A Buyer’s Guide To Fraud Detection Software For Fintech Teams

A Buyer’s Guide To Fraud Detection Software For Fintech Teams

A Buyer’s Guide To Fraud Detection Software For Fintech Teams

Explore the best fraud detection software for fintech, compare key features, and learn how to evaluate platforms for your fraud risks.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

Fraud does not always break through the front door.

Sometimes it slips in through a clean-looking signup, a trusted account, a new device, or a transaction that moves faster than your team can review. That is when the bigger issue becomes clear: your fintech has scaled, but your fraud stack has not kept up.

This is why choosing the right fraud detection software for fintech matters. A point solution may catch payment fraud, support KYC, or flag account takeover. But when these tools do not work together, fraud teams deal with gaps, duplicate reviews, and slower decisions.

Bureau ID’s UK and EU Fraud Research found that 50%+ of organizations reported increased fraud exposure, while 83% observed AI or automation in attacks. The same report found that 67% say siloed systems prevent early signal correlation, which explains why fintech fraud stacks now need real-time detection, AI-aware risk scoring, synthetic identity checks, and account-level monitoring

This guide compares 6 leading fraud detection platforms for fintech. Before we get to the platforms, let’s first take a look at how we approached this evaluation.

How We Evaluated Fraud Detection Software for Fintech

A good fraud platform fits how your fintech actually operates, where fraud enters the journey, how fast decisions need to happen, and how much control your risk team needs after implementation.

For this comparison, we looked at the criteria that matter most during vendor evaluation.

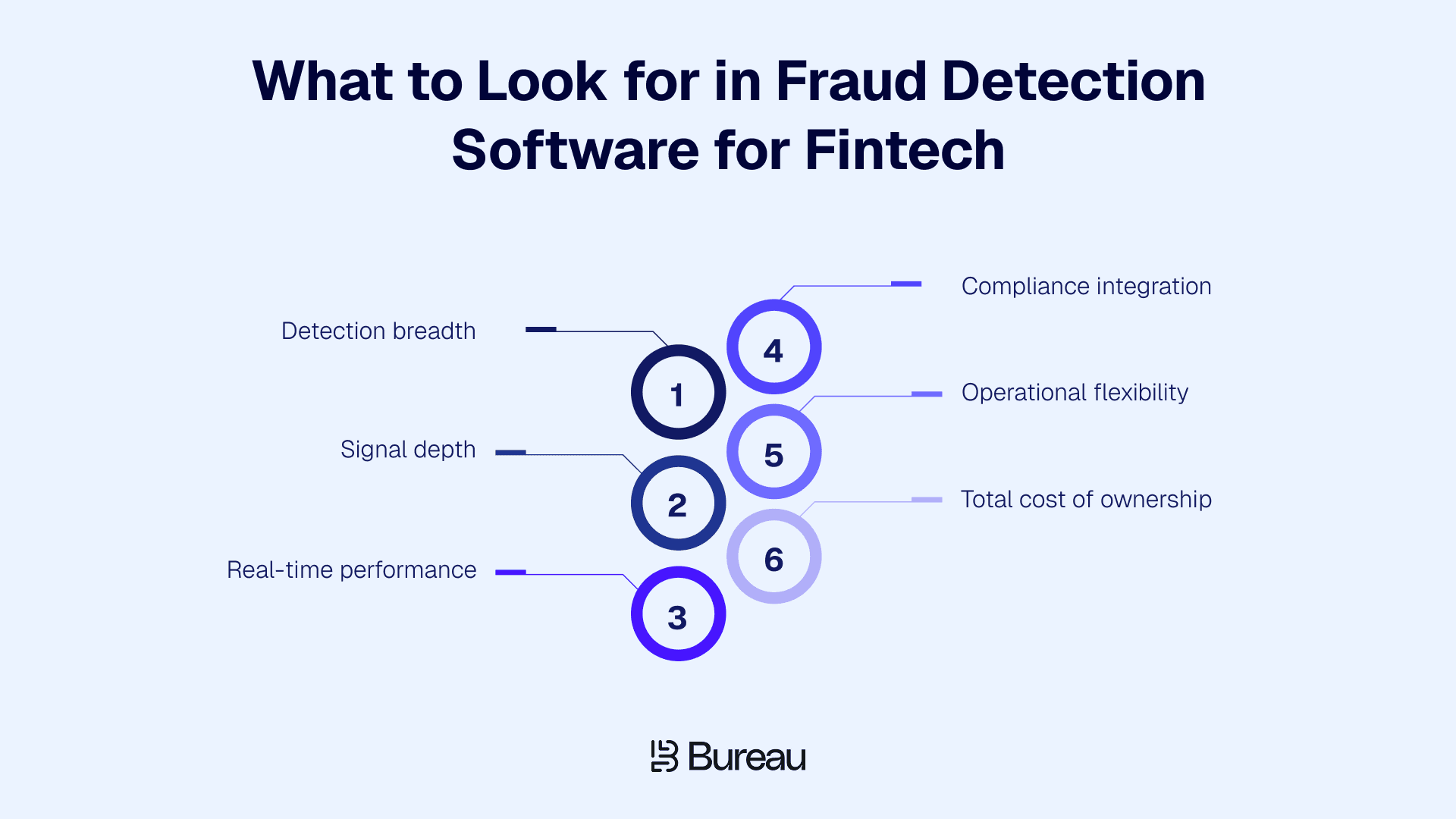

Detection breadth: Fraud rarely stays in one part of the customer journey. It can start at onboarding, show up during login, or surface during transactions. A strong anti-fraud platform should cover all three stages so your team does not have to stitch together separate tools for every risk point.

Signal depth: Fraudsters can work around basic checks when the system depends on one signal, such as IP, document verification, or device data alone. Stronger platforms combine identity, device intelligence, behavior, network, and transaction signals to create a more accurate risk score. This gives teams a fuller picture of the user, not just one isolated data point.

Real-time performance: Fintech products move quickly, especially in payments, wallets, lending, and BNPL. If a fraud decision takes too long, it can delay genuine users or let risky activity move forward. Real-time fraud detection helps teams act before the money moves, without adding unnecessary friction to every customer journey.

Compliance integration: Fraud, KYC, KYB, and AML teams often rely on overlapping signals. When those workflows sit in separate systems, teams spend more time reconciling data, reviewing duplicate alerts, and piecing together evidence. Platforms that connect fraud and compliance workflows create a cleaner audit trail and make investigations easier to manage.

Operational flexibility: Fraud patterns do not wait for engineering bandwidth. Risk teams need the ability to update rules, adjust thresholds, and respond to new attack patterns without depending on every change entering a development sprint. No-code or low-code workflows become especially useful when fraud teams need to act quickly.

Total cost of ownership: A lower license fee can still become expensive if the platform adds integration work, manual reviews, false declines, or vendor sprawl. Bureau ID’s 2026 India Fraud Report notes that UPI processed 228 billion transactions worth ₹300 trillion in 2025, showing how small fraud gaps can become costly at scale. Buyers should evaluate engineering time, operational effort, missed approvals, and fraud losses together.

The strongest platforms are the ones that balance fraud coverage, speed, compliance, and operational control without creating more work for the team using them. With that evaluation lens in place, it becomes easier to compare each tool based on fit rather than familiarity or brand recognition.

