Best Fraud Detection Software in 2026 for Unified Risk Decisions

Best Fraud Detection Software in 2026 for Unified Risk Decisions

Best Fraud Detection Software in 2026 for Unified Risk Decisions

Explore the best fraud detection software in 2026 with a tool-by-tool comparison, selection criteria, buyer checklist, and platform shortlist tips.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

Fraud teams often lack clear, real-time decisions when fraud moves across signups, logins, payments, refunds, withdrawals, and account activity. A basic fraud alert may flag risk, but it rarely tells teams what to do next without slowing down genuine customers.

The best fraud detection software helps close that gap. It connects identity, device, behavior, transaction, network, and AML signals so teams can detect suspicious activity, reduce false positives, automate reviews, and act faster across the customer journey.

In this guide, we compare nine top fraud detection tools for 2026: Bureau ID, Sift, SEON, BioCatch, Kount, Feedzai, DataVisor, Sardine, and LexisNexis ThreatMetrix.

You will see where each platform fits best, what to look for in a fraud detection platform, and how to shortlist the right software for your fintech, banking, ecommerce, or marketplace risk stack.

Fraud Detection Software Comparison: Top Tools at a Glance

The best fraud detection software helps businesses detect suspicious users, transactions, accounts, and behaviors in real time. It combines risk scoring, identity signals, device intelligence, behavioral analytics, rules, and machine learning. Strong platforms help fraud teams prevent payment fraud, account takeover, fake accounts, promo abuse, and chargebacks while supporting faster decisions, fewer false positives, case review, and compliance reporting.

A fraud detection software comparison should start with fit, not feature count. The right platform depends on where fraud appears in your journey, such as onboarding, login, payment, account recovery, withdrawal, refund, or repeat account activity.

Tool | Core strength | Key consideration | Best for |

Bureau ID | Identity, device, behavior, network, and transaction signals | Best for teams replacing fragmented fraud tools | Unified fraud risk decisioning |

Sift | Account, payment, and abuse prevention | Check fit for deeper identity and AML needs | Digital fraud operations |

SEON | Email, phone, IP, device, and digital footprint signals | Strong when enrichment is central to the workflow | Data enrichment and fraud checks |

BioCatch | Behavioral biometrics and session intelligence | May need complementary identity or AML tools | Behavioral analytics |

Kount | Transaction risk and identity trust | Stronger for payment-heavy use cases | Payment and account fraud |

Feedzai | Transaction monitoring and risk operations | Often better suited for large institutions | Enterprise financial crime prevention |

DataVisor | Adaptive AI and cross-entity intelligence | Evaluate explainability and analyst usability | Unknown fraud pattern detection |

Sardine | Device, behavior, payment, and AML signals | Best fit for high-risk financial workflows | Fraud, payments, and compliance |

LexisNexis ThreatMetrix | Device, identity, and network intelligence | Works well as part of a broader risk stack | Digital identity intelligence |

This table gives you a quick shortlist, but it should not be the only basis for choosing a platform.

A strong fraud detection platform also needs to match your fraud patterns, internal workflows, transaction volume, compliance needs, and review process. This broader coverage matters because the FBI's 2025 Internet Crime Report accounted for 452,868 cyber-enabled fraud complaints and $17.697 billion in losses in 2025, representing 45% of complaints and 85% of reported losses.

That is why the selection criteria matter as much as the vendor list.

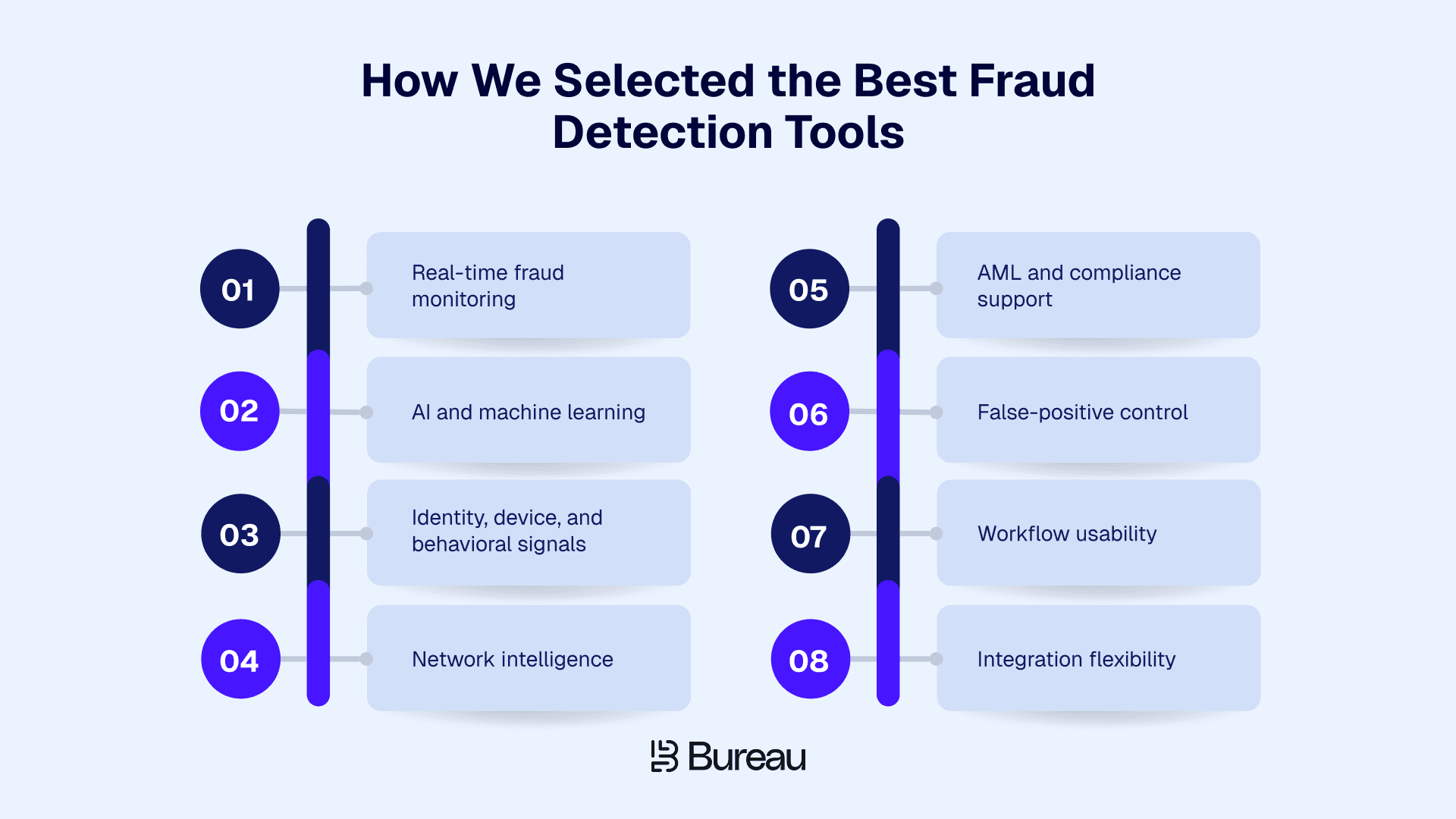

How We Selected the Best Fraud Detection Tools

Selecting the best fraud detection software requires buyers to understand how each tool collects signals, scores risk, explains decisions, reduces false positives, and fits into existing workflows.

