8 Best IDfy Competitors for KYC and Fraud Prevention, and Risk Decisioning

8 Best IDfy Competitors for KYC and Fraud Prevention, and Risk Decisioning

8 Best IDfy Competitors for KYC and Fraud Prevention, and Risk Decisioning

Compare the top IDfy competitors for KYC, onboarding, fraud detection, KYB, AML screening, and identity verification workflows in 2026.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

While IDfy is a widely used platform for KYC, document verification, and compliance-led onboarding, evolving fraud patterns are exposing gaps around fraud intelligence, real-time decisioning, device signals, workflow flexibility, and lifecycle risk visibility.

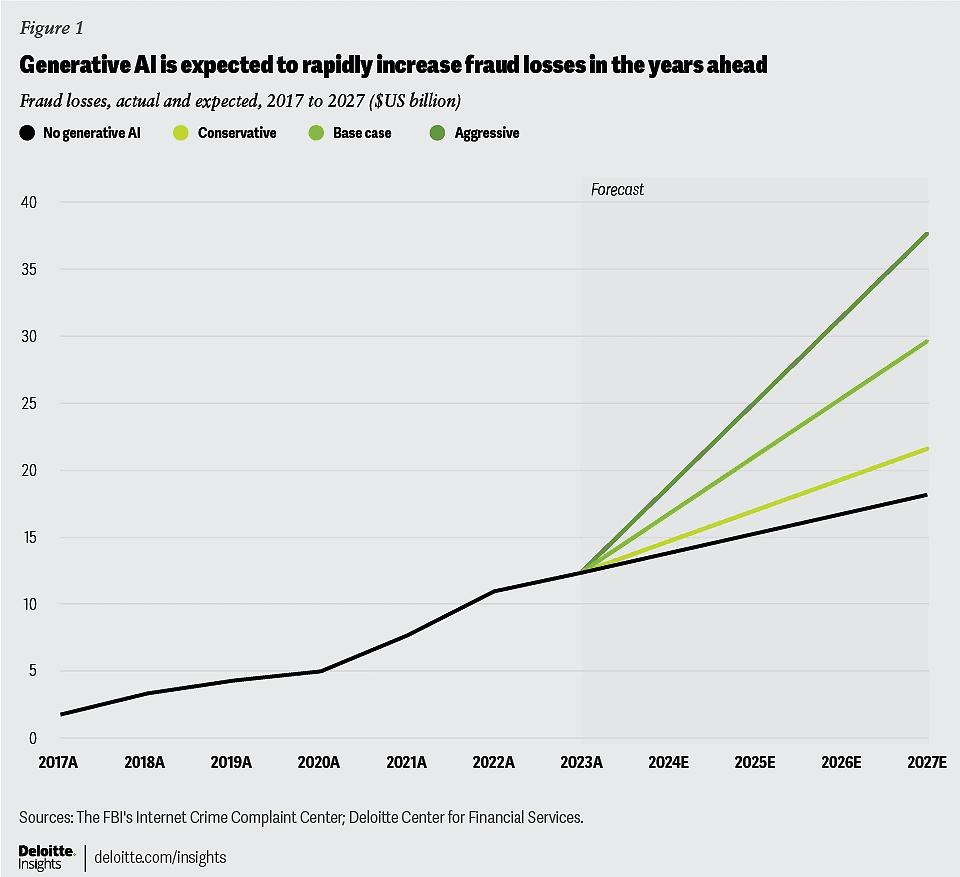

Deloitte’s Center for Financial Services predicts that generative AI could drive fraud losses in the United States from $12.3 billion in 2023 to $40 billion by 2027.

Image Source: Deloitte Center for Financial Services

That makes verification insufficient for high-volume onboarding environments, pushing fintechs, NBFCs, marketplaces, and digital platforms toward IDfy competitors that can evaluate identity, behavior, devices, and risk signals together instead of relying only on static verification checks.

Teams are looking for stronger fraud controls, fewer disconnected vendors, more flexible orchestration, across onboarding, transaction monitoring, AML, device & behavioural signals, and network-level fraud protection.

In this guide, we’ll compare the top IDfy competitors and alternatives for 2026, helping you understand where each platform fits best, which tools are stronger for fraud prevention or onboarding workflows, and what to evaluate before choosing a solution for your fintech or BFSI stack.

Quick Comparison: Best IDfy Alternatives Compared

The best IDfy competitors include identity verification and digital KYC platforms that help businesses automate onboarding, verify users, and prevent fraud across the customer lifecycle.

The right choice depends on whether your team needs stronger fraud intelligence, global identity coverage, stronger KYC workflows, background verification, or government-backed identity checks.

Tool | Best for | Core strength | Fraud capability | Workflow flexibility | Pricing model |

Bureau ID | Unified risk decisioning + network fraud prevention | Identity + fraud + device + behavior | High | High | Platform-based |

Sumsub | Global KYC and AML | Cross-border compliance | Moderate | High | Subscription |

Entrust IDV | Global remote onboarding | Document and biometric AI | Moderate | Moderate | API-based |

Veriff | International verification | Video KYC and fraud signals | Moderate | High | API-based |

HyperVerge | India BFSI onboarding | Face recognition accuracy | Moderate | Moderate | API-based |

Signzy | BFSI automation | AI-driven KYC and KYB | Moderate | High | Subscription |

Perfios KARZA | Lending workflows | Financial data aggregation | Low | Moderate | API-based |

AuthBridge | Background checks | Employee verification | Low | Low | Enterprise |

Each platform solves a different part of onboarding and risk management. Use this table as a first-pass shortlist, then evaluate each tool based on your fraud exposure, compliance needs, onboarding volume, and internal workflow complexity.