6 Best Fraud Detection Software for Fintech

Fraud detection software for fintech helps fintech companies detect, prevent, and investigate fraud across onboarding, accounts, payments, and transactions. The best tools help teams reduce payment fraud, prevent account takeover, detect synthetic identities, lower false positives, and protect customer trust without adding unnecessary friction.

Below are 6 fraud detection platforms worth evaluating.

1. Bureau ID

Bureau ID is an AI-powered Unified Risk Decisioning Platform that helps fintech teams verify users, detect fraud, and manage risk across onboarding, authentication, and transactions. It combines device intelligence, behavioral biometrics, identity verification, Graph Identity Network, and KYC/KYB/AML workflows into one decisioning layer.

Bureau ID serves 200+ global companies and uses a proprietary knowledge graph of 500M+ identities to detect connected risk.

Key strengths:

Full-lifecycle fraud coverage: The platform supports fraud detection across onboarding, login, account access, and transaction journeys, which helps fintech teams avoid gaps between separate tools.

Graph Identity Network: It maps connections between devices, phone numbers, emails, accounts, behaviors, and transactions to uncover fraud rings, mule networks, and synthetic identities that may look clean in isolation.

Persistent Device ID: It uses device intelligence to detect suspicious device reuse, cloned apps, emulators, spoofed environments, and high-risk device behavior even when fraudsters try to appear as new users.

Real-time risk decisioning: Bureau ID combines identity, device, network, transaction, and behavioral signals to deliver risk decisions quickly enough for fintech journeys where onboarding speed and payment timing matter.

Compliance-ready workflows: The software supports KYC, KYB, and AML workflows across 195+ markets, helping regulated fintechs bring fraud and compliance signals into the same operating layer.

No-code workflow control: It also gives risk teams configurable workflows, rule tuning, thresholds, and approval or rejection logic without depending on engineering for every change.

These strengths matter most when fraud does not follow a single pattern. For fintech buyers, the test is whether these capabilities can work together when fraudsters use synthetic identities, spoofed devices, and fast-moving credit journeys.

The Jupiter Edge case shows how Bureau ID handled that challenge in practice.

How Bureau ID Helped Jupiter Edge Stop Synthetic ID Fraud

Challenge: Jupiter Edge, a BNPL micro-loan app, offered instant credit with minimal onboarding friction. Fraudsters exploited that flow using stolen IDs, app clones, and device spoofing to bypass checks, transact, and disappear before the existing risk setup could identify synthetic identities and device-based attacks.

Bureau ID’s solution:

Device intelligence and fingerprinting: Detected cloned apps, malicious apps, suspicious device reuse, and fraudulent IP or geolocation signals.

Alternate data checks: Cross-checked name, phone, and email signals to identify synthetic or mismatched identities.

Unified signal analysis: Combined identity, device, network, and behavioral signals to identify coordinated rings and anomalous clusters.

Real-time risk scoring: Enabled Jupiter Edge to act on high-confidence risk signals instantly while preserving onboarding speed for genuine users.

Results achieved:

500+ fraudsters blocked in one day: Bureau ID identified and helped block a coordinated fraud ring operating from a common location.

Money movement was prevented before abuse: Jupiter Edge closed credit lines before fraudsters could move funds.

Zero additional friction for genuine users: The platform kept risk decisions invisible for genuine users while challenging risky flows.

Faster detection-to-action cycle: Bureau ID helped Jupiter Edge identify attack patterns within a few hours of deployment and act before the fraud scaled.

You can read the full case study here → Stopping Synthetic ID Fraud to Protect BNPL Customers

Pricing model: The platform offers custom pricing based on use case, transaction volume, markets covered, and the specific fraud, identity, compliance, and transaction workflows a fintech needs.

Bureau ID is a strong fit for neobanks, digital lenders, BNPL platforms, payment processors, wallets, and cross-border fintechs that need full-lifecycle fraud protection instead of multiple point solutions.

For fintech teams that want to reduce synthetic identity fraud, detect connected risk, prevent account takeover, and keep onboarding friction low, the software helps bring risk decisions into one workflow. Schedule a demo with Bureau ID to map the right fraud stack for your use case, volume, and market.

2. Sift

Sift is a digital fraud prevention platform that helps businesses detect account takeover, payment fraud, policy abuse, and other forms of online risk. Its platform is powered by a global data network of around 1 trillion annual events across 700+ brands, which helps teams identify suspicious behavior across users, accounts, and transactions at scale.

Key strengths:

Broad digital fraud coverage: Covers account takeover, payment fraud, and first-party abuse, which makes it useful for digital businesses that want one platform for multiple fraud use cases.

Cross-account intelligence: Connects user, account, and transaction signals to help detect coordinated fraud patterns across large digital ecosystems.

Real-time risk decisioning: Evaluates risk quickly across user journeys, helping teams stop suspicious activity before it turns into financial or reputational damage.

Strong marketplace and platform fit: Works well for online marketplaces, SaaS platforms, and high-volume digital businesses where fraud often moves across accounts, payments, and policy abuse.

Machine learning and behavioral analysis: Sift’s account takeover prevention uses machine learning and behavioral analysis to detect fraudulent logins and compare activity with patterns of good and bad behavior.

While Sift offers strong cross-account fraud detection, teams should evaluate where they need the most protection:

Sift’s broader fraud coverage can be useful, but teams may need careful configuration to avoid noisy rules or unnecessary reviews.

For businesses that need deeper identity verification, device-first risk detection, and lifecycle orchestration from onboarding through transactions, a more unified risk decisioning platform may be a better fit.

Pricing model: Sift usually follows a custom pricing model based on business needs, use case, and volume. Pricing is typically handled through a demo-led sales process.

Use case fit: Sift is a good fit for digital consumer platforms, marketplaces, subscription businesses, and fintech-adjacent companies. However, it may be less suitable for regulated fintechs that need deep native KYC, KYB, or AML workflows in the same platform.

3. Sardine

Sardine is a fraud and compliance platform built for fintech, crypto, and embedded finance companies. It combines device intelligence, behavioral signals, transaction monitoring, and AML support, making it relevant for teams that want fraud and compliance workflows to operate closer together across onboarding and payment journeys.

Key strengths:

Fraud and compliance alignment: Sardine brings fraud detection and AML workflows closer together, which helps reduce handoffs between risk and compliance teams.

Device and behavioral signals: The software uses device and behavioral data to identify risky users, suspicious sessions, and abnormal activity patterns.

Transaction monitoring support: It helps teams monitor financial activity and detect suspicious money movement across fintech and crypto use cases.

Crypto and embedded finance fit: It is relevant for crypto platforms, fintech infrastructure companies, BNPL providers, and embedded finance businesses.

Real-time risk decisioning: Sardine also supports real-time fraud decisions, which is useful for fintech products where money movement happens quickly.

While Sardine is strong for fraud and compliance convergence, teams should evaluate how well it fits their operating model:

Sardine can be especially useful for crypto, payments, and embedded finance teams with high transaction velocity.

Teams that need broader identity graph intelligence, lifecycle orchestration, or global KYC/KYB coverage should compare how Sardine fits against unified risk decisioning platforms.