For this fraud prevention software review, we looked at practical buying criteria that matter to teams already comparing platforms:

Real-time fraud monitoring: The platform should score risk during onboarding, login, payment, withdrawal, account recovery, and profile changes.

AI and machine learning: The tool should detect known and emerging fraud patterns without relying only on static rules.

Identity, device, and behavioral signals: Strong tools combine who the user is, what device they use, how they behave, and whether the activity matches past patterns.

Network intelligence: The platform should uncover linked accounts, repeat devices, fraud rings, mule activity, or coordinated attacks.

AML and compliance support: Regulated teams should check transaction monitoring, audit trails, sanctions workflows, and mule-risk signals.

False-positive control: The tool should stop fraud without rejecting too many genuine users.

Workflow usability: Analysts should review risk reasons, tune rules, prioritize cases, and take action quickly.

Integration flexibility: APIs, SDKs, webhooks, and case-management compatibility matter for deployment speed.

For payment-heavy teams, features like real-time monitoring are becoming more urgent. In fact, MRC’s 2026 Global Payments and Fraud Report found that 45% of merchants named real-time payment fraud as the next biggest fraud attack overall.

The strongest platforms usually connect multiple risk signals and turn them into decisions that fraud, compliance, and operations teams can actually use. That difference matters when the goal is to act on fraud quickly without adding more manual review or customer friction.

Related Read: A Buyer’s Guide To Fraud Detection Software For Fintech Teams

9 Best Fraud Detection Software in 2026

Each tool below solves a different part of the fraud problem, from payment fraud and account takeover to behavioral analytics, AML workflows, and unified risk decisioning. Use these reviews to understand where each platform fits best and what to consider before adding it to your shortlist.

1. Bureau ID

Bureau ID is a unified risk decisioning platform built for businesses that need fraud detection across onboarding, authentication, transactions, payments, and ongoing account activity. It brings identity, device, behavior, network, and transaction signals into one decisioning layer, helping fraud teams detect risky users faster, reduce false positives, automate workflows, and avoid managing separate tools for every fraud use case.

Key strengths:

Unified risk visibility: Bureau ID connects identity, device, behavior, network, and transaction signals so teams can see risk across the full customer journey instead of reviewing isolated alerts.

Real-time decisions: The platform helps teams score users, devices, accounts, and transactions in real time, which is useful when fraud needs to be stopped before money moves or access is granted.

Explainable risk scores: It gives fraud, compliance, and operations teams clearer reasons behind risk decisions, making it easier to review cases, tune rules, and justify actions internally.

Workflow customization: No-code and low-code configuration helps teams adjust fraud rules, thresholds, and decision flows without depending on engineering for every operational change.

Fraud network detection: It also helps uncover linked identities, devices, accounts, and transactions, making it useful for detecting fraud rings, mule activity, synthetic identities, and repeat offenders.

Lower operational load: By consolidating signals and automating decisions, Bureau ID helps teams reduce manual reviews while still protecting genuine users from unnecessary friction.

Why Bureau ID stands out:

Uses alternate data, device intelligence, behavioral biometrics, identity verification, graph intelligence, and contextual decisioning in one risk decisioning layer.

Analyzes device risk using 160+ signals, including rooted devices, emulator usage, and spoofed environments.

Maps connections between users, devices, IPs, behaviors, and transactions to uncover collusion and fraud rings at scale.

Supports real-time, explainable scoring models that help teams act on risk without relying only on post-transaction reviews.

These capabilities make Bureau ID especially useful for teams that need to stop fraud before damage happens, not just investigate it after the fact. A strong example is Bureau ID’s work with a leading proptech company that was dealing with chargeback fraud on credit card rent payments.

Case study: How a leading proptech saved $1.25M in chargeback fraud with Bureau ID

The proptech company offered credit card rent payments for user convenience, but fraudsters abused the flow through fake chargebacks. Existing controls were reactive, fragmented, and hard to explain, allowing chargeback fraud to escalate after transactions were completed.

What Bureau ID implemented:

Built a real-time, explainable risk scoring system using Bureau ID’s Alternate Data.

Evaluated user trustworthiness and transaction risk using 200+ live signals.

Used signals such as telco metadata, UPI integrity, email quality, identity consistency, transaction attributes, and digital footprint.

Segmented users into low-risk, moderate-risk, and high-risk bands.

Restricted risky users from sensitive flows such as credit card rent payments.

Results achieved:

Prevented $1.25M in chargeback fraud in three months.

Reduced false chargeback rates from 40% to 8%.

Stopped 1,200+ high-risk transactions before payment.

Flagged 60,000+ users as high-risk for chargeback fraud.

Enabled sub-150ms scoring latency for faster risk decisions.

Read the full case study here → A Leading PropTech Saves $1.25M in Chargeback Fraud

Bureau ID is a strong fit when fraud risk cuts across multiple workflows, but teams should still evaluate how it fits their current stack and operating model.

What to consider:

Bureau ID is best suited for teams that want a broader fraud risk decisioning layer, not just a single-purpose fraud signal.

Teams with existing fraud tools should map where Bureau ID will replace, complement, or orchestrate current systems across onboarding, ATO, mule risk, bot detection, payment fraud, and transaction monitoring.

Best for: Bureau ID is best for fintechs, banks, marketplaces, ecommerce businesses, lenders, gaming platforms, and digital-first companies that need unified fraud risk decisioning across identity, device, behavior, network, and transaction signals.

2. Sift

Sift is a digital fraud prevention platform built for online businesses that need to detect account abuse, payment fraud, content abuse, and suspicious user activity. It uses machine learning and fraud workflow tools to help teams assess user and transaction risk across digital touchpoints, making it relevant for marketplaces, subscription platforms, ecommerce brands, and online services with high user volumes.

Key strengths:

Account abuse detection: Sift helps teams identify risky accounts, suspicious signups, and abusive user behavior before they create larger losses.

Payment fraud protection: The platform supports fraud decisions around transactions, chargebacks, and payment risk, which is useful for ecommerce and marketplace teams.

Machine-learning-based scoring: It uses machine learning to help teams detect suspicious behavior without depending only on static rules.