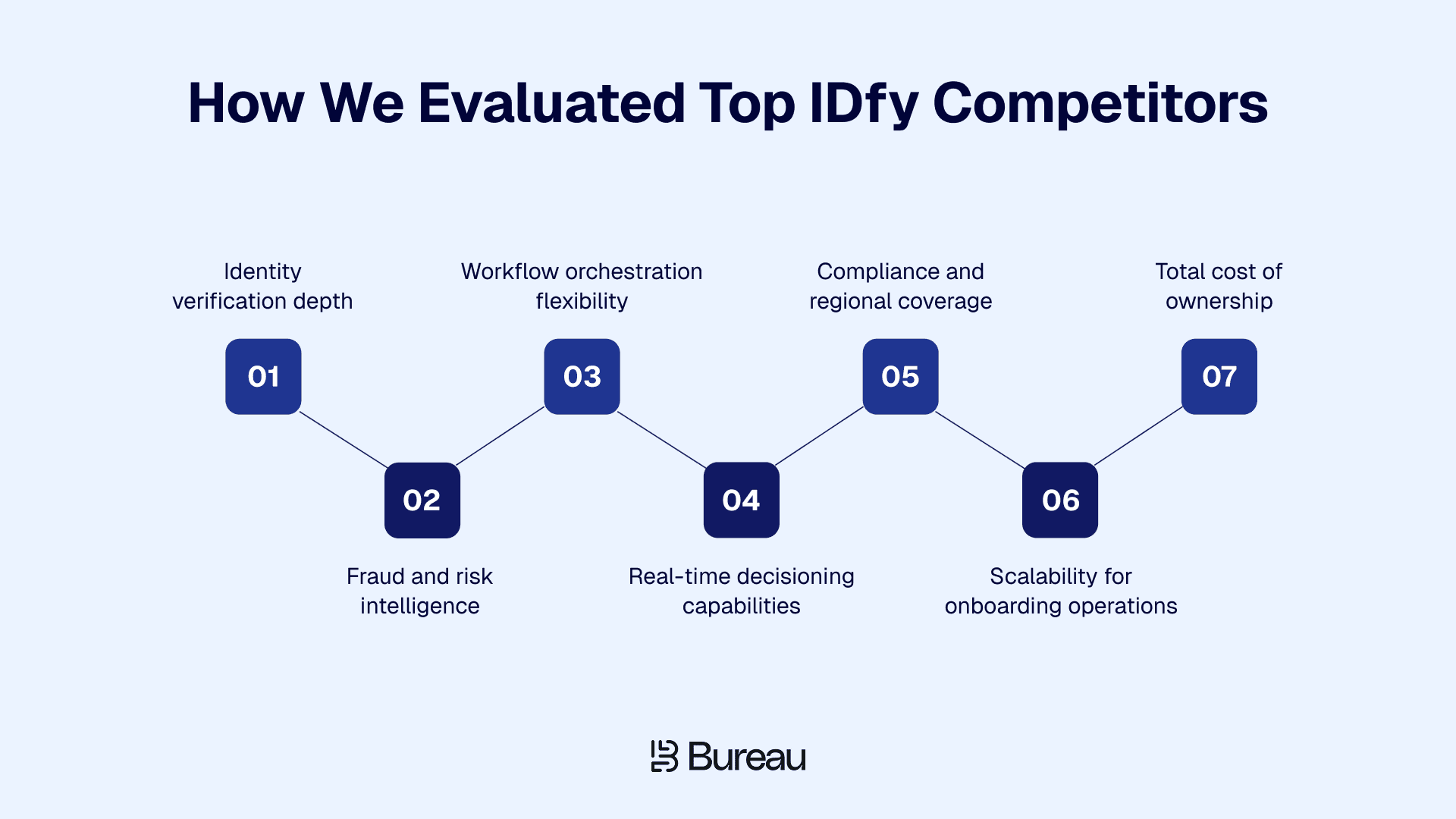

How We Evaluated Top IDfy Competitors

This evaluation focuses on what matters when teams replace or extend a verification platform. Fintech professionals highlighted issues such as rising onboarding friction, growing alert fatigue, synthetic identity fraud, and the operational complexity created by disconnected KYC, AML, and fraud workflows.

In fact, Bureau ID’s UK and EU Fraud Report also found that synthetic identity fraud increased by 50%, while digital fraud attempts across the EU rose 43%, highlighting how onboarding fraud is shifting beyond static document verification into coordinated identity, device, and behavioral attacks.

That is why we looked at how these platforms perform in onboarding environments, not feature lists built around marketing claims.

We evaluated each platform across the following criteria:

Identity verification depth: Support for document verification, biometrics, OCR accuracy, liveness detection, and Video KYC across onboarding workflows.

Fraud and risk intelligence: Coverage for device signals, behavioral analytics, fraud-ring detection, synthetic identity prevention, and adaptive risk scoring capabilities.

Workflow orchestration flexibility: Ability to configure onboarding rules, automate reviews, and reduce engineering dependency through APIs or no-code workflows.

Real-time decisioning capabilities: Support for evaluating onboarding, login, and transaction risks instantly instead of relying only on static verification checks.

Compliance and regional coverage: Strength across Indian KYC regulations, Aadhaar-linked workflows, AML checks, and international onboarding requirements.

Scalability for onboarding operations: Performance under high onboarding volumes, operational complexity, and fraud-heavy environments like fintech, gaming, and marketplaces.

Total cost of ownership: Impact of pricing models, engineering effort, operational overhead, and the need for multiple supporting fraud vendors.

This framework reflects how teams increasingly want unified onboarding and fraud decisioning instead of stitching together separate verification, AML, and fraud-prevention tools across the customer lifecycle.

8 Best IDfy Competitors and Alternatives

1. Bureau ID

Bureau ID approaches onboarding and fraud prevention differently from traditional verification-first platforms. Instead of treating identity verification as a standalone compliance step, it combines identity, fraud, device intelligence, behavioral analytics, and real-time risk decisioning within a single orchestration layer.

The platform continuously evaluates trust across onboarding, authentication, and transaction events instead of relying only on static document checks. As onboarding volumes grow, teams often add separate tools for device intelligence, AML, behavioral analytics, and workflow orchestration, which increases complexity without giving them a clear risk view.

Bureau ID positions itself as a unified decisioning platform designed to reduce that vendor sprawl while helping teams make faster, more explainable onboarding and fraud decisions.

Why choose Bureau ID:

Reduce onboarding fraud earlier: Combines identity verification, device intelligence, and behavioral signals to catch suspicious users before account creation completes.

Consolidate fragmented onboarding systems: Replaces multiple fraud, AML, and verification vendors through a single orchestration and decisioning platform integration.

Improve onboarding speed at scale: Uses real-time risk scoring and automated workflows to reduce manual reviews for genuine users significantly.

Detect fraud rings more effectively: Uses a Graph Identity Network with 500M+ linked identities, devices, and behavioral relationships across ecosystems.

Reduce engineering dependency: Supports no-code workflow orchestration so product and risk teams can adapt onboarding rules independently.

Support global compliance workflows: Combines KYC, KYB, AML, onboarding, and fraud decisioning across 195+ international markets from one platform.

Many teams evaluate Bureau ID after they hit the limits of a verification-first setup. KYC checks may pass, but mule accounts, promo abuse, synthetic identities, and coordinated fraud rings still create losses after onboarding. Bureau solves this by connecting identity, device, behavior, network, and transaction signals in one decisioning layer.

What changes after adoption:

Faster onboarding for genuine users with fewer unnecessary manual reviews

Unified visibility across identity, device, behavioral, and transaction-level risk signals

Real-time onboarding and fraud decisions instead of delayed operational reviews

Lower fraud losses through graph-based fraud detection and persistent device intelligence

Reduced operational complexity by consolidating multiple onboarding and fraud vendors

Less engineering overhead through configurable no-code workflow orchestration

Bureau ID also includes several AI-driven fraud and decisioning capabilities that extend beyond traditional identity verification workflows. These capabilities help businesses evaluate user trust continuously instead of relying only on one-time onboarding checks.

AI and decisioning capabilities:

Graph Identity Network: Maps relationships between identities, devices, accounts, and behaviors to uncover coordinated fraud activity at scale.

Behavioral biometrics: Monitors typing patterns, gestures, touchscreen behavior, and interaction anomalies to identify bots and fraud farms.

Persistent device intelligence: Detects spoofed devices, emulators, VPN usage, and repeated fraud attempts even after factory resets.