Pricing model: Sardine uses custom pricing based on use case, transaction volume, and platform requirements.

Use case fit: Sardine is a strong fit for crypto platforms, BNPL companies, embedded finance providers, and fintechs. It is especially relevant for companies managing fast-moving transactions and AML-related risk.

4. Feedzai

Feedzai is an enterprise RiskOps platform built for banks, financial institutions, and large fintechs with complex fraud and AML requirements. It combines fraud prevention, AML, machine learning, rules, behavioral analytics, and case management to help teams monitor risk across multiple channels and jurisdictions.

Key strengths:

Enterprise fraud coverage: The platform supports large-scale fraud operations across payments, accounts, channels, and customer journeys.

Fraud and AML integration: Feedzai brings fraud prevention and AML workflows into one operating model, helping reduce operational silos.

Adaptive machine learning: It uses machine learning and behavioral analytics to identify anomalies and improve risk detection over time.

Rules and case management: It gives risk teams tools to define rules, manage alerts, review cases, and support fraud investigations.

Multi-channel support: Feedzai is suited for financial institutions that need fraud monitoring across digital banking, payments, cards, and other channels.

While Feedzai offers enterprise-grade depth, teams should evaluate whether they need that level of complexity:

Feedzai can be powerful for teams with complex AML, fraud, and case management needs.

Early-stage or mid-market fintechs may find the platform heavier than needed if they want faster deployment, simpler workflows, or lighter operational overhead.

Pricing model: Feedzai follows an enterprise pricing model, typically based on scale, use case complexity, and implementation requirements. It is usually better suited for larger institutions with mature fraud operations.

Use case fit: Feedzai is a good fit for large fintechs, banks, and financial institutions with multi-channel fraud, AML, and case management needs. It may be too complex or costly for early-stage fintechs that need a faster, lighter deployment.

5. SEON

SEON is an API-first fraud prevention platform known for digital footprinting and transparent risk scoring. It uses email, phone, IP, device, and online profile signals to help teams detect suspicious users, prevent account fraud, and make faster fraud decisions with a configurable rules engine.

Key strengths:

Digital footprinting: The software checks email, phone, IP, device, and online presence signals to help identify risky users.

Fast deployment: SEON is designed for quick implementation, making it useful for fintech startups and mid-market teams that need fraud controls without a long rollout.

Transparent scoring: It gives risk teams explainable scores, which makes it easier to understand why a user or transaction was flagged.

Custom rules engine: The platform lets teams create and tune fraud rules based on their own risk patterns and operational needs.

Cost-conscious fit: It can be practical for growing fintechs that need functional online fraud prevention tools without enterprise-level complexity.

While SEON is strong for digital footprinting and quick deployment, teams should evaluate how far their fraud needs extend:

SEON can be a practical fit for startups and mid-market businesses that need online fraud prevention tools quickly.

Teams with deeper transaction monitoring, AML, identity graph, or full-lifecycle orchestration needs may need to pair it with additional systems as they scale.

Pricing model: SEON offers usage-based and subscription-style pricing, with a free trial available in some cases. Pricing depends on volume, products used, and plan type.

Use case fit: SEON is a good fit for startups and mid-market fintechs that need fast, explainable fraud detection for onboarding and account-level risk. Teams may need additional tools if they require deep AML, transaction monitoring, or identity graph intelligence as they scale.

6. Alloy

Alloy is a risk decisioning and identity orchestration platform that helps fintechs manage onboarding, identity verification, KYC, KYB, fraud checks, and compliance workflows. It connects businesses to multiple third-party data providers through one hub, making it useful for onboarding-heavy fintech products.

Key strengths:

Identity orchestration: It connects fintech teams to multiple identity, fraud, compliance, and credit data providers through a single workflow.

KYC and KYB support: The platform is useful for businesses that need to verify individuals, businesses, beneficial owners, and compliance status during onboarding.

Custom decision workflows: Alloy helps teams create approval, rejection, and step-up flows based on risk rules and provider signals.

Data provider flexibility: It gives teams access to a pre-integrated provider network, which can reduce the effort of managing separate vendor integrations.

Onboarding-focused decisioning: It is strongest when fintechs need to make fast, reliable decisions at account opening or application submission.

While Alloy offers strong identity and compliance orchestration, teams should evaluate whether orchestration is the main gap they need to solve:

Alloy can be useful for fintechs that already rely on several data providers and want cleaner decision-making across them.

Teams that need deeper native fraud detection, device intelligence, behavioral biometrics, or network-level fraud ring detection may need to compare Alloy with more fraud-native risk platforms.

Pricing model: Alloy uses custom pricing based on transaction volume, use case, and data provider integrations. Total cost can vary depending on how many external checks and providers the workflow uses.

Use case fit: Alloy is a strong fit for digital lenders, BNPL companies, B2B fintechs, and onboarding-heavy platforms where KYC, KYB, and identity orchestration are primary needs. It may need to be paired with deeper fraud detection or transaction monitoring tools, depending on the company’s risk profile.

Fraud Detection Software Comparison: Side-by-Side

Once you’ve reviewed the individual platforms, the shortlist usually comes down to fit. A tool may look strong on paper, but the right choice depends on where fraud enters your user journey, how much compliance support you need, and how easily your risk team can act on the signals.

The table below maps each platform against the core evaluation criteria from earlier in this guide. Use it as a practical shortlisting tool before moving into demos, pricing conversations, or proof-of-concept testing.

Platform | Detection breadth | Signal depth | Real-time decisioning | Compliance built in | Best fit |

Bureau ID | Full lifecycle: onboarding, auth, transactions | Device, behavior, identity, network, transaction | Millisecond-level decisioning | KYC/KYB/AML across 195+ markets | Fintechs needing unified fraud and compliance |

Sift | Account abuse and payment fraud | Behavior, device, network signals | Real-time event scoring | Limited native compliance | Marketplaces, consumer platforms, payment fraud |

Sardine | Onboarding through transaction monitoring | Device, behavior, AML, transaction signals | Real-time | Compliance-first | Crypto, embedded finance, BNPL |

Feedzai | Full lifecycle and multi-channel | Behavioral analytics, device, ML, rules | Enterprise-grade real-time | Fraud and AML unified | Banks and large fintechs |

SEON | Onboarding and account fraud | Email, phone, IP, device, digital footprint | Real-time | Limited native AML | Startups and mid-market fintechs |

Alloy | Onboarding and credit risk | Identity data and third-party provider hub | Real-time at onboarding | KYC/KYB/AML orchestration | Lenders, BNPL, B2B fintechs |

This comparison gives you a cleaner way to narrow the field, but it should not be the final decision-maker. The actual test is whether a platform can catch your known fraud patterns, keep false positives under control, and fit into your existing product, compliance, and engineering workflows.

A strong shortlist should now be easier to build, but choosing between two or three serious contenders still requires a more structured evaluation. That is where use-case mapping, integration planning, and proof-of-concept testing become essential.

Related Read → The Key Reasons Fraud Continues to Outpace Defenses in the UK and EU

How to Evaluate a Fraud Prevention Platform for Fintech

Once you have a shortlist, the next question is “Which platform can handle our fraud patterns, work with our existing stack, and help the team move faster without hurting genuine users?”