Fraud operations support: Case review and investigation workflows help analysts review risky users, understand patterns, and act faster.

Platform abuse coverage: It is also useful for businesses dealing with multiple abuse types, including payment fraud, account fraud, and content or policy abuse.

Sift works well for digital businesses that need broad fraud operations support across users, payments, and platform activity. Buyers should still check whether it gives them enough depth for identity, AML, or advanced orchestration needs.

What to consider:

Some G2 reviews note that Sift can occasionally generate false positives, which may increase review workload for fraud teams.

Buyers with deeper compliance or identity verification needs should assess whether Sift needs to be paired with other tools in the stack.

Best for: Sift is best for digital platforms, marketplaces, subscription businesses, and online services that need fraud prevention across user accounts, payments, and platform abuse.

3. SEON

SEON is a fraud prevention and AML compliance platform known for data enrichment, digital footprint checks, device intelligence, and flexible risk scoring. It helps teams evaluate users through signals such as email, phone, IP, device, and online presence, making it useful for businesses that need fast fraud checks during onboarding, login, payment, or account activity.

Key strengths:

Data enrichment: SEON helps teams build richer user profiles using email, phone, IP, device, and digital footprint data.

Fast fraud checks: The platform supports quick risk decisions during digital interactions, which helps teams respond before fraud moves downstream.

Flexible rules: Custom rules and scoring workflows help teams adapt fraud checks to their own risk patterns.

Device intelligence: It can help detect multi-accounting, account takeover, onboarding abuse, and suspicious device behavior.

Accessible usability: SEON is often positioned as easy to use for teams that want fraud checks without heavy implementation complexity.

SEON is strong when enrichment and flexible rules sit at the center of the fraud workflow. Teams should still evaluate whether enrichment alone is enough for their broader risk, compliance, or behavioral analytics needs.

What to consider:

Buyers should assess whether they also need deeper behavioral biometrics, AML workflows, or orchestration.

Some users suggest that SEON’s initial setup can require a learning curve, especially for teams trying to use advanced features well.

Best for: SEON is best for businesses that need flexible fraud checks using email, phone, IP, device, and digital footprint intelligence.

4. BioCatch

BioCatch focuses on behavioral biometrics and user-session intelligence. It analyzes how users interact with their devices, including typing rhythm, mouse movement, touchscreen behavior, session flow, and other behavior patterns. This makes it especially useful for banks and financial institutions that need to detect account takeover, scams, mule activity, and suspicious sessions.

Key strengths:

Behavioral biometrics: BioCatch helps teams detect suspicious activity by analyzing how users behave during digital sessions.

Account takeover detection: The platform can identify risk even when a user appears to have valid credentials.

Scam and mule-risk signals: Behavioral intelligence can help uncover unusual patterns linked to scams, social engineering, and mule activity.

Session-level insight: Teams can assess risk during the customer session, not only after a transaction has happened.

Low-friction detection layer: Behavioral signals add fraud context without necessarily forcing every user through extra verification.

BioCatch is valuable when behavioral analytics is the missing layer in a fraud stack. It is especially relevant for financial institutions, but buyers should check how it fits with identity, device, transaction, and AML systems.

What to consider:

Since BioCatch is behavioral-signal focused, teams may still need complementary identity, device, transaction monitoring, or AML tools.

Some PeerSpot commentary suggests that model decision-making in BioCatch can feel complex and not fully transparent for users reviewing outcomes.

Best for: BioCatch is best for banks and financial institutions that need behavioral analytics to detect account takeover, scams, mule activity, and suspicious user sessions.

5. Kount

Kount is a fraud detection and prevention platform focused on digital identity trust, payment fraud, account fraud, and transaction risk. It helps businesses make real-time risk decisions around payments, account activity, and customer interactions, making it relevant for retailers, ecommerce businesses, digital platforms, and transaction-heavy companies.

Key strengths:

Payment fraud detection: Kount helps businesses assess transaction risk and reduce exposure to fraudulent payments.

Chargeback protection: The platform supports teams trying to lower chargebacks and improve payment approval quality.

Identity trust signals: It helps distinguish trusted customers from risky activity using identity and transaction context.

Automated fraud checks: Rules and automation can reduce the volume of transactions that require manual review.

Transaction-focused decisioning: It is also useful for businesses where payment risk is one of the most urgent fraud problems.

Kount is a practical fit for businesses where payment fraud, chargebacks, and transaction risk are central concerns. Buyers should still assess whether it covers non-payment fraud needs deeply enough.

What to consider:

A G2 review notes that Kount’s configuration process can be complex and may require time and attention to detail.

Buyers should check whether Kount covers non-payment fraud needs deeply enough.

Best for: Kount is best for payment-heavy businesses, retailers, ecommerce brands, digital platforms, and transaction-driven companies that need real-time payment and account-risk decisions.

6. Feedzai

Feedzai is an enterprise fraud and financial crime prevention platform built for banks, payment providers, fintechs, and large financial institutions. It supports real-time transaction monitoring, fraud scoring, scam detection, and risk operations, making it especially relevant for organizations with high transaction volumes and complex financial crime workflows.

Key strengths:

Enterprise transaction monitoring: Feedzai supports high-volume transaction screening and fraud monitoring for large financial institutions.

Financial crime coverage: It helps teams manage fraud and financial crime risk across payment and banking workflows.

AI-based risk scoring: It uses AI to support fraud detection and help teams identify emerging patterns.

Risk operations support: Case management and investigation workflows help large teams review alerts and take action.

Regulated-market fit: The platform is useful for organizations that need fraud controls aligned with compliance-heavy operating environments.

Feedzai is strong when scale, transaction monitoring, and financial crime coverage are the main priorities. It is usually a better fit for larger institutions than smaller teams with lighter fraud operations.

What to consider:

Buyers should evaluate deployment complexity, data requirements, and internal team readiness before shortlisting Feedzai.

Smaller teams may need to assess whether the platform is more advanced than their current operating model requires.

Best for: Feedzai is best for banks, payment networks, and large financial institutions that need enterprise-grade transaction monitoring and financial crime prevention.

7. DataVisor

DataVisor is an AI-native fraud and risk platform focused on real-time decisioning, adaptive AI, and cross-entity intelligence. It is often evaluated by organizations dealing with high-volume digital activity, unknown fraud patterns, coordinated attacks, and fraud rings that static rules may miss.

Key strengths:

Unknown fraud detection: DataVisor helps teams identify emerging fraud patterns that may not match existing rules.

Adaptive AI: It supports machine-learning-led detection for fast-changing attacks and complex fraud behavior.

Cross-entity intelligence: The platform helps connect accounts, users, devices, transactions, and behaviors to uncover coordinated activity.

Real-time scoring: It supports fast risk scoring for digital activity and transaction flows.