Real-time explainable risk scoring: Delivers risk decisions in milliseconds with visibility into the underlying fraud and behavioral signals.

Adaptive onboarding workflows: Configures onboarding, AML, KYB, and fraud rules dynamically by geography, product, and user-risk profile.

Together, these capabilities make Bureau ID a strong fit for businesses trying to balance onboarding speed, fraud prevention, compliance, and operational efficiency within a single platform instead of managing disconnected systems across the customer lifecycle.

Real outcomes: How Bureau ID improved fraud prevention for a food delivery platform

One food delivery platform struggled with coordinated fraud rings abusing promotions and onboarding incentives across thousands of fake accounts. The company relied on fragmented onboarding and fraud systems, which made it difficult to identify linked fraud behavior in real time while maintaining a smooth onboarding experience for genuine users.

Bureau ID implemented unified onboarding and fraud decisioning using device intelligence, behavioral biometrics, graph-based identity analysis, and real-time risk scoring. The company also used configurable workflows to automate fraud reviews and reduce operational dependency on manual investigations.

Results:

Mapped and blocked a 2,700+ user fraud ring operating across 150 connected devices

Removed 1,750+ fraudulent accounts linked to just 3 devices, eliminating major abuse vectors

Flagged 97% of collusive users with high-risk scores for deeper investigation

Blocked repeat offenders through persistent device and behavioral intelligence, helping strengthen long-term fraud protection

Read the full case study here → A Food Delivery Company Eliminates a 2,700-User Fraud Ring

Bureau ID is best for fintechs, NBFCs, marketplaces, gaming platforms, and digital businesses operating in high-risk onboarding environments. Although Bureau ID comes at a higher price point than verification-only tools, its broader feature set and full-lifecycle fraud coverage can make it a stronger long-term investment for businesses managing complex onboarding, fraud prevention, AML, and risk decisioning workflows.

If your team is evaluating how to reduce vendor sprawl while improving onboarding speed and fraud detection together, book a 30-minute demo with Bureau ID to learn how it fits into your current risk and onboarding stack.

2. Sumsub

Sumsub is a global identity verification and compliance platform focused on KYC, KYB, AML screening, and cross-border onboarding. The platform is widely used by fintechs, crypto companies, and digital businesses operating across multiple geographies. Its strength lies in helping teams manage regional compliance workflows from one centralized system while supporting large-scale international onboarding operations.

Teams use Sumsub for global onboarding, identity verification, AML screening, and multi-country compliance management.

Why choose Sumsub:

Expand into global markets faster: Supports identity verification workflows across 220+ countries and territories through one onboarding platform.

Simplify AML and sanctions compliance: Combines KYC, KYB, sanctions screening, and PEP monitoring within a unified compliance workflow.

Reduce operational complexity across regions: Allows teams to configure onboarding flows by geography, regulation, and user-risk profile.

Improve onboarding scalability: Supports automated verification workflows that reduce manual review requirements for international onboarding teams.

Support crypto and high-risk industries: Offers strong regulatory coverage for fintech, crypto, trading, and digital financial services environments.

While Sumsub handles international compliance and onboarding particularly well, there are a few practical considerations worth evaluating before implementation.

India-specific Aadhaar and DigiLocker workflows are less mature compared to India-native onboarding platforms

Fraud prevention capabilities are lighter compared to platforms focused heavily on device intelligence and behavioral analytics

Pricing can increase significantly for businesses handling large international onboarding volumes

Best for: Global fintechs, crypto platforms, and businesses managing cross-border KYC, KYB, and AML compliance workflows.

3. Entrust IDV

Entrust IDV, formerly known as Onfido, is an AI-driven identity verification platform focused on remote onboarding and document authentication. The platform combines facial biometrics, liveness detection, and AI-powered document verification to help businesses verify users across digital onboarding environments. It is widely used by global fintechs, mobility platforms, and digital businesses operating in mobile-first markets.

Teams use Entrust IDV for remote onboarding, document verification, facial biometrics, and global identity authentication workflows.

Why choose Entrust IDV:

Improve remote onboarding accuracy: Uses AI-driven document authentication and biometric verification to reduce onboarding fraud risks.

Support mobile-first onboarding journeys: Offers developer-friendly SDKs and APIs designed for app-based onboarding experiences.

Expand verification coverage internationally: Supports identity verification across multiple countries and document types globally.

Reduce manual document reviews: Automates identity verification workflows using AI-powered authenticity and liveness checks.

Deliver faster onboarding experiences: Combines biometric verification and document checks within streamlined digital onboarding flows.

Although Entrust IDV performs strongly for remote verification and document AI, buyers should still evaluate a few trade-offs carefully.

India-specific onboarding integrations are less extensive compared to local KYC-focused platforms

Fraud prevention capabilities typically require additional orchestration or external fraud systems

Enterprise implementation and customization may involve longer onboarding cycles for some teams

Best for: Global digital platforms, fintechs, and businesses prioritizing remote onboarding and biometric identity verification.

4. Veriff

Veriff is a global identity verification platform known for video-based onboarding, document authentication, and fraud signal detection. The platform focuses heavily on balancing onboarding speed with verification accuracy across remote digital environments. Many international fintechs, marketplaces, and mobility platforms use Veriff to support scalable identity verification without introducing excessive onboarding friction.

Teams use Veriff for video verification, remote onboarding, fraud screening, and global document verification workflows.

Why choose Veriff:

Improve onboarding conversion rates: Balances identity verification accuracy with lower onboarding friction for genuine users.

Support international onboarding workflows: Verifies users across multiple countries and document types through one scalable verification system.

Detect onboarding fraud earlier: Combines video verification with fraud indicators during onboarding and account creation workflows.

Launch digital onboarding quickly: Offers API-driven onboarding infrastructure for fast implementation across web and mobile products.

Strengthen remote verification experiences: Uses video-based identity verification to improve trust during digital onboarding flows.

While Veriff works well for global onboarding and verification accuracy, there are some limitations businesses should account for.

India-focused government verification workflows are less comprehensive than local onboarding platforms

Fraud prevention capabilities focus primarily on onboarding rather than full lifecycle decisioning

Advanced compliance customization may require additional integrations for complex regulated workflows

Best for: International fintechs, marketplaces, and digital businesses focused on remote onboarding and video-based verification.

5. HyperVerge

HyperVerge is an Indian identity verification platform for BFSI onboarding and Aadhaar-linked workflows. It is particularly recognized for facial recognition accuracy, Video KYC infrastructure, and OCR capabilities across Indian onboarding environments. It is commonly used by banks, NBFCs, and fintech companies handling large-scale digital onboarding within India.

Teams use HyperVerge for Video KYC, facial biometrics, Aadhaar workflows, and India-focused onboarding verification.

Why choose HyperVerge :

Improve Video KYC onboarding quality: Offers strong facial recognition and liveness capabilities for remote onboarding workflows.

Support India-native compliance flows: Handles Aadhaar-linked onboarding and RBI-aligned verification requirements effectively.

