How to Detect Mule Accounts and Prevent Fraud in Real Time

How to Detect Mule Accounts and Prevent Fraud in Real Time

How to Detect Mule Accounts and Prevent Fraud in Real Time

Learn money mule detection techniques banks use to spot mule accounts, detect networks, reduce false positives, and stop fraud in real time.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

A mule account can pass onboarding, receive small deposits, and behave like a normal account until stolen funds start moving through it. For banks, fintechs, and payment platforms, that makes mule activity hard to catch with basic rules or transaction alerts alone.

Money mule detection helps identify accounts used to receive, transfer, layer, or withdraw illicit funds. Modern detection combines identity checks, device intelligence, behavioral signals, transaction monitoring, graph intelligence, and real-time risk scoring to spot risky accounts before funds move further.

In this guide, we’ll cover the main types of money mules, common red flags, key detection techniques, real-time detection workflows, and explain how Bureau ID helps banks and fintechs detect mule networks earlier.

Types of Money Mules

Money mules are people or accounts used to receive, transfer, layer, or withdraw illicit funds. For banks and fintechs, the tricky part is that mule activity does not always announce itself early. An account may look normal during onboarding, build a short history of routine activity, and only later become part of a pass-through fraud chain.

This matters because mule accounts often sit inside a much larger fraud economy. UNODC’s 2025 report on illicit crimes estimates that hundreds of industrial-scale scam centres generate just under USD 40 billion in annual profits, with criminal groups using cryptocurrency and underground banking to launder proceeds.

That is why money mule detection needs to account for different mule types. Each type creates a slightly different pattern, and each one needs a layered view of identity, device, behavior, transaction, and network signals.

Witting mules: These users knowingly allow their accounts to move illicit funds by renting their accounts, opening a new account for a fraudster, or transferring money for a commission. The problem is that the account can look legitimate until the actual fund movement begins.

Unwitting mules: These users may believe they are helping an employer, romantic partner, friend, or investment contact, not realizing they are moving scam proceeds. In these cases, detection needs to focus less on intent and more on activity patterns, such as sudden inflows, quick transfers, and frequent beneficiary changes.

Synthetic identity mule accounts: These accounts are created using fabricated or manipulated identity details, which may pass weak verification checks and stay quiet until a fraud ring activates them. This is where digital footprint checks, device intelligence, and identity consistency signals become important.

Account takeover-enabled mule accounts: These accounts start as legitimate customer accounts but become mule channels after fraudsters gain access. Since the account already has history and trust, detection needs to spot changes in behavior, device usage, and transaction velocity.

Once you understand the main mule types, the next step is to look at the red flags that reveal mule activity before funds move further.

Common Red Flags and Indicators of Mule Activity

Money mule detection becomes much stronger when fraud teams stop looking at alerts in isolation. One new beneficiary may not mean much on its own, but a new beneficiary combined with a new device, sudden transaction velocity, and a quick cash-out together tells a very different story.

That is usually how mule activity shows up, as a pattern of small changes that start to look suspicious when viewed together.

Indicator | Why It Matters |

Sudden spikes in transaction velocity | Indicates rapid pass-through movement |

Shared devices across multiple accounts | Signals coordinated fraud infrastructure |

Frequent beneficiary changes | Common in layered laundering activity |

Dormant accounts are becoming highly active | Often linked to mule recruitment or takeover |

Rapid withdrawals or cash-outs | Suggests attempts to move funds quickly |

This is where device intelligence and graph intelligence become useful. They help fraud teams connect accounts, devices, beneficiaries, and transaction paths that may look harmless when reviewed separately. Once those patterns are connected, mule activity becomes easier to spot earlier in the journey.