Fraud ring detection: It is also useful for teams dealing with organized attacks, repeat offenders, and linked suspicious accounts.

DataVisor is compelling for teams that need to detect fraud patterns before they become obvious. It works best when the business has enough data maturity and analyst capacity to act on model-driven insights.

What to consider:

Some users suggest that DataVisor setup and integration can be complex, especially for smaller teams without deep technical resources.

Buyers should check how easily analysts can interpret and act on model outputs.

Best for: DataVisor is best for enterprises and digital platforms that need to detect unknown fraud patterns, coordinated attacks, and fraud rings at scale.

8. Sardine

Sardine is a fraud and compliance platform used by digital finance, payments, and high-risk businesses. It combines device intelligence, behavioral biometrics, payment-risk scoring, AML workflows, and transaction monitoring, making it relevant for teams that want fraud and compliance signals in one risk workflow.

Key strengths:

Fraud and AML coverage: Sardine helps teams connect fraud prevention with compliance-heavy workflows such as AML monitoring.

Device and behavioral signals: The platform uses device intelligence and behavioral biometrics to help identify risky activity.

Payment-risk scoring: It supports payment and account-risk decisions for financial and high-risk digital environments.

Real-time monitoring: Teams can assess risk across onboarding, login, account funding, payments, and ongoing activity.

High-risk workflow fit: It is useful for fintechs, crypto platforms, payment businesses, and other teams with fast-moving fraud risk.

Sardine is strong when teams need fraud, payments, and compliance signals together. Buyers should still check whether the platform’s depth and pricing model fit their exact risk workflow and budget.

What to consider:

Buyers should evaluate how its AML and fraud workflows align with their internal compliance model.

Teams outside fintech, crypto, payments, or high-risk financial workflows should assess whether Sardine is broader than they need.

Best for: Sardine is best for fintechs, crypto platforms, payments companies, and high-risk digital finance businesses that need fraud and compliance signals together.

9. LexisNexis ThreatMetrix

LexisNexis ThreatMetrix is a digital identity intelligence and fraud prevention solution used to assess risk across devices, identities, locations, and digital interactions. It helps enterprises build trust decisions using device intelligence, identity context, and network signals, making it relevant for large organizations with complex authentication and fraud prevention needs.

Key strengths:

Digital identity intelligence: ThreatMetrix helps teams assess whether a user, device, or interaction can be trusted.

Device-risk insight: The platform analyzes device, location, and network signals to support fraud and authentication decisions.

Network intelligence: LexisNexis Digital Identity Network helps enrich fraud decisions with shared risk context.

Risk-based authentication support: Teams can use ThreatMetrix signals to challenge high-risk users while reducing friction for trusted users.

Enterprise-scale fit: It also works well for large organizations that need identity-risk context across multiple channels.

ThreatMetrix is useful when identity intelligence and device-risk context are central to the fraud stack. Buyers should treat it as part of a broader decisioning environment rather than assuming it will cover every fraud workflow alone.

What to consider:

Implementation and value may depend on existing identity, authentication, and fraud infrastructure.

Teams should evaluate how easily ThreatMetrix signals translate into operational workflows, especially if they need broader case management, AML support, or end-to-end orchestration.

Best for: LexisNexis ThreatMetrix is best for enterprises, banks, insurers, and digital platforms that need digital identity intelligence and device-risk insights at scale.

How to Shortlist the Right Fraud Detection Platform

By this point, you already have a sense of how the top fraud detection tools differ. The next step is to match those differences to your actual fraud journey.

Start by identifying where fraud creates the most pressure:

For a fintech, that may be fake accounts, mule activity, account takeover, or suspicious transactions.

For an e-commerce business, it may be chargebacks, refund abuse, promo abuse, or payment fraud.

For a bank, it may involve AML fraud detection, behavioral analytics, audit trails, and real-time transaction monitoring.

For instance, e-commerce operators discuss chargeback losses, dispute tools, fraud filters, address matching, delayed capture, and the risk of losing legitimate orders while trying to block abuse. That is exactly why e-commerce teams should shortlist platforms that support payment-risk checks, policy-abuse detection, false-positive control, and review workflows together.

Once the core risks are clear, evaluate each platform against three practical questions:

Does it cover the workflows where fraud appears most often? Look across onboarding, login, account recovery, checkout, withdrawals, refunds, and repeat account activity.

Does it connect the right signals? Strong platforms combine identity, device, behavior, network, and transaction data instead of depending on one risk indicator.

Can your team act on the output quickly? Risk scores, rules, explanations, case queues, and step-up workflows should help analysts move faster without creating more manual review.

Shortlisting becomes easier when the evaluation moves from “which tool has more features?” to “which tool improves our fraud decisions?” The checklist below turns that thinking into a practical buying framework.

Fraud Detection Platform Buyer Checklist

Use this checklist to pressure-test each platform before adding it to your final shortlist. It helps you move beyond feature claims and focus on whether the tool can support your real fraud risks, workflows, and team capacity.

Evaluation area | Buyer question |

Fraud coverage | Does the tool cover our top fraud risks across onboarding, login, and transactions? |

Signal quality | Does it combine identity, device, behavior, network, and transaction data? |

Real-time decisions | Can it score and act on risk instantly? |

AI capability | Does AI improve detection, or is it just a positioning claim? |

Explainability | Can analysts understand why something was flagged? |

False positives | Can the tool reduce fraud without blocking genuine users? |

AML support | Does it support compliance-heavy workflows where needed? |

Workflow control | Can teams tune rules and thresholds without heavy engineering work? |

Integrations | Does it support APIs, SDKs, webhooks, and existing fraud systems? |

Proof points | Can the vendor show relevant case studies or measurable outcomes? |

If your team keeps running into the same problem across multiple tools, such as one tool for device checks, another for behavioral signals, another for transaction risk, and another for case review, it may be time to look at a more unified decisioning layer.

A platform like Bureau ID combines multiple fraud signals with decisioning and workflow capabilities, making investigations easier and reducing the operational burden of managing several separate tools.

Reduce Fraud With Unified Decisions

When risk signals sit in separate systems, teams lose time connecting identities, devices, behaviors, transactions, and account activity. That delay can lead to missed fraud, slower reviews, higher false positives, and unnecessary friction for genuine customers.

The next step is to evaluate whether your current stack gives you one clear risk decision when it matters most. If fraud shows up across onboarding, login, payments, withdrawals, refunds, account recovery, and repeat usage, a unified decisioning layer can help your team act faster and with more context.

Bureau ID helps teams bring identity, device, behavior, network, and transaction intelligence into one fraud risk decisioning platform. That means your team can detect risky users, uncover connected fraud patterns, reduce manual reviews, automate workflows, and make faster decisions across the customer lifecycle.

If your team is evaluating fraud detection platforms, schedule a demo with Bureau ID to see how unified risk decisioning can fit into your fraud, compliance, and customer onboarding workflows.

