management isn’t about more checks. It’s about making better decisions earlier, and with confidence.

Where Bureau fits in this FRM evolution

Bureau is built for businesses navigating the shift from procedural compliance to continuous, outcome-driven risk management. It acts as a unifying risk intelligence layer that connects identity, device, behavior, and transaction signals across the customer lifecycle.

By enabling context-aware decisioning, network-level visibility, and explainable risk outcomes, Bureau helps teams operationalize modern KYC, AML, and FRM principles without adding friction or complexity.

Move Beyond Compliance. Operate with Confidence.Discover how modern KYC, AML, and fraud risk teams are building adaptive, explainable, and continuous risk controls with Bureau. |

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.