Reduce onboarding drop-offs: Uses automated OCR and document verification workflows to simplify customer onboarding journeys.

Accelerate onboarding integration timelines: Provides API-driven onboarding infrastructure for fintechs and BFSI onboarding environments.

Scale onboarding operations efficiently: Supports large onboarding volumes across banks, NBFCs, and regulated financial services businesses.

HyperVerge performs strongly within Indian onboarding ecosystems, though businesses should still evaluate broader operational needs carefully.

International verification coverage is more limited compared to globally focused onboarding providers

Fraud intelligence capabilities are lighter than platforms centered on risk decisioning and behavioral analytics

Teams managing lifecycle fraud may still require additional fraud-prevention systems

Best for: Indian fintechs, NBFCs, and BFSI companies focused on Aadhaar-based onboarding and Video KYC workflows.

6. Signzy

Signzy combines KYC, KYB, and banking workflow automation within a compliance-focused onboarding platform. The company is widely used by banks and financial institutions that need configurable onboarding journeys without building every workflow through engineering-heavy integrations. Its no-code workflow builder is one of its stronger differentiators within regulated BFSI onboarding environments.

Teams use Signzy for KYC, KYB, banking workflow automation, and compliance-focused onboarding operations.

Why choose Signzy:

Simplify onboarding workflow management: Supports configurable no-code onboarding workflows for regulated BFSI operations.

Unify KYC and KYB workflows: Handles both retail customer onboarding and business verification within one compliance framework.

Reduce operational dependency on engineering: Enables onboarding teams to modify workflows without heavy development effort.

Improve audit and compliance visibility: Maintains structured onboarding records and compliance-aligned verification processes.

Support banking-specific onboarding needs: Integrates well with financial services onboarding and compliance environments.

While Signzy is effective for banking automation and compliance workflows, there are a few operational considerations worth noting.

Fraud prevention capabilities are less advanced than platforms built specifically around fraud intelligence and decisioning

Best suited for BFSI environments rather than consumer platforms, facing high onboarding fraud volumes

Some advanced onboarding customizations may still require implementation support

Best for: Banks, NBFCs, and financial institutions managing compliance-heavy onboarding and KYB workflows.

7. Perfios KARZA

Perfios KARZA combines identity verification with financial intelligence and underwriting-focused APIs. The platform is widely used by lenders, NBFCs, and financial institutions that need onboarding verification alongside income, employment, and financial data validation. Its strength lies in connecting onboarding workflows directly with lending and underwriting operations.

Teams use Perfios KARZA for identity verification, financial data aggregation, underwriting support, and lending-focused onboarding workflows.

Why choose Perfios KARZA:

Strengthen lending decisions faster: Combines onboarding verification with financial and underwriting intelligence within connected workflows.

Reduce underwriting friction: Supports income verification, bank-statement analysis, and employment validation through integrated APIs.

Improve onboarding efficiency for lenders: Handles PAN, Aadhaar, GST, and financial verification within centralized onboarding systems.

Support credit-focused onboarding operations: Helps lenders evaluate both identity and financial eligibility during onboarding journeys.

Integrate with lending ecosystems smoothly: Works well for businesses already using Perfios financial intelligence products.

While Perfios KARZA performs strongly for lending and underwriting workflows, there are a few practical trade-offs to keep in mind.

Fraud detection and behavioral intelligence capabilities are lighter than specialized fraud-decisioning platforms

Teams may still require additional onboarding fraud and AML orchestration tools

Best suited for lending operations rather than broader marketplace or gaming onboarding environments

Best for: Lenders, NBFCs, and financial institutions managing underwriting-heavy onboarding and credit verification workflows.

8. AuthBridge

AuthBridge is one of India’s larger verification providers, focused on employee background checks, enterprise onboarding, and verification services. The platform supports employment verification, criminal record checks, education verification, vendor onboarding, and compliance reporting for large organizations. It is commonly used in hiring, HR, and enterprise procurement workflows.

Teams use AuthBridge for employee background verification, vendor onboarding, and enterprise compliance checks.

Why choose AuthBridge:

Simplify employee verification workflows: Supports education, employment, criminal record, and address verification within one verification platform.

Scale enterprise onboarding operations: Handles high-volume background verification across hiring and procurement environments.

Improve vendor onboarding compliance: Supports enterprise verification workflows for vendors, suppliers, and third-party onboarding.

Reduce manual verification effort: Automates large portions of employee and vendor verification processes at scale.

Support enterprise-grade reporting needs: Provides structured compliance and verification reporting for HR and procurement teams.

Although AuthBridge is strong for enterprise verification and hiring workflows, it is important to understand where its focus differs.

Built primarily for verification services rather than real-time onboarding fraud decisioning

Less suited for fintechs or digital platforms managing high-risk consumer onboarding

Consumer identity verification workflows are not as advanced as dedicated KYC onboarding platforms

Best for: Enterprises, HR teams, and businesses focused on employee background verification and vendor onboarding.

Related Read: Compare Top Account Takeover Prevention Software and Build a Full-Stack ATO Defense

Bureau ID vs IDfy: Side-by-Side Comparison

At a high level, both Bureau ID and IDfy help businesses manage onboarding and identity verification. But the way the two platforms approach onboarding risk is fundamentally different.

IDfy is primarily built around compliance-led verification workflows such as KYC, KYB, document verification, and Video KYC. Bureau ID takes a broader approach by combining identity verification with fraud intelligence, device signals, behavioral analytics, and real-time decisioning within a unified platform.

That difference becomes more important as onboarding volumes grow, fraud patterns become more coordinated, and teams try to reduce operational complexity caused by multiple disconnected vendors.

Criteria | Bureau ID | IDfy |

Positioning | Unified risk decisioning platform | Verification and compliance platform |

Core capability | Identity + fraud + device + behavior | KYC, KYB, Video KYC |

Fraud intelligence | High, with graph + device + behavioral signals | Moderate, primarily verification-led |

Real-time decisioning | Built-in, explainable scoring | Limited, often requires external systems |

Device intelligence | 99.97% persistent device ID | Not a core capability |

Behavioral biometrics | Yes | No |

Identity graph | 500M+ identities mapped | Not available |

Workflow orchestration | No-code, configurable by risk teams | API-heavy for complex setups |

Vendor consolidation | High, replaces multiple tools | Often paired with fraud and AML tools |

Lifecycle coverage | Onboarding to transactions | Mostly onboarding |

Best fit | Fintechs, NBFCs, marketplaces, high-risk segments | Compliance-heavy KYC workflows |

When IDfy fits better

IDfy works well for compliance-focused onboarding environments where Video KYC, document verification, and regulated identity checks remain the primary requirement. It is often a strong fit for traditional BFSI workflows where fraud prevention and risk monitoring are handled through separate systems.

When Bureau ID fits better

Bureau ID becomes more relevant when onboarding decisions extend beyond identity verification into full lifecycle trust and fraud evaluation. Fintechs, marketplaces, gaming platforms, and NBFCs often use it to consolidate vendors, improve fraud detection accuracy, and reduce onboarding friction at the same time.