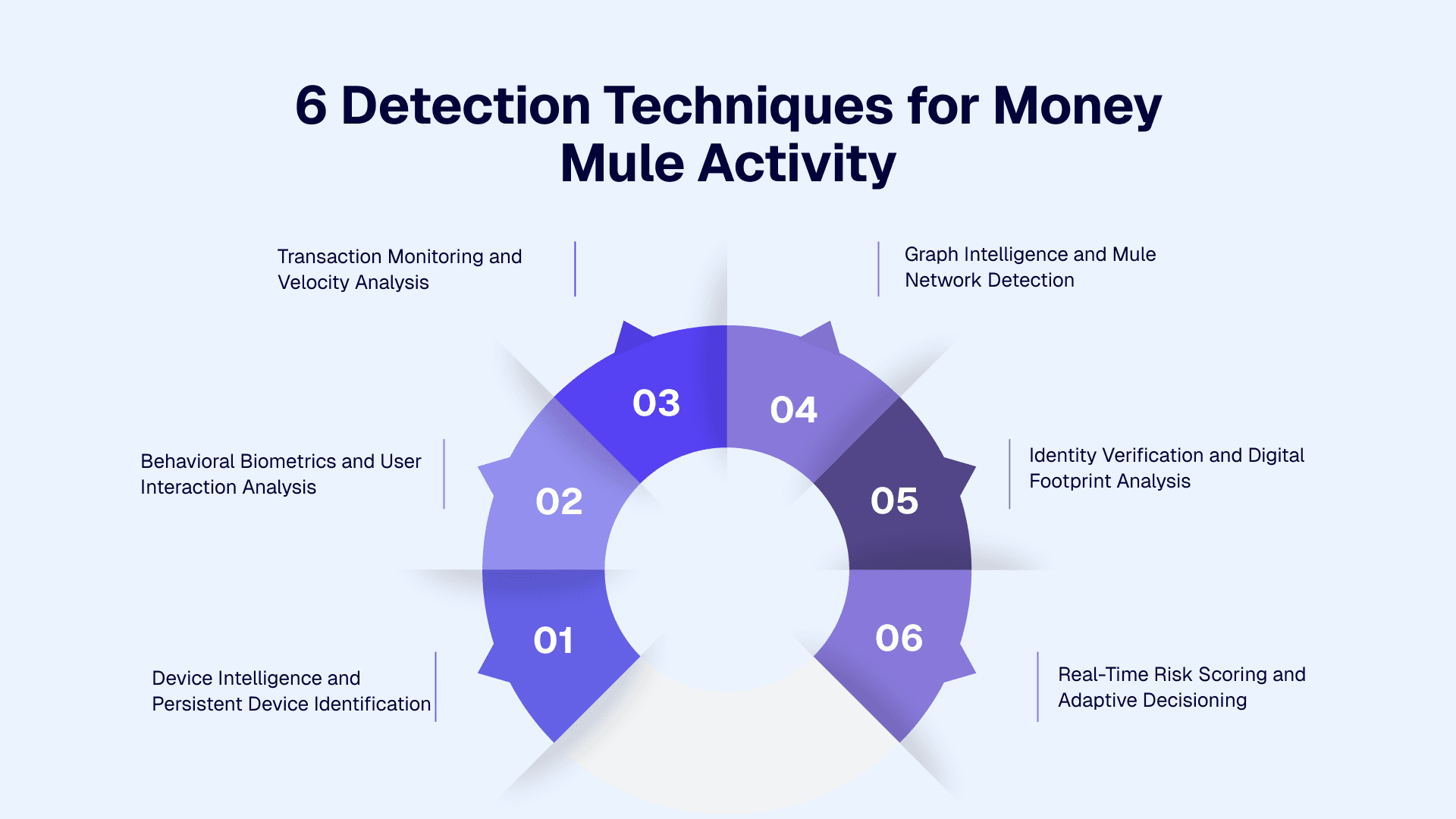

6 Detection Techniques for Money Mule Activity

Money mule detection works best when banks and fintechs connect signals across identity, device, behavior, transactions, and networks in real time. Static AML rules and threshold-based monitoring still have a role, but they often catch risk after suspicious movement has already started.