A structured evaluation makes that decision much easier. It also helps you move vendor conversations away from generic demos and toward proof that the platform can solve your specific risk problems.

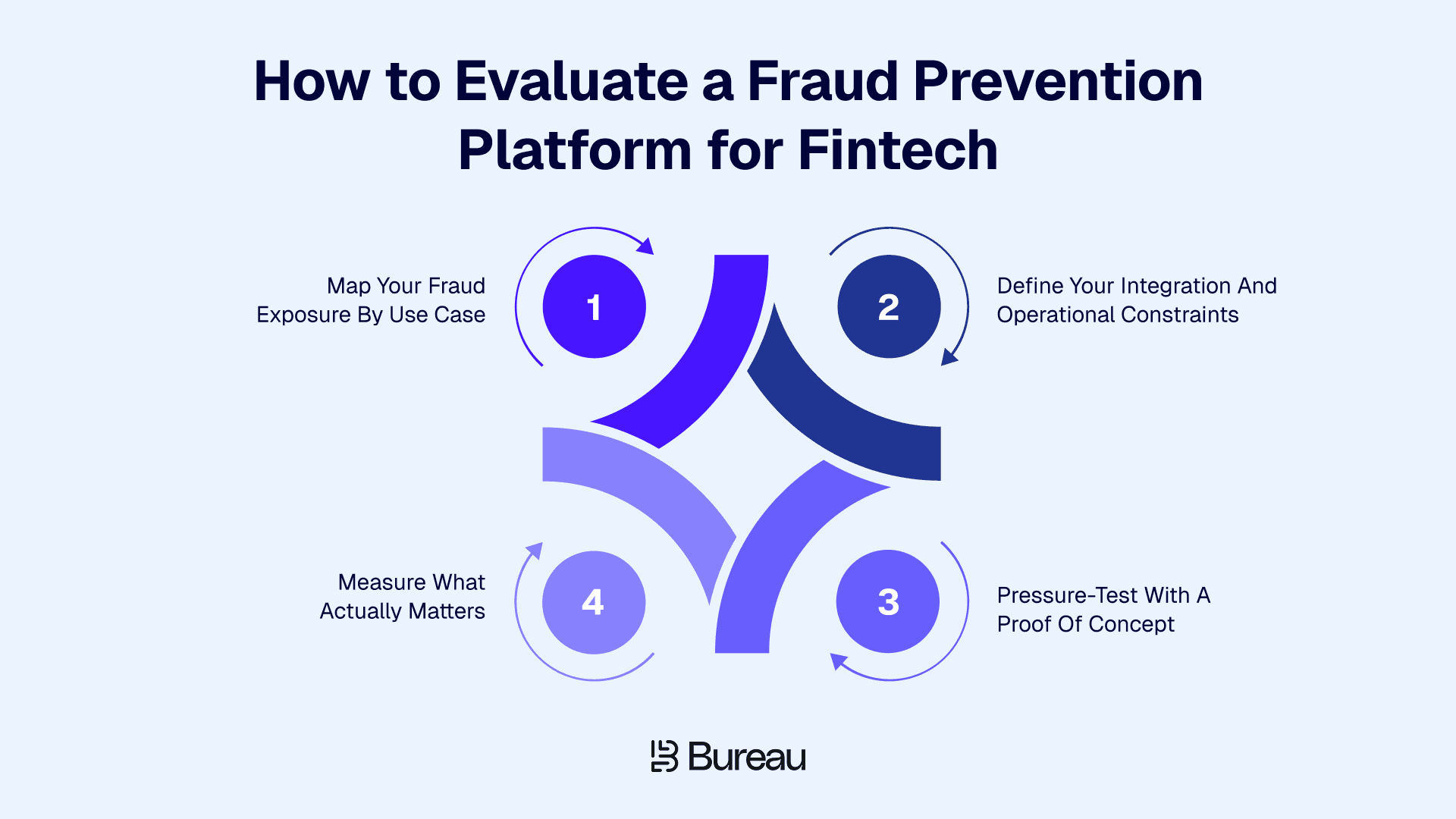

Step 1: Map Your Fraud Exposure by Use Case

Start with the fraud patterns you already see instead of the features a vendor wants to showcase. Pull your internal data by journey stage, such as onboarding, authentication, transactions, account changes, and payouts. Then group those incidents by attack vector and financial impact.

A simple template works well here:

Fraud type → Attack vector → Current detection gap → Financial impact per quarter