Key benefits teams typically look for include:

Faster onboarding decisions with lower dependency on manual reviews

Stronger fraud detection across onboarding, login, and transaction events

Unified visibility across identity, device, behavioral, and network-level signals

Reduced vendor sprawl across KYC, AML, fraud prevention, and orchestration workflows

More flexibility for risk teams through configurable no-code workflows

Better detection of fraud rings, mule accounts, and repeat offenders

If your onboarding stack is already struggling with fragmented fraud tooling, operational complexity, or rising onboarding abuse, the difference between verification and real-time decisioning becomes much more noticeable at scale.

Take the Next Step Toward Unified Risk Decisioning

A verification stack can look perfectly functional until fraud losses, onboarding delays, and operational overhead start increasing together. For teams using IDfy, these issues begin when onboarding, fraud prevention, AML, and risk workflows operate across separate systems without a unified real-time decisioning layer.

The next step is understanding how identity verification, fraud intelligence, device signals, behavioral analytics, AML, and workflow orchestration should work together within one decisioning system.

If your team is evaluating how to reduce fraud losses while improving onboarding speed and operational efficiency, Bureau ID can help consolidate fragmented onboarding and fraud workflows into a single platform with real-time risk visibility.

Schedule a demo today to see how unified risk decisioning can help your team detect fraud earlier, reduce vendor sprawl, and make faster onboarding decisions at scale.

FAQs

1. What are the best IDfy competitors in 2026?

The best IDfy competitors in 2026 include identity verification and digital onboarding platforms that support KYC, KYB, fraud detection, document verification, liveness checks, and compliance automation. Businesses often compare these platforms based on onboarding speed, API integrations, fraud prevention capabilities, scalability, and regional compliance coverage.

2. Which IDfy alternatives are better for fintech KYC?

Some IDfy alternatives focus more heavily on fintech onboarding workflows, real-time verification, fraud-risk scoring, AML screening, and compliance automation. Fintech companies typically evaluate platforms based on onboarding accuracy, API flexibility, verification coverage, and the ability to reduce manual review effort while maintaining compliance standards.

3. How does Bureau compare with IDfy for onboarding and fraud prevention?

Bureau combines identity verification, fraud prevention, risk decisioning, and onboarding workflows within a unified platform. Businesses often evaluate Bureau against IDfy for capabilities such as real-time fraud detection, device intelligence, behavioral risk analysis, configurable onboarding workflows, and scalable API integrations. Fintech, BFSI, gaming, and marketplace companies also compare both platforms based on onboarding speed, fraud prevention coverage, and operational efficiency.

4. Which platform supports document verification, face match, and liveness detection?

Many IDfy competitors support document verification, biometric face match, passive liveness detection, active liveness checks, and fraud screening workflows. These capabilities help businesses verify user identity, detect spoofing attempts, and reduce onboarding fraud across fintech, BFSI, gaming, and marketplace environments.

5. Which IDfy alternative is better for high-volume onboarding?

High-volume onboarding platforms typically offer automated workflows, scalable APIs, configurable verification logic, and real-time fraud checks. Businesses evaluating IDfy alternatives for scale often prioritize low onboarding friction, fast verification response times, and the ability to process large user volumes without increasing operational overhead.

6. Which IDfy competitor is best for fraud prevention beyond KYC?

Some IDfy competitors extend beyond standard KYC verification by supporting behavioral risk analysis, device intelligence, mule account detection, synthetic identity detection, and adaptive risk scoring. Businesses in fintech, crypto, gaming, and marketplaces often evaluate these advanced fraud-prevention capabilities to strengthen onboarding security and reduce account abuse.

While IDfy is a widely used platform for KYC, document verification, and compliance-led onboarding, evolving fraud patterns are exposing gaps around fraud intelligence, real-time decisioning, device signals, workflow flexibility, and lifecycle risk visibility.

Deloitte’s Center for Financial Services predicts that generative AI could drive fraud losses in the United States from $12.3 billion in 2023 to $40 billion by 2027.

Image Source: Deloitte Center for Financial Services

That makes verification insufficient for high-volume onboarding environments, pushing fintechs, NBFCs, marketplaces, and digital platforms toward IDfy competitors that can evaluate identity, behavior, devices, and risk signals together instead of relying only on static verification checks.

Teams are looking for stronger fraud controls, fewer disconnected vendors, more flexible orchestration, across onboarding, transaction monitoring, AML, device & behavioural signals, and network-level fraud protection.

In this guide, we’ll compare the top IDfy competitors and alternatives for 2026, helping you understand where each platform fits best, which tools are stronger for fraud prevention or onboarding workflows, and what to evaluate before choosing a solution for your fintech or BFSI stack.

Quick Comparison: Best IDfy Alternatives Compared

The best IDfy competitors include identity verification and digital KYC platforms that help businesses automate onboarding, verify users, and prevent fraud across the customer lifecycle.

The right choice depends on whether your team needs stronger fraud intelligence, global identity coverage, stronger KYC workflows, background verification, or government-backed identity checks.

Tool | Best for | Core strength | Fraud capability | Workflow flexibility | Pricing model |

Bureau ID | Unified risk decisioning + network fraud prevention | Identity + fraud + device + behavior | High | High | Platform-based |

Sumsub | Global KYC and AML | Cross-border compliance | Moderate | High | Subscription |

Entrust IDV | Global remote onboarding | Document and biometric AI | Moderate | Moderate | API-based |

Veriff | International verification | Video KYC and fraud signals | Moderate | High | API-based |

HyperVerge | India BFSI onboarding | Face recognition accuracy | Moderate | Moderate | API-based |

Signzy | BFSI automation | AI-driven KYC and KYB | Moderate | High | Subscription |

Perfios KARZA | Lending workflows | Financial data aggregation | Low | Moderate | API-based |

AuthBridge | Background checks | Employee verification | Low | Low | Enterprise |

Each platform solves a different part of onboarding and risk management. Use this table as a first-pass shortlist, then evaluate each tool based on your fraud exposure, compliance needs, onboarding volume, and internal workflow complexity.

How We Evaluated Top IDfy Competitors

This evaluation focuses on what matters when teams replace or extend a verification platform. Fintech professionals highlighted issues such as rising onboarding friction, growing alert fatigue, synthetic identity fraud, and the operational complexity created by disconnected KYC, AML, and fraud workflows.

In fact, Bureau ID’s UK and EU Fraud Report also found that synthetic identity fraud increased by 50%, while digital fraud attempts across the EU rose 43%, highlighting how onboarding fraud is shifting beyond static document verification into coordinated identity, device, and behavioral attacks.

That is why we looked at how these platforms perform in onboarding environments, not feature lists built around marketing claims.

We evaluated each platform across the following criteria:

Identity verification depth: Support for document verification, biometrics, OCR accuracy, liveness detection, and Video KYC across onboarding workflows.

Fraud and risk intelligence: Coverage for device signals, behavioral analytics, fraud-ring detection, synthetic identity prevention, and adaptive risk scoring capabilities.

Workflow orchestration flexibility: Ability to configure onboarding rules, automate reviews, and reduce engineering dependency through APIs or no-code workflows.