FAQs

1. What is the best fraud detection software in 2026?

The best fraud detection software in 2026 depends on the fraud risks a business needs to manage. Leading platforms include Bureau ID, Sift, SEON, BioCatch, Kount, Feedzai, DataVisor, Sardine, and LexisNexis ThreatMetrix. Strong solutions combine real-time risk scoring, identity signals, device intelligence, behavioral analytics, rules, machine learning, case workflows, and compliance reporting.

2. What features should I look for in fraud detection software?

Look for fraud detection software with real-time decisioning, risk scoring, device intelligence, behavioral analytics, machine learning, rules automation, case management, and clear reporting. The platform should also support API integrations, explainable decisions, false-positive reduction, and compliance needs across onboarding, login, payment, transaction, and account workflows.

3. What is the best fraud detection software for reducing fraud losses and false positives?

The best fraud detection software for reducing fraud losses and false positives combines real-time risk scoring, identity verification signals, device intelligence, behavioral analytics, and machine learning. Bureau ID balances strong detection capabilities with a seamless customer experience, helping teams make confident risk decisions, streamline investigations, and scale fraud operations effectively.

4. How does Bureau ID support fraud prevention?

Bureau ID helps organizations reduce fraud risk across onboarding, account access, payments, and transactions. Teams can use Bureau ID to make real-time risk decisions, identify suspicious behavior, link devices and identities, automate fraud rules, reduce false positives, and streamline investigation workflows.

5. What is the difference between fraud detection software and fraud prevention software?

Fraud detection software identifies suspicious activity across users, accounts, transactions, devices, and behaviors. Fraud prevention software helps businesses act on that risk by blocking, challenging, routing, or reviewing high-risk activity. Many modern platforms combine both capabilities through risk scoring, automation, and real-time decisioning.

6. How do I compare fraud detection software vendors?

Compare fraud detection software vendors by fraud type coverage, signal depth, real-time scoring, machine learning capability, device intelligence, workflow automation, case management, API flexibility, compliance reporting, and false-positive control. The right platform should fit your industry, transaction volume, risk model, and review process.

Fraud teams often lack clear, real-time decisions when fraud moves across signups, logins, payments, refunds, withdrawals, and account activity. A basic fraud alert may flag risk, but it rarely tells teams what to do next without slowing down genuine customers.

The best fraud detection software helps close that gap. It connects identity, device, behavior, transaction, network, and AML signals so teams can detect suspicious activity, reduce false positives, automate reviews, and act faster across the customer journey.

In this guide, we compare nine top fraud detection tools for 2026: Bureau ID, Sift, SEON, BioCatch, Kount, Feedzai, DataVisor, Sardine, and LexisNexis ThreatMetrix.

You will see where each platform fits best, what to look for in a fraud detection platform, and how to shortlist the right software for your fintech, banking, ecommerce, or marketplace risk stack.

Fraud Detection Software Comparison: Top Tools at a Glance

The best fraud detection software helps businesses detect suspicious users, transactions, accounts, and behaviors in real time. It combines risk scoring, identity signals, device intelligence, behavioral analytics, rules, and machine learning. Strong platforms help fraud teams prevent payment fraud, account takeover, fake accounts, promo abuse, and chargebacks while supporting faster decisions, fewer false positives, case review, and compliance reporting.

A fraud detection software comparison should start with fit, not feature count. The right platform depends on where fraud appears in your journey, such as onboarding, login, payment, account recovery, withdrawal, refund, or repeat account activity.

Tool | Core strength | Key consideration | Best for |

Bureau ID | Identity, device, behavior, network, and transaction signals | Best for teams replacing fragmented fraud tools | Unified fraud risk decisioning |

Sift | Account, payment, and abuse prevention | Check fit for deeper identity and AML needs | Digital fraud operations |

SEON | Email, phone, IP, device, and digital footprint signals | Strong when enrichment is central to the workflow | Data enrichment and fraud checks |

BioCatch | Behavioral biometrics and session intelligence | May need complementary identity or AML tools | Behavioral analytics |

Kount | Transaction risk and identity trust | Stronger for payment-heavy use cases | Payment and account fraud |

Feedzai | Transaction monitoring and risk operations | Often better suited for large institutions | Enterprise financial crime prevention |

DataVisor | Adaptive AI and cross-entity intelligence | Evaluate explainability and analyst usability | Unknown fraud pattern detection |

Sardine | Device, behavior, payment, and AML signals | Best fit for high-risk financial workflows | Fraud, payments, and compliance |

LexisNexis ThreatMetrix | Device, identity, and network intelligence | Works well as part of a broader risk stack | Digital identity intelligence |

This table gives you a quick shortlist, but it should not be the only basis for choosing a platform.

A strong fraud detection platform also needs to match your fraud patterns, internal workflows, transaction volume, compliance needs, and review process. This broader coverage matters because the FBI's 2025 Internet Crime Report accounted for 452,868 cyber-enabled fraud complaints and $17.697 billion in losses in 2025, representing 45% of complaints and 85% of reported losses.

That is why the selection criteria matter as much as the vendor list.

How We Selected the Best Fraud Detection Tools

Selecting the best fraud detection software requires buyers to understand how each tool collects signals, scores risk, explains decisions, reduces false positives, and fits into existing workflows.

For this fraud prevention software review, we looked at practical buying criteria that matter to teams already comparing platforms:

Real-time fraud monitoring: The platform should score risk during onboarding, login, payment, withdrawal, account recovery, and profile changes.

AI and machine learning: The tool should detect known and emerging fraud patterns without relying only on static rules.

Identity, device, and behavioral signals: Strong tools combine who the user is, what device they use, how they behave, and whether the activity matches past patterns.

Network intelligence: The platform should uncover linked accounts, repeat devices, fraud rings, mule activity, or coordinated attacks.

AML and compliance support: Regulated teams should check transaction monitoring, audit trails, sanctions workflows, and mule-risk signals.

False-positive control: The tool should stop fraud without rejecting too many genuine users.

Workflow usability: Analysts should review risk reasons, tune rules, prioritize cases, and take action quickly.

Integration flexibility: APIs, SDKs, webhooks, and case-management compatibility matter for deployment speed.

For payment-heavy teams, features like real-time monitoring are becoming more urgent. In fact, MRC’s 2026 Global Payments and Fraud Report found that 45% of merchants named real-time payment fraud as the next biggest fraud attack overall.

The strongest platforms usually connect multiple risk signals and turn them into decisions that fraud, compliance, and operations teams can actually use. That difference matters when the goal is to act on fraud quickly without adding more manual review or customer friction.