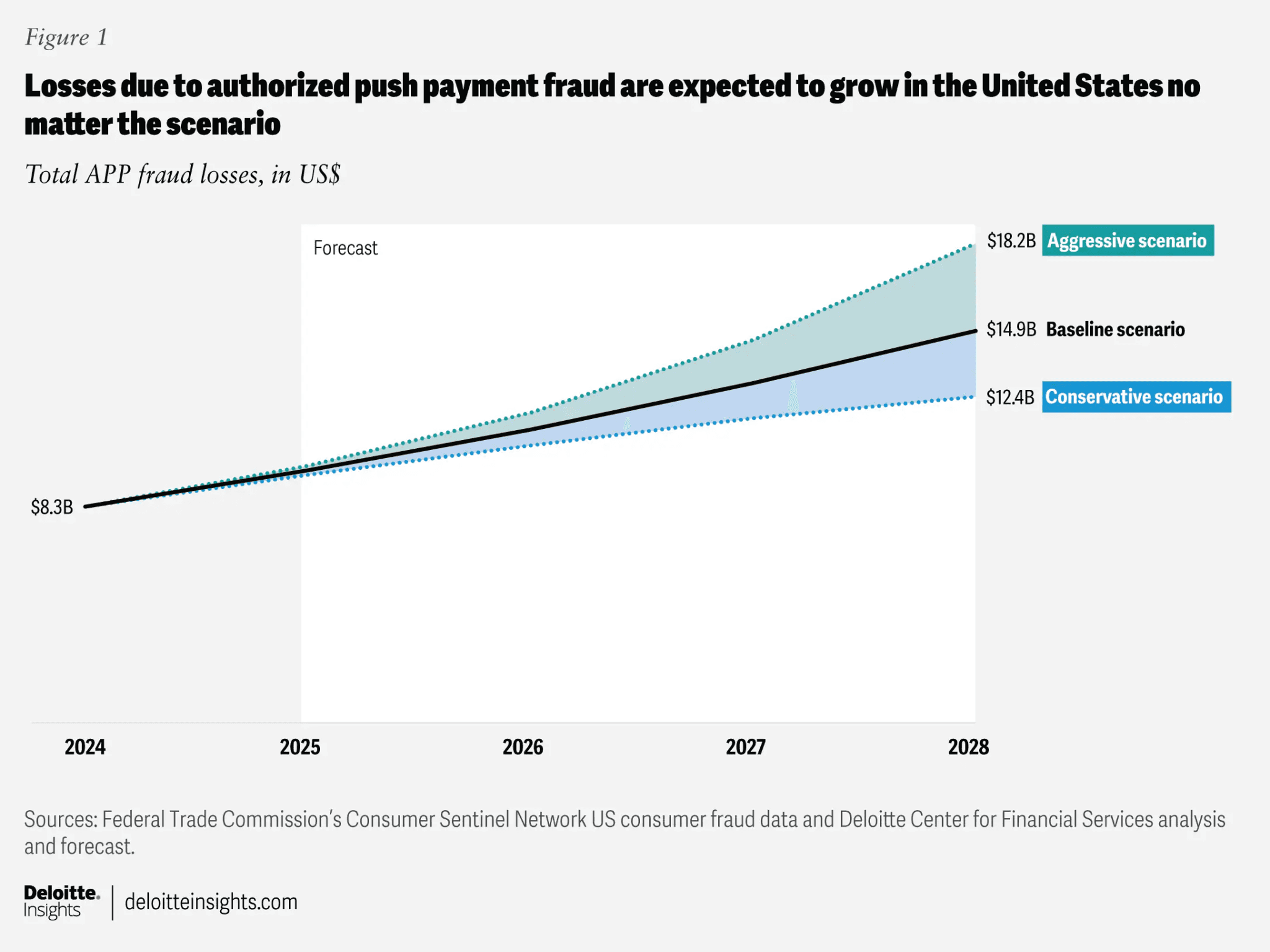

Synthetic identity fraud during BNPL onboarding needs a different evaluation lens than account takeover in a wallet product or chargeback abuse in payments. Authorized push payment fraud deserves the same level of attention, especially as Deloitte estimates U.S. APP fraud losses could rise from $8.3 billion in 2024 to $14.9 billion by 2028.

Image Source: Deloitte

The clearer your risk map is, the easier it becomes to see which platforms are relevant and which ones only look good on paper.

Step 2: Define Your Integration and Operational Constraints

Before you enter a proof of concept, be clear about what your team can realistically support. This includes engineering bandwidth, SDK or API preferences, no-code requirements, data residency rules, existing KYC providers, payment stack dependencies, and compliance review needs.

Two platforms can look almost identical in a comparison table, then feel completely different during implementation. Where a strong fraud detection API matters, so does usability. Risk teams should be able to tune rules, review flagged activity, understand decisions, and update workflows without waiting on engineering for every small change.

Step 3: Pressure-Test with a Proof of Concept

A good proof of concept should run on your own historical fraud cases and a clean sample of genuine users. Vendor demo data can show how the product works, but it rarely captures your customer behavior, fraud patterns, approval logic, latency needs, or compliance review process.

During the PoC, look at the detection rate, false positive rate, decision latency, and explainability. If your compliance team needs to review fraud decisions, ask how the platform shows the signals behind each outcome. If a vendor restricts what you can test or avoids your harder use cases, that tells you something useful before you commit.

Step 4: Measure What Actually Matters

The final decision should come down to measurable business outcomes, not just feature coverage. Fraud catch rate is important, but it should never sit alone. A system that catches more fraud while blocking too many genuine users can still hurt revenue, growth, and customer trust.

Track metrics such as false-positive rate, p99 latency, pass-rate improvement, manual-review volume, compliance-automation coverage, and time to rule change. These numbers show whether the platform improves risk control without creating new friction for customers or new work for the fraud team.

The right fraud prevention platform should make your team faster, your decisions clearer, and your customer journey safer. Once a tool proves that across your own data, use cases, and workflows, the decision becomes much easier to defend.

Build a Fraud Stack That Scales

Fraud stacks usually break at the point where growth starts to look good.

More users, more products, more markets, and more transactions all create more places for fraud to enter. If your tools only solve isolated problems, your team ends up managing gaps between onboarding, account access, payments, and compliance workflows.

That is why the next step is understanding whether your current stack can support the way your fintech is growing. For teams that need full-lifecycle fraud coverage, Bureau ID brings device intelligence, behavioral signals, identity verification, network intelligence, transaction monitoring, and KYC/KYB/AML workflows into one decisioning layer.

If you contact Bureau ID, the next steps would typically include:

Reviewing where fraud enters your customer journey.

Identifying gaps across fraud, identity, compliance, and transaction workflows.

Mapping the right capabilities to your use case, market, and volume.

Choosing the best integration path, such as API, SDK, or no-code workflows.

Defining success metrics like lower fraud losses, fewer false positives, and faster reviews.

If your fintech needs a fraud stack that can scale across onboarding, authentication, transactions, and compliance, schedule a demo with Bureau ID to see how the platform fits your use case.

FAQs

1. What is fraud detection software for fintech?

Fraud detection software for fintech helps fintech companies identify, prevent, and investigate suspicious activity across payments, accounts, onboarding, and transactions. It uses risk scoring, identity checks, device signals, transaction monitoring, behavioral analytics, and AI to flag fraud in real time. Some of the top choices include Bureau ID, Sift, Sardine, Feedzai, SEON, and Alloy.

2. How does fraud detection software work in fintech?

Fraud detection software collects signals from users, devices, transactions, accounts, and behavior. It then applies rules, AI models, and risk scores to detect suspicious activity. Fraud teams use alerts, case workflows, and decision records to review, approve, block, or escalate risky activity.

3. What features should fintech fraud detection software include?

Fintech fraud detection software should include real-time monitoring, risk scoring, identity verification, transaction monitoring, device intelligence, behavioral analytics, rule engines, AI models, case management, API integrations, and compliance support. These features help teams detect fraud without adding unnecessary friction.

4. What makes Bureau ID a good choice for fintech fraud detection?

Bureau ID is a good choice for fintech fraud detection when teams need identity, device, behavior, and risk signals to work together across onboarding and transaction journeys. It supports fraud checks for use cases such as account takeover, fake accounts, synthetic identity risk, mule activity, and payment fraud.

5. How can fintech companies detect fraud in real time?

Fintech companies can detect fraud in real time by monitoring transactions, logins, account changes, device signals, and user behavior as they happen. Real-time risk scoring helps teams flag suspicious payments, account takeover attempts, synthetic identities, scams, and money mule activity before losses increase.

6. How does AI improve fintech fraud detection?

AI improves fintech fraud detection by identifying patterns that static rules may miss. It helps detect unusual behavior, payment risk, account takeover attempts, synthetic identities, and scam signals. AI also supports faster investigations by prioritizing high-risk alerts for fraud teams.

Fraud does not always break through the front door.

Sometimes it slips in through a clean-looking signup, a trusted account, a new device, or a transaction that moves faster than your team can review. That is when the bigger issue becomes clear: your fintech has scaled, but your fraud stack has not kept up.

This is why choosing the right fraud detection software for fintech matters. A point solution may catch payment fraud, support KYC, or flag account takeover. But when these tools do not work together, fraud teams deal with gaps, duplicate reviews, and slower decisions.

Bureau ID’s UK and EU Fraud Research found that 50%+ of organizations reported increased fraud exposure, while 83% observed AI or automation in attacks. The same report found that 67% say siloed systems prevent early signal correlation, which explains why fintech fraud stacks now need real-time detection, AI-aware risk scoring, synthetic identity checks, and account-level monitoring

This guide compares 6 leading fraud detection platforms for fintech. Before we get to the platforms, let’s first take a look at how we approached this evaluation.

How We Evaluated Fraud Detection Software for Fintech

A good fraud platform fits how your fintech actually operates, where fraud enters the journey, how fast decisions need to happen, and how much control your risk team needs after implementation.

For this comparison, we looked at the criteria that matter most during vendor evaluation.