Real-time decisioning capabilities: Support for evaluating onboarding, login, and transaction risks instantly instead of relying only on static verification checks.

Compliance and regional coverage: Strength across Indian KYC regulations, Aadhaar-linked workflows, AML checks, and international onboarding requirements.

Scalability for onboarding operations: Performance under high onboarding volumes, operational complexity, and fraud-heavy environments like fintech, gaming, and marketplaces.

Total cost of ownership: Impact of pricing models, engineering effort, operational overhead, and the need for multiple supporting fraud vendors.

This framework reflects how teams increasingly want unified onboarding and fraud decisioning instead of stitching together separate verification, AML, and fraud-prevention tools across the customer lifecycle.

8 Best IDfy Competitors and Alternatives

1. Bureau ID

Bureau ID approaches onboarding and fraud prevention differently from traditional verification-first platforms. Instead of treating identity verification as a standalone compliance step, it combines identity, fraud, device intelligence, behavioral analytics, and real-time risk decisioning within a single orchestration layer.

The platform continuously evaluates trust across onboarding, authentication, and transaction events instead of relying only on static document checks. As onboarding volumes grow, teams often add separate tools for device intelligence, AML, behavioral analytics, and workflow orchestration, which increases complexity without giving them a clear risk view.

Bureau ID positions itself as a unified decisioning platform designed to reduce that vendor sprawl while helping teams make faster, more explainable onboarding and fraud decisions.

Why choose Bureau ID:

Reduce onboarding fraud earlier: Combines identity verification, device intelligence, and behavioral signals to catch suspicious users before account creation completes.

Consolidate fragmented onboarding systems: Replaces multiple fraud, AML, and verification vendors through a single orchestration and decisioning platform integration.

Improve onboarding speed at scale: Uses real-time risk scoring and automated workflows to reduce manual reviews for genuine users significantly.

Detect fraud rings more effectively: Uses a Graph Identity Network with 500M+ linked identities, devices, and behavioral relationships across ecosystems.

Reduce engineering dependency: Supports no-code workflow orchestration so product and risk teams can adapt onboarding rules independently.

Support global compliance workflows: Combines KYC, KYB, AML, onboarding, and fraud decisioning across 195+ international markets from one platform.

Many teams evaluate Bureau ID after they hit the limits of a verification-first setup. KYC checks may pass, but mule accounts, promo abuse, synthetic identities, and coordinated fraud rings still create losses after onboarding. Bureau solves this by connecting identity, device, behavior, network, and transaction signals in one decisioning layer.

What changes after adoption:

Faster onboarding for genuine users with fewer unnecessary manual reviews

Unified visibility across identity, device, behavioral, and transaction-level risk signals

Real-time onboarding and fraud decisions instead of delayed operational reviews

Lower fraud losses through graph-based fraud detection and persistent device intelligence

Reduced operational complexity by consolidating multiple onboarding and fraud vendors

Less engineering overhead through configurable no-code workflow orchestration

Bureau ID also includes several AI-driven fraud and decisioning capabilities that extend beyond traditional identity verification workflows. These capabilities help businesses evaluate user trust continuously instead of relying only on one-time onboarding checks.

AI and decisioning capabilities:

Graph Identity Network: Maps relationships between identities, devices, accounts, and behaviors to uncover coordinated fraud activity at scale.

Behavioral biometrics: Monitors typing patterns, gestures, touchscreen behavior, and interaction anomalies to identify bots and fraud farms.

Persistent device intelligence: Detects spoofed devices, emulators, VPN usage, and repeated fraud attempts even after factory resets.

Real-time explainable risk scoring: Delivers risk decisions in milliseconds with visibility into the underlying fraud and behavioral signals.

Adaptive onboarding workflows: Configures onboarding, AML, KYB, and fraud rules dynamically by geography, product, and user-risk profile.

Together, these capabilities make Bureau ID a strong fit for businesses trying to balance onboarding speed, fraud prevention, compliance, and operational efficiency within a single platform instead of managing disconnected systems across the customer lifecycle.

Real outcomes: How Bureau ID improved fraud prevention for a food delivery platform

One food delivery platform struggled with coordinated fraud rings abusing promotions and onboarding incentives across thousands of fake accounts. The company relied on fragmented onboarding and fraud systems, which made it difficult to identify linked fraud behavior in real time while maintaining a smooth onboarding experience for genuine users.

Bureau ID implemented unified onboarding and fraud decisioning using device intelligence, behavioral biometrics, graph-based identity analysis, and real-time risk scoring. The company also used configurable workflows to automate fraud reviews and reduce operational dependency on manual investigations.

Results:

Mapped and blocked a 2,700+ user fraud ring operating across 150 connected devices

Removed 1,750+ fraudulent accounts linked to just 3 devices, eliminating major abuse vectors

Flagged 97% of collusive users with high-risk scores for deeper investigation

Blocked repeat offenders through persistent device and behavioral intelligence, helping strengthen long-term fraud protection

Read the full case study here → A Food Delivery Company Eliminates a 2,700-User Fraud Ring

Bureau ID is best for fintechs, NBFCs, marketplaces, gaming platforms, and digital businesses operating in high-risk onboarding environments. Although Bureau ID comes at a higher price point than verification-only tools, its broader feature set and full-lifecycle fraud coverage can make it a stronger long-term investment for businesses managing complex onboarding, fraud prevention, AML, and risk decisioning workflows.

If your team is evaluating how to reduce vendor sprawl while improving onboarding speed and fraud detection together, book a 30-minute demo with Bureau ID to learn how it fits into your current risk and onboarding stack.

2. Sumsub

Sumsub is a global identity verification and compliance platform focused on KYC, KYB, AML screening, and cross-border onboarding. The platform is widely used by fintechs, crypto companies, and digital businesses operating across multiple geographies. Its strength lies in helping teams manage regional compliance workflows from one centralized system while supporting large-scale international onboarding operations.

Teams use Sumsub for global onboarding, identity verification, AML screening, and multi-country compliance management.

Why choose Sumsub:

Expand into global markets faster: Supports identity verification workflows across 220+ countries and territories through one onboarding platform.

Simplify AML and sanctions compliance: Combines KYC, KYB, sanctions screening, and PEP monitoring within a unified compliance workflow.

Reduce operational complexity across regions: Allows teams to configure onboarding flows by geography, regulation, and user-risk profile.

Improve onboarding scalability: Supports automated verification workflows that reduce manual review requirements for international onboarding teams.

Support crypto and high-risk industries: Offers strong regulatory coverage for fintech, crypto, trading, and digital financial services environments.

While Sumsub handles international compliance and onboarding particularly well, there are a few practical considerations worth evaluating before implementation.

India-specific Aadhaar and DigiLocker workflows are less mature compared to India-native onboarding platforms

Fraud prevention capabilities are lighter compared to platforms focused heavily on device intelligence and behavioral analytics

Pricing can increase significantly for businesses handling large international onboarding volumes

Best for: Global fintechs, crypto platforms, and businesses managing cross-border KYC, KYB, and AML compliance workflows.