This is also where fragmented systems become a real detection gap. The Indian Cyber Crime Coordination Centre (I4C) Suspect Registry, built in collaboration with banks and financial institutions, had shared 26.48 lakh Layer 1 mule accounts with participating entities by December 31, 2025, helping decline transactions worth ₹9,055.27 crore.

That scale shows why mule detection cannot depend on isolated transaction alerts alone. A stronger detection model follows the account from onboarding to every transaction, so fraud teams can spot mule activity before funds move further.

1. Device Intelligence and Persistent Device Identification

Device intelligence helps fraud teams identify the infrastructure behind mule activity. A user may create a new account, change an email address, or use different personal details, but the same device can often reveal repeat behavior.

This helps banks and fintechs detect shared devices across multiple accounts, spoofed devices, emulators, VPN usage, and other suspicious device patterns. Bureau ID’s Device ID, for example, analyzes 200+ device attributes and offers 99.97% persistence, helping risk teams recognize risky devices even when fraudsters try to change basic identifiers.

2. Behavioral Biometrics and User Interaction Analysis

Behavioral biometrics look at how a user interacts with an app or platform. This can include typing rhythm, navigation behavior, session patterns, hesitation, and other interaction signals.

This matters because mule activity does not always come from the original account holder. Fraud farms, scripted flows, and hired account operators often behave differently from genuine users. Behavioral analysis helps fraud teams detect these differences even when the login credentials or identity details appear valid.

3. Transaction Monitoring and Velocity Analysis

Transaction monitoring helps identify pass-through account fraud by tracking how money enters, moves through, and leaves an account. Mule accounts often receive funds and move them quickly through transfers, withdrawals, wallets, or other cash-out routes.

Velocity analysis adds the timing layer, as this is also a common concern in AML operations. Practitioners suggest focusing less on the payment label itself and more on what happens after the money enters the account: whether the activity is new, whether the volume is unusual, and whether funds are quickly cashed out.

Fraud teams can see whether the account is moving funds faster than usual, sending money to multiple beneficiaries, or showing activity that does not match the customer’s profile. This becomes more useful when transaction data is connected with device, identity, and network signals.

4. Graph Intelligence and Mule Network Detection

Graph intelligence helps fraud teams move beyond single-account review. Mule accounts often appear harmless when viewed separately, but the connections between them can reveal the real risk.

Fraud rings may reuse devices, phone numbers, addresses, beneficiaries, IP patterns, and transaction routes across several accounts. Graph-based intelligence maps these relationships and helps teams uncover mule networks that individual alerts may miss. This is especially important when funds move through multiple accounts before cash-out.

5. Identity Verification and Digital Footprint Analysis

Identity verification helps reduce mule risk before an account becomes active. Banks and fintechs can check whether a person, phone number, email address, device, and digital footprint point to a real and consistent identity.

This is especially useful for synthetic identity mule accounts and ghost account detection. A document check may confirm that an ID looks valid, but digital footprint analysis can show whether the identity behaves like a real customer. Phone reputation, email history, device history, and identity consistency all support stronger mule account identification.

6. Real-Time Risk Scoring and Adaptive Decisioning

Real-time risk scoring helps institutions act while the transaction is still in progress. A modern system can continuously evaluate risk, trigger alerts, hold suspicious transactions, request step-up verification, or escalate a case for review.

This approach also gives fraud and AML teams more context behind each decision. When a case moves toward suspicious activity reporting or SAR filing, teams need to understand why an account was flagged. Adaptive scoring improves over time by learning from confirmed fraud, false positives, analyst feedback, and changing mule typologies.

When these techniques work together, fraud teams get a clearer view of what each signal can and cannot detect on its own.