Related Read: A Buyer’s Guide To Fraud Detection Software For Fintech Teams

9 Best Fraud Detection Software in 2026

Each tool below solves a different part of the fraud problem, from payment fraud and account takeover to behavioral analytics, AML workflows, and unified risk decisioning. Use these reviews to understand where each platform fits best and what to consider before adding it to your shortlist.

1. Bureau ID

Bureau ID is a unified risk decisioning platform built for businesses that need fraud detection across onboarding, authentication, transactions, payments, and ongoing account activity. It brings identity, device, behavior, network, and transaction signals into one decisioning layer, helping fraud teams detect risky users faster, reduce false positives, automate workflows, and avoid managing separate tools for every fraud use case.

Key strengths:

Unified risk visibility: Bureau ID connects identity, device, behavior, network, and transaction signals so teams can see risk across the full customer journey instead of reviewing isolated alerts.

Real-time decisions: The platform helps teams score users, devices, accounts, and transactions in real time, which is useful when fraud needs to be stopped before money moves or access is granted.

Explainable risk scores: It gives fraud, compliance, and operations teams clearer reasons behind risk decisions, making it easier to review cases, tune rules, and justify actions internally.

Workflow customization: No-code and low-code configuration helps teams adjust fraud rules, thresholds, and decision flows without depending on engineering for every operational change.

Fraud network detection: It also helps uncover linked identities, devices, accounts, and transactions, making it useful for detecting fraud rings, mule activity, synthetic identities, and repeat offenders.

Lower operational load: By consolidating signals and automating decisions, Bureau ID helps teams reduce manual reviews while still protecting genuine users from unnecessary friction.

Why Bureau ID stands out:

Uses alternate data, device intelligence, behavioral biometrics, identity verification, graph intelligence, and contextual decisioning in one risk decisioning layer.

Analyzes device risk using 160+ signals, including rooted devices, emulator usage, and spoofed environments.

Maps connections between users, devices, IPs, behaviors, and transactions to uncover collusion and fraud rings at scale.

Supports real-time, explainable scoring models that help teams act on risk without relying only on post-transaction reviews.

These capabilities make Bureau ID especially useful for teams that need to stop fraud before damage happens, not just investigate it after the fact. A strong example is Bureau ID’s work with a leading proptech company that was dealing with chargeback fraud on credit card rent payments.

Case study: How a leading proptech saved $1.25M in chargeback fraud with Bureau ID

The proptech company offered credit card rent payments for user convenience, but fraudsters abused the flow through fake chargebacks. Existing controls were reactive, fragmented, and hard to explain, allowing chargeback fraud to escalate after transactions were completed.

What Bureau ID implemented:

Built a real-time, explainable risk scoring system using Bureau ID’s Alternate Data.

Evaluated user trustworthiness and transaction risk using 200+ live signals.

Used signals such as telco metadata, UPI integrity, email quality, identity consistency, transaction attributes, and digital footprint.

Segmented users into low-risk, moderate-risk, and high-risk bands.

Restricted risky users from sensitive flows such as credit card rent payments.

Results achieved:

Prevented $1.25M in chargeback fraud in three months.

Reduced false chargeback rates from 40% to 8%.

Stopped 1,200+ high-risk transactions before payment.

Flagged 60,000+ users as high-risk for chargeback fraud.

Enabled sub-150ms scoring latency for faster risk decisions.

Read the full case study here → A Leading PropTech Saves $1.25M in Chargeback Fraud

Bureau ID is a strong fit when fraud risk cuts across multiple workflows, but teams should still evaluate how it fits their current stack and operating model.

What to consider:

Bureau ID is best suited for teams that want a broader fraud risk decisioning layer, not just a single-purpose fraud signal.

Teams with existing fraud tools should map where Bureau ID will replace, complement, or orchestrate current systems across onboarding, ATO, mule risk, bot detection, payment fraud, and transaction monitoring.

Best for: Bureau ID is best for fintechs, banks, marketplaces, ecommerce businesses, lenders, gaming platforms, and digital-first companies that need unified fraud risk decisioning across identity, device, behavior, network, and transaction signals.

2. Sift

Sift is a digital fraud prevention platform built for online businesses that need to detect account abuse, payment fraud, content abuse, and suspicious user activity. It uses machine learning and fraud workflow tools to help teams assess user and transaction risk across digital touchpoints, making it relevant for marketplaces, subscription platforms, ecommerce brands, and online services with high user volumes.

Key strengths:

Account abuse detection: Sift helps teams identify risky accounts, suspicious signups, and abusive user behavior before they create larger losses.

Payment fraud protection: The platform supports fraud decisions around transactions, chargebacks, and payment risk, which is useful for ecommerce and marketplace teams.

Machine-learning-based scoring: It uses machine learning to help teams detect suspicious behavior without depending only on static rules.

Fraud operations support: Case review and investigation workflows help analysts review risky users, understand patterns, and act faster.

Platform abuse coverage: It is also useful for businesses dealing with multiple abuse types, including payment fraud, account fraud, and content or policy abuse.

Sift works well for digital businesses that need broad fraud operations support across users, payments, and platform activity. Buyers should still check whether it gives them enough depth for identity, AML, or advanced orchestration needs.

What to consider:

Some G2 reviews note that Sift can occasionally generate false positives, which may increase review workload for fraud teams.

Buyers with deeper compliance or identity verification needs should assess whether Sift needs to be paired with other tools in the stack.

Best for: Sift is best for digital platforms, marketplaces, subscription businesses, and online services that need fraud prevention across user accounts, payments, and platform abuse.

3. SEON

SEON is a fraud prevention and AML compliance platform known for data enrichment, digital footprint checks, device intelligence, and flexible risk scoring. It helps teams evaluate users through signals such as email, phone, IP, device, and online presence, making it useful for businesses that need fast fraud checks during onboarding, login, payment, or account activity.

Key strengths:

Data enrichment: SEON helps teams build richer user profiles using email, phone, IP, device, and digital footprint data.

Fast fraud checks: The platform supports quick risk decisions during digital interactions, which helps teams respond before fraud moves downstream.

Flexible rules: Custom rules and scoring workflows help teams adapt fraud checks to their own risk patterns.

Device intelligence: It can help detect multi-accounting, account takeover, onboarding abuse, and suspicious device behavior.

Accessible usability: SEON is often positioned as easy to use for teams that want fraud checks without heavy implementation complexity.

SEON is strong when enrichment and flexible rules sit at the center of the fraud workflow. Teams should still evaluate whether enrichment alone is enough for their broader risk, compliance, or behavioral analytics needs.

What to consider:

Buyers should assess whether they also need deeper behavioral biometrics, AML workflows, or orchestration.

Some users suggest that SEON’s initial setup can require a learning curve, especially for teams trying to use advanced features well.

Best for: SEON is best for businesses that need flexible fraud checks using email, phone, IP, device, and digital footprint intelligence.