Detection breadth: Fraud rarely stays in one part of the customer journey. It can start at onboarding, show up during login, or surface during transactions. A strong anti-fraud platform should cover all three stages so your team does not have to stitch together separate tools for every risk point.

Signal depth: Fraudsters can work around basic checks when the system depends on one signal, such as IP, document verification, or device data alone. Stronger platforms combine identity, device intelligence, behavior, network, and transaction signals to create a more accurate risk score. This gives teams a fuller picture of the user, not just one isolated data point.

Real-time performance: Fintech products move quickly, especially in payments, wallets, lending, and BNPL. If a fraud decision takes too long, it can delay genuine users or let risky activity move forward. Real-time fraud detection helps teams act before the money moves, without adding unnecessary friction to every customer journey.

Compliance integration: Fraud, KYC, KYB, and AML teams often rely on overlapping signals. When those workflows sit in separate systems, teams spend more time reconciling data, reviewing duplicate alerts, and piecing together evidence. Platforms that connect fraud and compliance workflows create a cleaner audit trail and make investigations easier to manage.

Operational flexibility: Fraud patterns do not wait for engineering bandwidth. Risk teams need the ability to update rules, adjust thresholds, and respond to new attack patterns without depending on every change entering a development sprint. No-code or low-code workflows become especially useful when fraud teams need to act quickly.

Total cost of ownership: A lower license fee can still become expensive if the platform adds integration work, manual reviews, false declines, or vendor sprawl. Bureau ID’s 2026 India Fraud Report notes that UPI processed 228 billion transactions worth ₹300 trillion in 2025, showing how small fraud gaps can become costly at scale. Buyers should evaluate engineering time, operational effort, missed approvals, and fraud losses together.

The strongest platforms are the ones that balance fraud coverage, speed, compliance, and operational control without creating more work for the team using them. With that evaluation lens in place, it becomes easier to compare each tool based on fit rather than familiarity or brand recognition.

6 Best Fraud Detection Software for Fintech

Fraud detection software for fintech helps fintech companies detect, prevent, and investigate fraud across onboarding, accounts, payments, and transactions. The best tools help teams reduce payment fraud, prevent account takeover, detect synthetic identities, lower false positives, and protect customer trust without adding unnecessary friction.

Below are 6 fraud detection platforms worth evaluating.

1. Bureau ID

Bureau ID is an AI-powered Unified Risk Decisioning Platform that helps fintech teams verify users, detect fraud, and manage risk across onboarding, authentication, and transactions. It combines device intelligence, behavioral biometrics, identity verification, Graph Identity Network, and KYC/KYB/AML workflows into one decisioning layer.

Bureau ID serves 200+ global companies and uses a proprietary knowledge graph of 500M+ identities to detect connected risk.

Key strengths:

Full-lifecycle fraud coverage: The platform supports fraud detection across onboarding, login, account access, and transaction journeys, which helps fintech teams avoid gaps between separate tools.

Graph Identity Network: It maps connections between devices, phone numbers, emails, accounts, behaviors, and transactions to uncover fraud rings, mule networks, and synthetic identities that may look clean in isolation.

Persistent Device ID: It uses device intelligence to detect suspicious device reuse, cloned apps, emulators, spoofed environments, and high-risk device behavior even when fraudsters try to appear as new users.

Real-time risk decisioning: Bureau ID combines identity, device, network, transaction, and behavioral signals to deliver risk decisions quickly enough for fintech journeys where onboarding speed and payment timing matter.

Compliance-ready workflows: The software supports KYC, KYB, and AML workflows across 195+ markets, helping regulated fintechs bring fraud and compliance signals into the same operating layer.

No-code workflow control: It also gives risk teams configurable workflows, rule tuning, thresholds, and approval or rejection logic without depending on engineering for every change.

These strengths matter most when fraud does not follow a single pattern. For fintech buyers, the test is whether these capabilities can work together when fraudsters use synthetic identities, spoofed devices, and fast-moving credit journeys.

The Jupiter Edge case shows how Bureau ID handled that challenge in practice.

How Bureau ID Helped Jupiter Edge Stop Synthetic ID Fraud

Challenge: Jupiter Edge, a BNPL micro-loan app, offered instant credit with minimal onboarding friction. Fraudsters exploited that flow using stolen IDs, app clones, and device spoofing to bypass checks, transact, and disappear before the existing risk setup could identify synthetic identities and device-based attacks.

Bureau ID’s solution:

Device intelligence and fingerprinting: Detected cloned apps, malicious apps, suspicious device reuse, and fraudulent IP or geolocation signals.

Alternate data checks: Cross-checked name, phone, and email signals to identify synthetic or mismatched identities.

Unified signal analysis: Combined identity, device, network, and behavioral signals to identify coordinated rings and anomalous clusters.

Real-time risk scoring: Enabled Jupiter Edge to act on high-confidence risk signals instantly while preserving onboarding speed for genuine users.

Results achieved:

500+ fraudsters blocked in one day: Bureau ID identified and helped block a coordinated fraud ring operating from a common location.

Money movement was prevented before abuse: Jupiter Edge closed credit lines before fraudsters could move funds.

Zero additional friction for genuine users: The platform kept risk decisions invisible for genuine users while challenging risky flows.

Faster detection-to-action cycle: Bureau ID helped Jupiter Edge identify attack patterns within a few hours of deployment and act before the fraud scaled.

You can read the full case study here → Stopping Synthetic ID Fraud to Protect BNPL Customers

Pricing model: The platform offers custom pricing based on use case, transaction volume, markets covered, and the specific fraud, identity, compliance, and transaction workflows a fintech needs.

Bureau ID is a strong fit for neobanks, digital lenders, BNPL platforms, payment processors, wallets, and cross-border fintechs that need full-lifecycle fraud protection instead of multiple point solutions.

For fintech teams that want to reduce synthetic identity fraud, detect connected risk, prevent account takeover, and keep onboarding friction low, the software helps bring risk decisions into one workflow. Schedule a demo with Bureau ID to map the right fraud stack for your use case, volume, and market.

2. Sift

Sift is a digital fraud prevention platform that helps businesses detect account takeover, payment fraud, policy abuse, and other forms of online risk. Its platform is powered by a global data network of around 1 trillion annual events across 700+ brands, which helps teams identify suspicious behavior across users, accounts, and transactions at scale.

Key strengths:

Broad digital fraud coverage: Covers account takeover, payment fraud, and first-party abuse, which makes it useful for digital businesses that want one platform for multiple fraud use cases.

Cross-account intelligence: Connects user, account, and transaction signals to help detect coordinated fraud patterns across large digital ecosystems.

Real-time risk decisioning: Evaluates risk quickly across user journeys, helping teams stop suspicious activity before it turns into financial or reputational damage.

Strong marketplace and platform fit: Works well for online marketplaces, SaaS platforms, and high-volume digital businesses where fraud often moves across accounts, payments, and policy abuse.

Machine learning and behavioral analysis: Sift’s account takeover prevention uses machine learning and behavioral analysis to detect fraudulent logins and compare activity with patterns of good and bad behavior.

While Sift offers strong cross-account fraud detection, teams should evaluate where they need the most protection:

Sift’s broader fraud coverage can be useful, but teams may need careful configuration to avoid noisy rules or unnecessary reviews.