Detection technique | Detects | Limitation if used alone |

Device intelligence | Shared fraud infrastructure | Misses transaction context |

Behavioral biometrics | Scripted or coordinated activity | Limited network visibility |

Transaction monitoring | Pass-through movement patterns | Reactive without an identity context |

Graph intelligence | Fraud rings and linked accounts | Requires connected datasets |

Identity verification | Synthetic and risky identities | Limited post-onboarding visibility |

Adaptive risk scoring | Real-time suspicious behavior | Depends on signal quality |

This comparison also shows why single-signal detection often falls short. Mule account detection becomes stronger when fraud teams connect onboarding risk, device behavior, transaction activity, and network relationships in one decision flow.

Related Read: The Growing Threat of Remote Access Trojans and Money Mules to Digital Trust

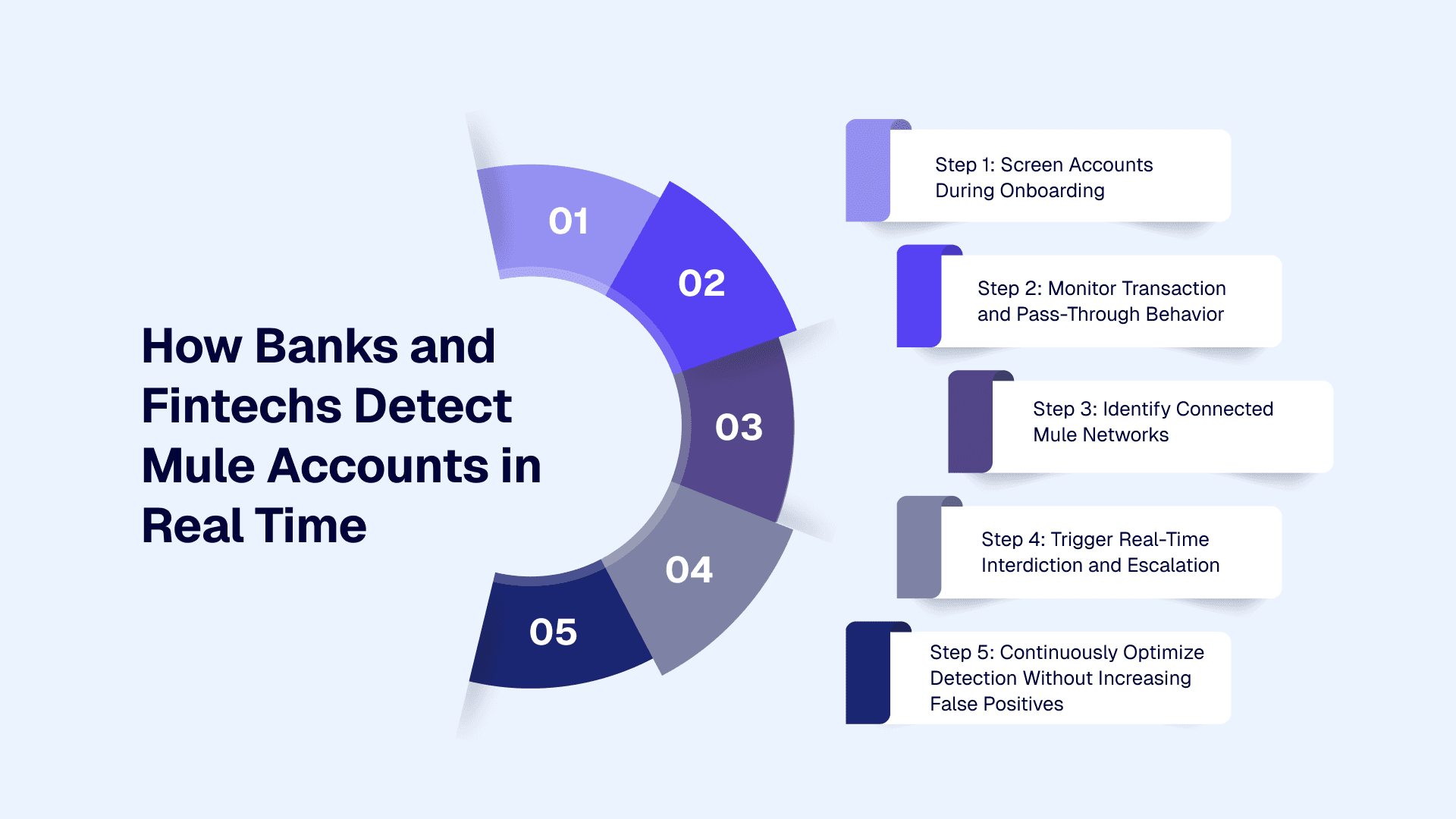

How Banks and Fintechs Detect Mule Accounts in Real Time

Banks and fintechs usually detect mule accounts through a layered workflow that starts at onboarding and continues through every high-risk transaction. The goal is to spot risky accounts early, connect suspicious behavior across accounts, and act before funds move further.

Step 1: Screen Accounts During Onboarding

The first opportunity to detect mule risk appears before the account becomes active. Banks and fintechs can check identity documents, device signals, phone and email reputation, digital footprint, and synthetic identity indicators during onboarding.

This step matters because many mule accounts are prepared before the actual fraud event. A weak onboarding process gives fraudsters room to create or control accounts and activate them later for pass-through movement.

Step 2: Monitor Transaction and Pass-Through Behavior

Once the account is active, transaction behavior becomes a critical signal. Fraud teams need to watch for rapid inflows, fast fund movement, high-velocity transfers, repeated beneficiary changes, and quick cash-outs.

This is especially important in APP fraud and digital payment fraud, where funds can move quickly from the victim to a receiving account and then to another destination. Receiving-side monitoring helps banks and fintechs identify suspicious movement before the mule account becomes only one more step in a longer laundering chain.