4. BioCatch

BioCatch focuses on behavioral biometrics and user-session intelligence. It analyzes how users interact with their devices, including typing rhythm, mouse movement, touchscreen behavior, session flow, and other behavior patterns. This makes it especially useful for banks and financial institutions that need to detect account takeover, scams, mule activity, and suspicious sessions.

Key strengths:

Behavioral biometrics: BioCatch helps teams detect suspicious activity by analyzing how users behave during digital sessions.

Account takeover detection: The platform can identify risk even when a user appears to have valid credentials.

Scam and mule-risk signals: Behavioral intelligence can help uncover unusual patterns linked to scams, social engineering, and mule activity.

Session-level insight: Teams can assess risk during the customer session, not only after a transaction has happened.

Low-friction detection layer: Behavioral signals add fraud context without necessarily forcing every user through extra verification.

BioCatch is valuable when behavioral analytics is the missing layer in a fraud stack. It is especially relevant for financial institutions, but buyers should check how it fits with identity, device, transaction, and AML systems.

What to consider:

Since BioCatch is behavioral-signal focused, teams may still need complementary identity, device, transaction monitoring, or AML tools.

Some PeerSpot commentary suggests that model decision-making in BioCatch can feel complex and not fully transparent for users reviewing outcomes.

Best for: BioCatch is best for banks and financial institutions that need behavioral analytics to detect account takeover, scams, mule activity, and suspicious user sessions.

5. Kount

Kount is a fraud detection and prevention platform focused on digital identity trust, payment fraud, account fraud, and transaction risk. It helps businesses make real-time risk decisions around payments, account activity, and customer interactions, making it relevant for retailers, ecommerce businesses, digital platforms, and transaction-heavy companies.

Key strengths:

Payment fraud detection: Kount helps businesses assess transaction risk and reduce exposure to fraudulent payments.

Chargeback protection: The platform supports teams trying to lower chargebacks and improve payment approval quality.

Identity trust signals: It helps distinguish trusted customers from risky activity using identity and transaction context.

Automated fraud checks: Rules and automation can reduce the volume of transactions that require manual review.

Transaction-focused decisioning: It is also useful for businesses where payment risk is one of the most urgent fraud problems.

Kount is a practical fit for businesses where payment fraud, chargebacks, and transaction risk are central concerns. Buyers should still assess whether it covers non-payment fraud needs deeply enough.

What to consider:

A G2 review notes that Kount’s configuration process can be complex and may require time and attention to detail.

Buyers should check whether Kount covers non-payment fraud needs deeply enough.

Best for: Kount is best for payment-heavy businesses, retailers, ecommerce brands, digital platforms, and transaction-driven companies that need real-time payment and account-risk decisions.

6. Feedzai

Feedzai is an enterprise fraud and financial crime prevention platform built for banks, payment providers, fintechs, and large financial institutions. It supports real-time transaction monitoring, fraud scoring, scam detection, and risk operations, making it especially relevant for organizations with high transaction volumes and complex financial crime workflows.

Key strengths:

Enterprise transaction monitoring: Feedzai supports high-volume transaction screening and fraud monitoring for large financial institutions.

Financial crime coverage: It helps teams manage fraud and financial crime risk across payment and banking workflows.

AI-based risk scoring: It uses AI to support fraud detection and help teams identify emerging patterns.

Risk operations support: Case management and investigation workflows help large teams review alerts and take action.

Regulated-market fit: The platform is useful for organizations that need fraud controls aligned with compliance-heavy operating environments.

Feedzai is strong when scale, transaction monitoring, and financial crime coverage are the main priorities. It is usually a better fit for larger institutions than smaller teams with lighter fraud operations.

What to consider:

Buyers should evaluate deployment complexity, data requirements, and internal team readiness before shortlisting Feedzai.

Smaller teams may need to assess whether the platform is more advanced than their current operating model requires.

Best for: Feedzai is best for banks, payment networks, and large financial institutions that need enterprise-grade transaction monitoring and financial crime prevention.

7. DataVisor

DataVisor is an AI-native fraud and risk platform focused on real-time decisioning, adaptive AI, and cross-entity intelligence. It is often evaluated by organizations dealing with high-volume digital activity, unknown fraud patterns, coordinated attacks, and fraud rings that static rules may miss.

Key strengths:

Unknown fraud detection: DataVisor helps teams identify emerging fraud patterns that may not match existing rules.

Adaptive AI: It supports machine-learning-led detection for fast-changing attacks and complex fraud behavior.

Cross-entity intelligence: The platform helps connect accounts, users, devices, transactions, and behaviors to uncover coordinated activity.

Real-time scoring: It supports fast risk scoring for digital activity and transaction flows.

Fraud ring detection: It is also useful for teams dealing with organized attacks, repeat offenders, and linked suspicious accounts.

DataVisor is compelling for teams that need to detect fraud patterns before they become obvious. It works best when the business has enough data maturity and analyst capacity to act on model-driven insights.

What to consider:

Some users suggest that DataVisor setup and integration can be complex, especially for smaller teams without deep technical resources.

Buyers should check how easily analysts can interpret and act on model outputs.

Best for: DataVisor is best for enterprises and digital platforms that need to detect unknown fraud patterns, coordinated attacks, and fraud rings at scale.

8. Sardine

Sardine is a fraud and compliance platform used by digital finance, payments, and high-risk businesses. It combines device intelligence, behavioral biometrics, payment-risk scoring, AML workflows, and transaction monitoring, making it relevant for teams that want fraud and compliance signals in one risk workflow.

Key strengths:

Fraud and AML coverage: Sardine helps teams connect fraud prevention with compliance-heavy workflows such as AML monitoring.

Device and behavioral signals: The platform uses device intelligence and behavioral biometrics to help identify risky activity.

Payment-risk scoring: It supports payment and account-risk decisions for financial and high-risk digital environments.

Real-time monitoring: Teams can assess risk across onboarding, login, account funding, payments, and ongoing activity.

High-risk workflow fit: It is useful for fintechs, crypto platforms, payment businesses, and other teams with fast-moving fraud risk.

Sardine is strong when teams need fraud, payments, and compliance signals together. Buyers should still check whether the platform’s depth and pricing model fit their exact risk workflow and budget.

What to consider:

Buyers should evaluate how its AML and fraud workflows align with their internal compliance model.

Teams outside fintech, crypto, payments, or high-risk financial workflows should assess whether Sardine is broader than they need.

Best for: Sardine is best for fintechs, crypto platforms, payments companies, and high-risk digital finance businesses that need fraud and compliance signals together.

9. LexisNexis ThreatMetrix

LexisNexis ThreatMetrix is a digital identity intelligence and fraud prevention solution used to assess risk across devices, identities, locations, and digital interactions. It helps enterprises build trust decisions using device intelligence, identity context, and network signals, making it relevant for large organizations with complex authentication and fraud prevention needs.