3. Entrust IDV

Entrust IDV, formerly known as Onfido, is an AI-driven identity verification platform focused on remote onboarding and document authentication. The platform combines facial biometrics, liveness detection, and AI-powered document verification to help businesses verify users across digital onboarding environments. It is widely used by global fintechs, mobility platforms, and digital businesses operating in mobile-first markets.

Teams use Entrust IDV for remote onboarding, document verification, facial biometrics, and global identity authentication workflows.

Why choose Entrust IDV:

Improve remote onboarding accuracy: Uses AI-driven document authentication and biometric verification to reduce onboarding fraud risks.

Support mobile-first onboarding journeys: Offers developer-friendly SDKs and APIs designed for app-based onboarding experiences.

Expand verification coverage internationally: Supports identity verification across multiple countries and document types globally.

Reduce manual document reviews: Automates identity verification workflows using AI-powered authenticity and liveness checks.

Deliver faster onboarding experiences: Combines biometric verification and document checks within streamlined digital onboarding flows.

Although Entrust IDV performs strongly for remote verification and document AI, buyers should still evaluate a few trade-offs carefully.

India-specific onboarding integrations are less extensive compared to local KYC-focused platforms

Fraud prevention capabilities typically require additional orchestration or external fraud systems

Enterprise implementation and customization may involve longer onboarding cycles for some teams

Best for: Global digital platforms, fintechs, and businesses prioritizing remote onboarding and biometric identity verification.

4. Veriff

Veriff is a global identity verification platform known for video-based onboarding, document authentication, and fraud signal detection. The platform focuses heavily on balancing onboarding speed with verification accuracy across remote digital environments. Many international fintechs, marketplaces, and mobility platforms use Veriff to support scalable identity verification without introducing excessive onboarding friction.

Teams use Veriff for video verification, remote onboarding, fraud screening, and global document verification workflows.

Why choose Veriff:

Improve onboarding conversion rates: Balances identity verification accuracy with lower onboarding friction for genuine users.

Support international onboarding workflows: Verifies users across multiple countries and document types through one scalable verification system.

Detect onboarding fraud earlier: Combines video verification with fraud indicators during onboarding and account creation workflows.

Launch digital onboarding quickly: Offers API-driven onboarding infrastructure for fast implementation across web and mobile products.

Strengthen remote verification experiences: Uses video-based identity verification to improve trust during digital onboarding flows.

While Veriff works well for global onboarding and verification accuracy, there are some limitations businesses should account for.

India-focused government verification workflows are less comprehensive than local onboarding platforms

Fraud prevention capabilities focus primarily on onboarding rather than full lifecycle decisioning

Advanced compliance customization may require additional integrations for complex regulated workflows

Best for: International fintechs, marketplaces, and digital businesses focused on remote onboarding and video-based verification.

5. HyperVerge

HyperVerge is an Indian identity verification platform for BFSI onboarding and Aadhaar-linked workflows. It is particularly recognized for facial recognition accuracy, Video KYC infrastructure, and OCR capabilities across Indian onboarding environments. It is commonly used by banks, NBFCs, and fintech companies handling large-scale digital onboarding within India.

Teams use HyperVerge for Video KYC, facial biometrics, Aadhaar workflows, and India-focused onboarding verification.

Why choose HyperVerge :

Improve Video KYC onboarding quality: Offers strong facial recognition and liveness capabilities for remote onboarding workflows.

Support India-native compliance flows: Handles Aadhaar-linked onboarding and RBI-aligned verification requirements effectively.

Reduce onboarding drop-offs: Uses automated OCR and document verification workflows to simplify customer onboarding journeys.

Accelerate onboarding integration timelines: Provides API-driven onboarding infrastructure for fintechs and BFSI onboarding environments.

Scale onboarding operations efficiently: Supports large onboarding volumes across banks, NBFCs, and regulated financial services businesses.

HyperVerge performs strongly within Indian onboarding ecosystems, though businesses should still evaluate broader operational needs carefully.

International verification coverage is more limited compared to globally focused onboarding providers

Fraud intelligence capabilities are lighter than platforms centered on risk decisioning and behavioral analytics

Teams managing lifecycle fraud may still require additional fraud-prevention systems

Best for: Indian fintechs, NBFCs, and BFSI companies focused on Aadhaar-based onboarding and Video KYC workflows.

6. Signzy

Signzy combines KYC, KYB, and banking workflow automation within a compliance-focused onboarding platform. The company is widely used by banks and financial institutions that need configurable onboarding journeys without building every workflow through engineering-heavy integrations. Its no-code workflow builder is one of its stronger differentiators within regulated BFSI onboarding environments.

Teams use Signzy for KYC, KYB, banking workflow automation, and compliance-focused onboarding operations.

Why choose Signzy:

Simplify onboarding workflow management: Supports configurable no-code onboarding workflows for regulated BFSI operations.

Unify KYC and KYB workflows: Handles both retail customer onboarding and business verification within one compliance framework.

Reduce operational dependency on engineering: Enables onboarding teams to modify workflows without heavy development effort.

Improve audit and compliance visibility: Maintains structured onboarding records and compliance-aligned verification processes.

Support banking-specific onboarding needs: Integrates well with financial services onboarding and compliance environments.

While Signzy is effective for banking automation and compliance workflows, there are a few operational considerations worth noting.

Fraud prevention capabilities are less advanced than platforms built specifically around fraud intelligence and decisioning

Best suited for BFSI environments rather than consumer platforms, facing high onboarding fraud volumes

Some advanced onboarding customizations may still require implementation support

Best for: Banks, NBFCs, and financial institutions managing compliance-heavy onboarding and KYB workflows.

7. Perfios KARZA

Perfios KARZA combines identity verification with financial intelligence and underwriting-focused APIs. The platform is widely used by lenders, NBFCs, and financial institutions that need onboarding verification alongside income, employment, and financial data validation. Its strength lies in connecting onboarding workflows directly with lending and underwriting operations.

Teams use Perfios KARZA for identity verification, financial data aggregation, underwriting support, and lending-focused onboarding workflows.

Why choose Perfios KARZA:

Strengthen lending decisions faster: Combines onboarding verification with financial and underwriting intelligence within connected workflows.

Reduce underwriting friction: Supports income verification, bank-statement analysis, and employment validation through integrated APIs.

Improve onboarding efficiency for lenders: Handles PAN, Aadhaar, GST, and financial verification within centralized onboarding systems.

Support credit-focused onboarding operations: Helps lenders evaluate both identity and financial eligibility during onboarding journeys.

Integrate with lending ecosystems smoothly: Works well for businesses already using Perfios financial intelligence products.

While Perfios KARZA performs strongly for lending and underwriting workflows, there are a few practical trade-offs to keep in mind.

Fraud detection and behavioral intelligence capabilities are lighter than specialized fraud-decisioning platforms

Teams may still require additional onboarding fraud and AML orchestration tools

Best suited for lending operations rather than broader marketplace or gaming onboarding environments

Best for: Lenders, NBFCs, and financial institutions managing underwriting-heavy onboarding and credit verification workflows.