Step 3: Identify Connected Mule Networks

Mule activity often becomes clearer when teams look beyond a single account. Shared devices, linked beneficiaries, reused phone numbers, similar onboarding patterns, and repeated transaction paths can expose accounts that belong to the same fraud ring.

This is where mule network detection becomes more useful than isolated account review. A new account may not look risky on its own, but its connection to several suspicious accounts can change how the risk team treats it.

Step 4: Trigger Real-Time Interdiction and Escalation

Detection only helps when the institution can act quickly, because speed can change the outcome. According to the FBI’s 2024 Internet Crime Report, the Financial Fraud Kill Chain handled 3,020 complaints involving USD 848.4 million in attempted theft and achieved a 66% success rate in freezing funds.

Real-time interdiction may include transaction holds, step-up verification, account restrictions, AML escalation, or fraud investigation.

At the same time, the process needs to protect legitimate customers. Risk teams need enough context to understand why an account was flagged, so they can decide whether to approve, hold, escalate, or prepare suspicious activity reporting.

Step 5: Continuously Optimize Detection Without Increasing False Positives

False positives create extra work for analysts and unnecessary friction for customers. A strong framework uses feedback loops to improve risk scoring, reduce low-quality alerts, and focus attention on high-risk mule activity.

Financial institutions should track confirmed mule accounts, blocked losses, alert quality, case resolution time, and customer impact. These metrics help teams improve detection without slowing down genuine users.

A strong real-time workflow connects onboarding risk, transaction behavior, and mule network signals into decisions that fraud teams can act on before suspicious funds move out of reach.

How Bureau ID Helps Detect and Prevent Money Mule Activity

Bureau ID helps banks and fintechs detect mule activity through unified risk decisioning across identity, device, behavior, network, and transaction signals. Its money mule detection solution uses a dynamic Mule Score to flag mule risk across onboarding, account monitoring, and transaction activity.