For businesses that need deeper identity verification, device-first risk detection, and lifecycle orchestration from onboarding through transactions, a more unified risk decisioning platform may be a better fit.

Pricing model: Sift usually follows a custom pricing model based on business needs, use case, and volume. Pricing is typically handled through a demo-led sales process.

Use case fit: Sift is a good fit for digital consumer platforms, marketplaces, subscription businesses, and fintech-adjacent companies. However, it may be less suitable for regulated fintechs that need deep native KYC, KYB, or AML workflows in the same platform.

3. Sardine

Sardine is a fraud and compliance platform built for fintech, crypto, and embedded finance companies. It combines device intelligence, behavioral signals, transaction monitoring, and AML support, making it relevant for teams that want fraud and compliance workflows to operate closer together across onboarding and payment journeys.

Key strengths:

Fraud and compliance alignment: Sardine brings fraud detection and AML workflows closer together, which helps reduce handoffs between risk and compliance teams.

Device and behavioral signals: The software uses device and behavioral data to identify risky users, suspicious sessions, and abnormal activity patterns.

Transaction monitoring support: It helps teams monitor financial activity and detect suspicious money movement across fintech and crypto use cases.

Crypto and embedded finance fit: It is relevant for crypto platforms, fintech infrastructure companies, BNPL providers, and embedded finance businesses.

Real-time risk decisioning: Sardine also supports real-time fraud decisions, which is useful for fintech products where money movement happens quickly.

While Sardine is strong for fraud and compliance convergence, teams should evaluate how well it fits their operating model:

Sardine can be especially useful for crypto, payments, and embedded finance teams with high transaction velocity.

Teams that need broader identity graph intelligence, lifecycle orchestration, or global KYC/KYB coverage should compare how Sardine fits against unified risk decisioning platforms.

Pricing model: Sardine uses custom pricing based on use case, transaction volume, and platform requirements.

Use case fit: Sardine is a strong fit for crypto platforms, BNPL companies, embedded finance providers, and fintechs. It is especially relevant for companies managing fast-moving transactions and AML-related risk.

4. Feedzai

Feedzai is an enterprise RiskOps platform built for banks, financial institutions, and large fintechs with complex fraud and AML requirements. It combines fraud prevention, AML, machine learning, rules, behavioral analytics, and case management to help teams monitor risk across multiple channels and jurisdictions.

Key strengths:

Enterprise fraud coverage: The platform supports large-scale fraud operations across payments, accounts, channels, and customer journeys.

Fraud and AML integration: Feedzai brings fraud prevention and AML workflows into one operating model, helping reduce operational silos.

Adaptive machine learning: It uses machine learning and behavioral analytics to identify anomalies and improve risk detection over time.

Rules and case management: It gives risk teams tools to define rules, manage alerts, review cases, and support fraud investigations.

Multi-channel support: Feedzai is suited for financial institutions that need fraud monitoring across digital banking, payments, cards, and other channels.

While Feedzai offers enterprise-grade depth, teams should evaluate whether they need that level of complexity:

Feedzai can be powerful for teams with complex AML, fraud, and case management needs.

Early-stage or mid-market fintechs may find the platform heavier than needed if they want faster deployment, simpler workflows, or lighter operational overhead.

Pricing model: Feedzai follows an enterprise pricing model, typically based on scale, use case complexity, and implementation requirements. It is usually better suited for larger institutions with mature fraud operations.

Use case fit: Feedzai is a good fit for large fintechs, banks, and financial institutions with multi-channel fraud, AML, and case management needs. It may be too complex or costly for early-stage fintechs that need a faster, lighter deployment.

5. SEON

SEON is an API-first fraud prevention platform known for digital footprinting and transparent risk scoring. It uses email, phone, IP, device, and online profile signals to help teams detect suspicious users, prevent account fraud, and make faster fraud decisions with a configurable rules engine.

Key strengths:

Digital footprinting: The software checks email, phone, IP, device, and online presence signals to help identify risky users.

Fast deployment: SEON is designed for quick implementation, making it useful for fintech startups and mid-market teams that need fraud controls without a long rollout.

Transparent scoring: It gives risk teams explainable scores, which makes it easier to understand why a user or transaction was flagged.

Custom rules engine: The platform lets teams create and tune fraud rules based on their own risk patterns and operational needs.

Cost-conscious fit: It can be practical for growing fintechs that need functional online fraud prevention tools without enterprise-level complexity.

While SEON is strong for digital footprinting and quick deployment, teams should evaluate how far their fraud needs extend:

SEON can be a practical fit for startups and mid-market businesses that need online fraud prevention tools quickly.

Teams with deeper transaction monitoring, AML, identity graph, or full-lifecycle orchestration needs may need to pair it with additional systems as they scale.

Pricing model: SEON offers usage-based and subscription-style pricing, with a free trial available in some cases. Pricing depends on volume, products used, and plan type.

Use case fit: SEON is a good fit for startups and mid-market fintechs that need fast, explainable fraud detection for onboarding and account-level risk. Teams may need additional tools if they require deep AML, transaction monitoring, or identity graph intelligence as they scale.

6. Alloy

Alloy is a risk decisioning and identity orchestration platform that helps fintechs manage onboarding, identity verification, KYC, KYB, fraud checks, and compliance workflows. It connects businesses to multiple third-party data providers through one hub, making it useful for onboarding-heavy fintech products.

Key strengths:

Identity orchestration: It connects fintech teams to multiple identity, fraud, compliance, and credit data providers through a single workflow.

KYC and KYB support: The platform is useful for businesses that need to verify individuals, businesses, beneficial owners, and compliance status during onboarding.

Custom decision workflows: Alloy helps teams create approval, rejection, and step-up flows based on risk rules and provider signals.

Data provider flexibility: It gives teams access to a pre-integrated provider network, which can reduce the effort of managing separate vendor integrations.

Onboarding-focused decisioning: It is strongest when fintechs need to make fast, reliable decisions at account opening or application submission.

While Alloy offers strong identity and compliance orchestration, teams should evaluate whether orchestration is the main gap they need to solve:

Alloy can be useful for fintechs that already rely on several data providers and want cleaner decision-making across them.

Teams that need deeper native fraud detection, device intelligence, behavioral biometrics, or network-level fraud ring detection may need to compare Alloy with more fraud-native risk platforms.

Pricing model: Alloy uses custom pricing based on transaction volume, use case, and data provider integrations. Total cost can vary depending on how many external checks and providers the workflow uses.

Use case fit: Alloy is a strong fit for digital lenders, BNPL companies, B2B fintechs, and onboarding-heavy platforms where KYC, KYB, and identity orchestration are primary needs. It may need to be paired with deeper fraud detection or transaction monitoring tools, depending on the company’s risk profile.

Fraud Detection Software Comparison: Side-by-Side

Once you’ve reviewed the individual platforms, the shortlist usually comes down to fit. A tool may look strong on paper, but the right choice depends on where fraud enters your user journey, how much compliance support you need, and how easily your risk team can act on the signals.

The table below maps each platform against the core evaluation criteria from earlier in this guide. Use it as a practical shortlisting tool before moving into demos, pricing conversations, or proof-of-concept testing.