8. AuthBridge

AuthBridge is one of India’s larger verification providers, focused on employee background checks, enterprise onboarding, and verification services. The platform supports employment verification, criminal record checks, education verification, vendor onboarding, and compliance reporting for large organizations. It is commonly used in hiring, HR, and enterprise procurement workflows.

Teams use AuthBridge for employee background verification, vendor onboarding, and enterprise compliance checks.

Why choose AuthBridge:

Simplify employee verification workflows: Supports education, employment, criminal record, and address verification within one verification platform.

Scale enterprise onboarding operations: Handles high-volume background verification across hiring and procurement environments.

Improve vendor onboarding compliance: Supports enterprise verification workflows for vendors, suppliers, and third-party onboarding.

Reduce manual verification effort: Automates large portions of employee and vendor verification processes at scale.

Support enterprise-grade reporting needs: Provides structured compliance and verification reporting for HR and procurement teams.

Although AuthBridge is strong for enterprise verification and hiring workflows, it is important to understand where its focus differs.

Built primarily for verification services rather than real-time onboarding fraud decisioning

Less suited for fintechs or digital platforms managing high-risk consumer onboarding

Consumer identity verification workflows are not as advanced as dedicated KYC onboarding platforms

Best for: Enterprises, HR teams, and businesses focused on employee background verification and vendor onboarding.

Related Read: Compare Top Account Takeover Prevention Software and Build a Full-Stack ATO Defense

Bureau ID vs IDfy: Side-by-Side Comparison

At a high level, both Bureau ID and IDfy help businesses manage onboarding and identity verification. But the way the two platforms approach onboarding risk is fundamentally different.

IDfy is primarily built around compliance-led verification workflows such as KYC, KYB, document verification, and Video KYC. Bureau ID takes a broader approach by combining identity verification with fraud intelligence, device signals, behavioral analytics, and real-time decisioning within a unified platform.

That difference becomes more important as onboarding volumes grow, fraud patterns become more coordinated, and teams try to reduce operational complexity caused by multiple disconnected vendors.

Criteria | Bureau ID | IDfy |

Positioning | Unified risk decisioning platform | Verification and compliance platform |

Core capability | Identity + fraud + device + behavior | KYC, KYB, Video KYC |

Fraud intelligence | High, with graph + device + behavioral signals | Moderate, primarily verification-led |

Real-time decisioning | Built-in, explainable scoring | Limited, often requires external systems |

Device intelligence | 99.97% persistent device ID | Not a core capability |

Behavioral biometrics | Yes | No |

Identity graph | 500M+ identities mapped | Not available |

Workflow orchestration | No-code, configurable by risk teams | API-heavy for complex setups |

Vendor consolidation | High, replaces multiple tools | Often paired with fraud and AML tools |

Lifecycle coverage | Onboarding to transactions | Mostly onboarding |

Best fit | Fintechs, NBFCs, marketplaces, high-risk segments | Compliance-heavy KYC workflows |

When IDfy fits better

IDfy works well for compliance-focused onboarding environments where Video KYC, document verification, and regulated identity checks remain the primary requirement. It is often a strong fit for traditional BFSI workflows where fraud prevention and risk monitoring are handled through separate systems.

When Bureau ID fits better

Bureau ID becomes more relevant when onboarding decisions extend beyond identity verification into full lifecycle trust and fraud evaluation. Fintechs, marketplaces, gaming platforms, and NBFCs often use it to consolidate vendors, improve fraud detection accuracy, and reduce onboarding friction at the same time.

Key benefits teams typically look for include:

Faster onboarding decisions with lower dependency on manual reviews

Stronger fraud detection across onboarding, login, and transaction events

Unified visibility across identity, device, behavioral, and network-level signals

Reduced vendor sprawl across KYC, AML, fraud prevention, and orchestration workflows

More flexibility for risk teams through configurable no-code workflows

Better detection of fraud rings, mule accounts, and repeat offenders

If your onboarding stack is already struggling with fragmented fraud tooling, operational complexity, or rising onboarding abuse, the difference between verification and real-time decisioning becomes much more noticeable at scale.

Take the Next Step Toward Unified Risk Decisioning

A verification stack can look perfectly functional until fraud losses, onboarding delays, and operational overhead start increasing together. For teams using IDfy, these issues begin when onboarding, fraud prevention, AML, and risk workflows operate across separate systems without a unified real-time decisioning layer.

The next step is understanding how identity verification, fraud intelligence, device signals, behavioral analytics, AML, and workflow orchestration should work together within one decisioning system.

If your team is evaluating how to reduce fraud losses while improving onboarding speed and operational efficiency, Bureau ID can help consolidate fragmented onboarding and fraud workflows into a single platform with real-time risk visibility.

Schedule a demo today to see how unified risk decisioning can help your team detect fraud earlier, reduce vendor sprawl, and make faster onboarding decisions at scale.

FAQs

1. What are the best IDfy competitors in 2026?

The best IDfy competitors in 2026 include identity verification and digital onboarding platforms that support KYC, KYB, fraud detection, document verification, liveness checks, and compliance automation. Businesses often compare these platforms based on onboarding speed, API integrations, fraud prevention capabilities, scalability, and regional compliance coverage.

2. Which IDfy alternatives are better for fintech KYC?

Some IDfy alternatives focus more heavily on fintech onboarding workflows, real-time verification, fraud-risk scoring, AML screening, and compliance automation. Fintech companies typically evaluate platforms based on onboarding accuracy, API flexibility, verification coverage, and the ability to reduce manual review effort while maintaining compliance standards.

3. How does Bureau compare with IDfy for onboarding and fraud prevention?

Bureau combines identity verification, fraud prevention, risk decisioning, and onboarding workflows within a unified platform. Businesses often evaluate Bureau against IDfy for capabilities such as real-time fraud detection, device intelligence, behavioral risk analysis, configurable onboarding workflows, and scalable API integrations. Fintech, BFSI, gaming, and marketplace companies also compare both platforms based on onboarding speed, fraud prevention coverage, and operational efficiency.

4. Which platform supports document verification, face match, and liveness detection?

Many IDfy competitors support document verification, biometric face match, passive liveness detection, active liveness checks, and fraud screening workflows. These capabilities help businesses verify user identity, detect spoofing attempts, and reduce onboarding fraud across fintech, BFSI, gaming, and marketplace environments.

5. Which IDfy alternative is better for high-volume onboarding?

High-volume onboarding platforms typically offer automated workflows, scalable APIs, configurable verification logic, and real-time fraud checks. Businesses evaluating IDfy alternatives for scale often prioritize low onboarding friction, fast verification response times, and the ability to process large user volumes without increasing operational overhead.

6. Which IDfy competitor is best for fraud prevention beyond KYC?

Some IDfy competitors extend beyond standard KYC verification by supporting behavioral risk analysis, device intelligence, mule account detection, synthetic identity detection, and adaptive risk scoring. Businesses in fintech, crypto, gaming, and marketplaces often evaluate these advanced fraud-prevention capabilities to strengthen onboarding security and reduce account abuse.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.