Instead of treating mule detection as a single alerting problem, Bureau ID connects multiple signals that often reveal risk only when viewed together. This helps fraud and AML teams identify suspicious accounts, uncover linked mule networks, and act before pass-through movement becomes harder to stop.

The platform supports money mule detection through capabilities such as:

Mule Score for onboarding, monitoring, and interdiction: Risk teams can assess mule risk before an account becomes active and continue monitoring suspicious behavior after onboarding.

Graph Identity Network for mule network detection: Instead of reviewing accounts one by one, teams can uncover connected accounts, shared patterns, and fraud-ring behavior across Bureau ID’s network of 500M+ identities.

Device intelligence for repeat fraud actors: Fraudsters may change account details, but reused devices, suspicious device behavior, and coordinated mule infrastructure can still reveal repeat risk.

Behavioral biometrics for coordinated activity: User interaction signals can surface scripted behavior, unusual session patterns, and fraud-farm activity that basic credential checks may miss.

Real-time transaction monitoring and adaptive scoring: Bureau ID evaluates 200+ risk signals across device, identity, behavior, email, phone, and network data, giving teams faster context before risky activity moves further.

Explainable risk decisions: Fraud and compliance teams can see why an account or transaction was flagged, which makes reviews, escalations, and investigations easier to manage.

No-code workflow orchestration: Risk teams can adjust decision flows, rules, and thresholds more quickly without depending on engineering teams for every workflow change.

Together, these capabilities help Bureau ID support mule account detection at the points where risk usually appears: during onboarding, when accounts start behaving differently, and when connected accounts begin moving funds in coordinated patterns.

A relevant example is Bureau ID’s Mule Score work with a leading Indian bank, where early-stage detection helped the bank stop high-risk mule accounts before they became active channels.

Case Study: How a leading Indian bank increased high-risk mule detection by 60%

A leading Indian bank needed to identify mule accounts earlier during onboarding. Besides detecting suspicious transactions after they occurred, the bank needed to spot high-risk accounts before they could be used for pass-through fund movement, account layering, or downstream fraud.

What Bureau ID implemented:

Bureau ID deployed its Mule Score to evaluate mule risk during onboarding.

The solution used identity, device, behavioral, and network signals to identify high-risk accounts earlier.

Bureau ID’s risk intelligence helped surface accounts that may not have appeared suspicious through basic onboarding checks alone.

The bank used Bureau ID’s scoring to improve early interdiction and reduce the chance of mule accounts entering the active customer base.

Results achieved:

60% increase in high-risk account identification during onboarding.

300,000 potential mule accounts stopped.

$40M in potential losses prevented.

The key takeaway is simple: mule detection works better when risk teams identify mule accounts before funds start moving. Bureau ID’s approach gives banks and fintechs a way to connect early identity risk, device intelligence, network relationships, and transaction behavior into decisions that can be acted on in real time.

If you're curious about how this would work across your onboarding, transaction monitoring, and fraud investigation workflows, a quick 30-minute demo with Bureau ID can help you map the right mule detection approach for your risk environment.

Build a Real-Time Mule Detection Framework

By the time a mule account looks obvious, the money may already be gone.

That is why the next step is to move from isolated alert review to a real-time mule detection framework. That means connecting onboarding checks, device intelligence, behavioral signals, transaction monitoring, graph intelligence, and risk scoring into one decision flow. Fraud teams need to see not just whether one account looks risky, but whether that account is connected to a larger mule network.

Bureau ID helps banks and fintechs bring these signals together through Mule Score, Graph Identity Network, device intelligence, behavioral biometrics, and real-time risk decisioning. This gives risk teams a clearer way to identify mule accounts earlier, uncover connected fraud patterns, and act before suspicious funds move further.

If mule account detection is becoming harder to manage with rules, manual reviews, or disconnected systems, schedule a demo with Bureau ID and see how real-time mule detection could work for your team.