Platform | Detection breadth | Signal depth | Real-time decisioning | Compliance built in | Best fit |

Bureau ID | Full lifecycle: onboarding, auth, transactions | Device, behavior, identity, network, transaction | Millisecond-level decisioning | KYC/KYB/AML across 195+ markets | Fintechs needing unified fraud and compliance |

Sift | Account abuse and payment fraud | Behavior, device, network signals | Real-time event scoring | Limited native compliance | Marketplaces, consumer platforms, payment fraud |

Sardine | Onboarding through transaction monitoring | Device, behavior, AML, transaction signals | Real-time | Compliance-first | Crypto, embedded finance, BNPL |

Feedzai | Full lifecycle and multi-channel | Behavioral analytics, device, ML, rules | Enterprise-grade real-time | Fraud and AML unified | Banks and large fintechs |

SEON | Onboarding and account fraud | Email, phone, IP, device, digital footprint | Real-time | Limited native AML | Startups and mid-market fintechs |

Alloy | Onboarding and credit risk | Identity data and third-party provider hub | Real-time at onboarding | KYC/KYB/AML orchestration | Lenders, BNPL, B2B fintechs |

This comparison gives you a cleaner way to narrow the field, but it should not be the final decision-maker. The actual test is whether a platform can catch your known fraud patterns, keep false positives under control, and fit into your existing product, compliance, and engineering workflows.

A strong shortlist should now be easier to build, but choosing between two or three serious contenders still requires a more structured evaluation. That is where use-case mapping, integration planning, and proof-of-concept testing become essential.

Related Read → The Key Reasons Fraud Continues to Outpace Defenses in the UK and EU

How to Evaluate a Fraud Prevention Platform for Fintech

Once you have a shortlist, the next question is “Which platform can handle our fraud patterns, work with our existing stack, and help the team move faster without hurting genuine users?”

A structured evaluation makes that decision much easier. It also helps you move vendor conversations away from generic demos and toward proof that the platform can solve your specific risk problems.

Step 1: Map Your Fraud Exposure by Use Case

Start with the fraud patterns you already see instead of the features a vendor wants to showcase. Pull your internal data by journey stage, such as onboarding, authentication, transactions, account changes, and payouts. Then group those incidents by attack vector and financial impact.

A simple template works well here:

Fraud type → Attack vector → Current detection gap → Financial impact per quarter

Synthetic identity fraud during BNPL onboarding needs a different evaluation lens than account takeover in a wallet product or chargeback abuse in payments. Authorized push payment fraud deserves the same level of attention, especially as Deloitte estimates U.S. APP fraud losses could rise from $8.3 billion in 2024 to $14.9 billion by 2028.

Image Source: Deloitte

The clearer your risk map is, the easier it becomes to see which platforms are relevant and which ones only look good on paper.

Step 2: Define Your Integration and Operational Constraints

Before you enter a proof of concept, be clear about what your team can realistically support. This includes engineering bandwidth, SDK or API preferences, no-code requirements, data residency rules, existing KYC providers, payment stack dependencies, and compliance review needs.

Two platforms can look almost identical in a comparison table, then feel completely different during implementation. Where a strong fraud detection API matters, so does usability. Risk teams should be able to tune rules, review flagged activity, understand decisions, and update workflows without waiting on engineering for every small change.

Step 3: Pressure-Test with a Proof of Concept

A good proof of concept should run on your own historical fraud cases and a clean sample of genuine users. Vendor demo data can show how the product works, but it rarely captures your customer behavior, fraud patterns, approval logic, latency needs, or compliance review process.

During the PoC, look at the detection rate, false positive rate, decision latency, and explainability. If your compliance team needs to review fraud decisions, ask how the platform shows the signals behind each outcome. If a vendor restricts what you can test or avoids your harder use cases, that tells you something useful before you commit.

Step 4: Measure What Actually Matters

The final decision should come down to measurable business outcomes, not just feature coverage. Fraud catch rate is important, but it should never sit alone. A system that catches more fraud while blocking too many genuine users can still hurt revenue, growth, and customer trust.

Track metrics such as false-positive rate, p99 latency, pass-rate improvement, manual-review volume, compliance-automation coverage, and time to rule change. These numbers show whether the platform improves risk control without creating new friction for customers or new work for the fraud team.

The right fraud prevention platform should make your team faster, your decisions clearer, and your customer journey safer. Once a tool proves that across your own data, use cases, and workflows, the decision becomes much easier to defend.

Build a Fraud Stack That Scales

Fraud stacks usually break at the point where growth starts to look good.

More users, more products, more markets, and more transactions all create more places for fraud to enter. If your tools only solve isolated problems, your team ends up managing gaps between onboarding, account access, payments, and compliance workflows.

That is why the next step is understanding whether your current stack can support the way your fintech is growing. For teams that need full-lifecycle fraud coverage, Bureau ID brings device intelligence, behavioral signals, identity verification, network intelligence, transaction monitoring, and KYC/KYB/AML workflows into one decisioning layer.

If you contact Bureau ID, the next steps would typically include:

Reviewing where fraud enters your customer journey.

Identifying gaps across fraud, identity, compliance, and transaction workflows.

Mapping the right capabilities to your use case, market, and volume.

Choosing the best integration path, such as API, SDK, or no-code workflows.

Defining success metrics like lower fraud losses, fewer false positives, and faster reviews.

If your fintech needs a fraud stack that can scale across onboarding, authentication, transactions, and compliance, schedule a demo with Bureau ID to see how the platform fits your use case.

FAQs

1. What is fraud detection software for fintech?

Fraud detection software for fintech helps fintech companies identify, prevent, and investigate suspicious activity across payments, accounts, onboarding, and transactions. It uses risk scoring, identity checks, device signals, transaction monitoring, behavioral analytics, and AI to flag fraud in real time. Some of the top choices include Bureau ID, Sift, Sardine, Feedzai, SEON, and Alloy.

2. How does fraud detection software work in fintech?

Fraud detection software collects signals from users, devices, transactions, accounts, and behavior. It then applies rules, AI models, and risk scores to detect suspicious activity. Fraud teams use alerts, case workflows, and decision records to review, approve, block, or escalate risky activity.

3. What features should fintech fraud detection software include?

Fintech fraud detection software should include real-time monitoring, risk scoring, identity verification, transaction monitoring, device intelligence, behavioral analytics, rule engines, AI models, case management, API integrations, and compliance support. These features help teams detect fraud without adding unnecessary friction.

4. What makes Bureau ID a good choice for fintech fraud detection?

Bureau ID is a good choice for fintech fraud detection when teams need identity, device, behavior, and risk signals to work together across onboarding and transaction journeys. It supports fraud checks for use cases such as account takeover, fake accounts, synthetic identity risk, mule activity, and payment fraud.

5. How can fintech companies detect fraud in real time?

Fintech companies can detect fraud in real time by monitoring transactions, logins, account changes, device signals, and user behavior as they happen. Real-time risk scoring helps teams flag suspicious payments, account takeover attempts, synthetic identities, scams, and money mule activity before losses increase.

6. How does AI improve fintech fraud detection?

AI improves fintech fraud detection by identifying patterns that static rules may miss. It helps detect unusual behavior, payment risk, account takeover attempts, synthetic identities, and scam signals. AI also supports faster investigations by prioritizing high-risk alerts for fraud teams.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.