Key strengths:

Digital identity intelligence: ThreatMetrix helps teams assess whether a user, device, or interaction can be trusted.

Device-risk insight: The platform analyzes device, location, and network signals to support fraud and authentication decisions.

Network intelligence: LexisNexis Digital Identity Network helps enrich fraud decisions with shared risk context.

Risk-based authentication support: Teams can use ThreatMetrix signals to challenge high-risk users while reducing friction for trusted users.

Enterprise-scale fit: It also works well for large organizations that need identity-risk context across multiple channels.

ThreatMetrix is useful when identity intelligence and device-risk context are central to the fraud stack. Buyers should treat it as part of a broader decisioning environment rather than assuming it will cover every fraud workflow alone.

What to consider:

Implementation and value may depend on existing identity, authentication, and fraud infrastructure.

Teams should evaluate how easily ThreatMetrix signals translate into operational workflows, especially if they need broader case management, AML support, or end-to-end orchestration.

Best for: LexisNexis ThreatMetrix is best for enterprises, banks, insurers, and digital platforms that need digital identity intelligence and device-risk insights at scale.

How to Shortlist the Right Fraud Detection Platform

By this point, you already have a sense of how the top fraud detection tools differ. The next step is to match those differences to your actual fraud journey.

Start by identifying where fraud creates the most pressure:

For a fintech, that may be fake accounts, mule activity, account takeover, or suspicious transactions.

For an e-commerce business, it may be chargebacks, refund abuse, promo abuse, or payment fraud.

For a bank, it may involve AML fraud detection, behavioral analytics, audit trails, and real-time transaction monitoring.

For instance, e-commerce operators discuss chargeback losses, dispute tools, fraud filters, address matching, delayed capture, and the risk of losing legitimate orders while trying to block abuse. That is exactly why e-commerce teams should shortlist platforms that support payment-risk checks, policy-abuse detection, false-positive control, and review workflows together.

Once the core risks are clear, evaluate each platform against three practical questions:

Does it cover the workflows where fraud appears most often? Look across onboarding, login, account recovery, checkout, withdrawals, refunds, and repeat account activity.

Does it connect the right signals? Strong platforms combine identity, device, behavior, network, and transaction data instead of depending on one risk indicator.

Can your team act on the output quickly? Risk scores, rules, explanations, case queues, and step-up workflows should help analysts move faster without creating more manual review.

Shortlisting becomes easier when the evaluation moves from “which tool has more features?” to “which tool improves our fraud decisions?” The checklist below turns that thinking into a practical buying framework.

Fraud Detection Platform Buyer Checklist

Use this checklist to pressure-test each platform before adding it to your final shortlist. It helps you move beyond feature claims and focus on whether the tool can support your real fraud risks, workflows, and team capacity.

Evaluation area | Buyer question |

Fraud coverage | Does the tool cover our top fraud risks across onboarding, login, and transactions? |

Signal quality | Does it combine identity, device, behavior, network, and transaction data? |

Real-time decisions | Can it score and act on risk instantly? |

AI capability | Does AI improve detection, or is it just a positioning claim? |

Explainability | Can analysts understand why something was flagged? |

False positives | Can the tool reduce fraud without blocking genuine users? |

AML support | Does it support compliance-heavy workflows where needed? |

Workflow control | Can teams tune rules and thresholds without heavy engineering work? |

Integrations | Does it support APIs, SDKs, webhooks, and existing fraud systems? |

Proof points | Can the vendor show relevant case studies or measurable outcomes? |

If your team keeps running into the same problem across multiple tools, such as one tool for device checks, another for behavioral signals, another for transaction risk, and another for case review, it may be time to look at a more unified decisioning layer.

A platform like Bureau ID combines multiple fraud signals with decisioning and workflow capabilities, making investigations easier and reducing the operational burden of managing several separate tools.

Reduce Fraud With Unified Decisions

When risk signals sit in separate systems, teams lose time connecting identities, devices, behaviors, transactions, and account activity. That delay can lead to missed fraud, slower reviews, higher false positives, and unnecessary friction for genuine customers.

The next step is to evaluate whether your current stack gives you one clear risk decision when it matters most. If fraud shows up across onboarding, login, payments, withdrawals, refunds, account recovery, and repeat usage, a unified decisioning layer can help your team act faster and with more context.

Bureau ID helps teams bring identity, device, behavior, network, and transaction intelligence into one fraud risk decisioning platform. That means your team can detect risky users, uncover connected fraud patterns, reduce manual reviews, automate workflows, and make faster decisions across the customer lifecycle.

If your team is evaluating fraud detection platforms, schedule a demo with Bureau ID to see how unified risk decisioning can fit into your fraud, compliance, and customer onboarding workflows.

FAQs

1. What is the best fraud detection software in 2026?

The best fraud detection software in 2026 depends on the fraud risks a business needs to manage. Leading platforms include Bureau ID, Sift, SEON, BioCatch, Kount, Feedzai, DataVisor, Sardine, and LexisNexis ThreatMetrix. Strong solutions combine real-time risk scoring, identity signals, device intelligence, behavioral analytics, rules, machine learning, case workflows, and compliance reporting.

2. What features should I look for in fraud detection software?

Look for fraud detection software with real-time decisioning, risk scoring, device intelligence, behavioral analytics, machine learning, rules automation, case management, and clear reporting. The platform should also support API integrations, explainable decisions, false-positive reduction, and compliance needs across onboarding, login, payment, transaction, and account workflows.

3. What is the best fraud detection software for reducing fraud losses and false positives?

The best fraud detection software for reducing fraud losses and false positives combines real-time risk scoring, identity verification signals, device intelligence, behavioral analytics, and machine learning. Bureau ID balances strong detection capabilities with a seamless customer experience, helping teams make confident risk decisions, streamline investigations, and scale fraud operations effectively.

4. How does Bureau ID support fraud prevention?

Bureau ID helps organizations reduce fraud risk across onboarding, account access, payments, and transactions. Teams can use Bureau ID to make real-time risk decisions, identify suspicious behavior, link devices and identities, automate fraud rules, reduce false positives, and streamline investigation workflows.

5. What is the difference between fraud detection software and fraud prevention software?

Fraud detection software identifies suspicious activity across users, accounts, transactions, devices, and behaviors. Fraud prevention software helps businesses act on that risk by blocking, challenging, routing, or reviewing high-risk activity. Many modern platforms combine both capabilities through risk scoring, automation, and real-time decisioning.

6. How do I compare fraud detection software vendors?

Compare fraud detection software vendors by fraud type coverage, signal depth, real-time scoring, machine learning capability, device intelligence, workflow automation, case management, API flexibility, compliance reporting, and false-positive control. The right platform should fit your industry, transaction volume, risk model, and review process.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.