FAQs

1. What is money mule detection?

Money mule detection is the process of identifying accounts, transactions, and networks used to move illegally obtained funds. Banks and fintechs use transaction monitoring, identity checks, device intelligence, behavioral signals, and risk scoring to flag mule activity before stolen money moves further.

2. How does money mule detection work in banking?

Money mule detection in banking works by monitoring account behavior, transaction speed, fund movement, device usage, and customer identity signals. Banks look for unusual inflows, fast withdrawals, shared devices, weak KYC details, and links between suspicious accounts.

3. What are the common red flags of money mule activity?

Common money mule red flags include sudden account activity, rapid fund transfers, multiple unrelated beneficiaries, high transaction velocity, new accounts receiving large inflows, dormant accounts becoming active, and quick withdrawals after money enters the account.

4. How does Bureau ID help with money mule detection?

Bureau ID helps banks and fintechs detect money mule activity by combining device intelligence, behavioral signals, identity checks, graph intelligence, and real-time risk scoring. This helps risk teams identify suspicious accounts, connected mule networks, and high-risk transactions before funds move further.

5. What role does graph analytics play in detecting money mules?

Graph analytics helps detect money mules by mapping relationships between accounts, devices, phone numbers, IP addresses, beneficiaries, and transaction paths. This helps fraud teams identify connected mule networks instead of reviewing suspicious accounts in isolation.

6. How can banks reduce false positives in mule detection?

Banks can reduce false positives by combining multiple signals instead of relying on single transaction rules. Strong detection uses identity data, transaction history, device signals, behavioral patterns, network links, and real-time risk scoring to separate risky activity from legitimate customer behavior.

A mule account can pass onboarding, receive small deposits, and behave like a normal account until stolen funds start moving through it. For banks, fintechs, and payment platforms, that makes mule activity hard to catch with basic rules or transaction alerts alone.

Money mule detection helps identify accounts used to receive, transfer, layer, or withdraw illicit funds. Modern detection combines identity checks, device intelligence, behavioral signals, transaction monitoring, graph intelligence, and real-time risk scoring to spot risky accounts before funds move further.

In this guide, we’ll cover the main types of money mules, common red flags, key detection techniques, real-time detection workflows, and explain how Bureau ID helps banks and fintechs detect mule networks earlier.

Types of Money Mules

Money mules are people or accounts used to receive, transfer, layer, or withdraw illicit funds. For banks and fintechs, the tricky part is that mule activity does not always announce itself early. An account may look normal during onboarding, build a short history of routine activity, and only later become part of a pass-through fraud chain.

This matters because mule accounts often sit inside a much larger fraud economy. UNODC’s 2025 report on illicit crimes estimates that hundreds of industrial-scale scam centres generate just under USD 40 billion in annual profits, with criminal groups using cryptocurrency and underground banking to launder proceeds.

That is why money mule detection needs to account for different mule types. Each type creates a slightly different pattern, and each one needs a layered view of identity, device, behavior, transaction, and network signals.

Witting mules: These users knowingly allow their accounts to move illicit funds by renting their accounts, opening a new account for a fraudster, or transferring money for a commission. The problem is that the account can look legitimate until the actual fund movement begins.

Unwitting mules: These users may believe they are helping an employer, romantic partner, friend, or investment contact, not realizing they are moving scam proceeds. In these cases, detection needs to focus less on intent and more on activity patterns, such as sudden inflows, quick transfers, and frequent beneficiary changes.

Synthetic identity mule accounts: These accounts are created using fabricated or manipulated identity details, which may pass weak verification checks and stay quiet until a fraud ring activates them. This is where digital footprint checks, device intelligence, and identity consistency signals become important.

Account takeover-enabled mule accounts: These accounts start as legitimate customer accounts but become mule channels after fraudsters gain access. Since the account already has history and trust, detection needs to spot changes in behavior, device usage, and transaction velocity.

Once you understand the main mule types, the next step is to look at the red flags that reveal mule activity before funds move further.

Common Red Flags and Indicators of Mule Activity

Money mule detection becomes much stronger when fraud teams stop looking at alerts in isolation. One new beneficiary may not mean much on its own, but a new beneficiary combined with a new device, sudden transaction velocity, and a quick cash-out together tells a very different story.

That is usually how mule activity shows up, as a pattern of small changes that start to look suspicious when viewed together.

Indicator | Why It Matters |

Sudden spikes in transaction velocity | Indicates rapid pass-through movement |

Shared devices across multiple accounts | Signals coordinated fraud infrastructure |

Frequent beneficiary changes | Common in layered laundering activity |

Dormant accounts are becoming highly active | Often linked to mule recruitment or takeover |

Rapid withdrawals or cash-outs | Suggests attempts to move funds quickly |

This is where device intelligence and graph intelligence become useful. They help fraud teams connect accounts, devices, beneficiaries, and transaction paths that may look harmless when reviewed separately. Once those patterns are connected, mule activity becomes easier to spot earlier in the journey.

6 Detection Techniques for Money Mule Activity

Money mule detection works best when banks and fintechs connect signals across identity, device, behavior, transactions, and networks in real time. Static AML rules and threshold-based monitoring still have a role, but they often catch risk after suspicious movement has already started.

This is also where fragmented systems become a real detection gap. The Indian Cyber Crime Coordination Centre (I4C) Suspect Registry, built in collaboration with banks and financial institutions, had shared 26.48 lakh Layer 1 mule accounts with participating entities by December 31, 2025, helping decline transactions worth ₹9,055.27 crore.

That scale shows why mule detection cannot depend on isolated transaction alerts alone. A stronger detection model follows the account from onboarding to every transaction, so fraud teams can spot mule activity before funds move further.

1. Device Intelligence and Persistent Device Identification

Device intelligence helps fraud teams identify the infrastructure behind mule activity. A user may create a new account, change an email address, or use different personal details, but the same device can often reveal repeat behavior.

This helps banks and fintechs detect shared devices across multiple accounts, spoofed devices, emulators, VPN usage, and other suspicious device patterns. Bureau ID’s Device ID, for example, analyzes 200+ device attributes and offers 99.97% persistence, helping risk teams recognize risky devices even when fraudsters try to change basic identifiers.

2. Behavioral Biometrics and User Interaction Analysis

Behavioral biometrics look at how a user interacts with an app or platform. This can include typing rhythm, navigation behavior, session patterns, hesitation, and other interaction signals.

This matters because mule activity does not always come from the original account holder. Fraud farms, scripted flows, and hired account operators often behave differently from genuine users. Behavioral analysis helps fraud teams detect these differences even when the login credentials or identity details appear valid.

3. Transaction Monitoring and Velocity Analysis

Transaction monitoring helps identify pass-through account fraud by tracking how money enters, moves through, and leaves an account. Mule accounts often receive funds and move them quickly through transfers, withdrawals, wallets, or other cash-out routes.

Velocity analysis adds the timing layer, as this is also a common concern in AML operations. Practitioners suggest focusing less on the payment label itself and more on what happens after the money enters the account: whether the activity is new, whether the volume is unusual, and whether funds are quickly cashed out.

Fraud teams can see whether the account is moving funds faster than usual, sending money to multiple beneficiaries, or showing activity that does not match the customer’s profile. This becomes more useful when transaction data is connected with device, identity, and network signals.

4. Graph Intelligence and Mule Network Detection

Graph intelligence helps fraud teams move beyond single-account review. Mule accounts often appear harmless when viewed separately, but the connections between them can reveal the real risk.

Fraud rings may reuse devices, phone numbers, addresses, beneficiaries, IP patterns, and transaction routes across several accounts. Graph-based intelligence maps these relationships and helps teams uncover mule networks that individual alerts may miss. This is especially important when funds move through multiple accounts before cash-out.

5. Identity Verification and Digital Footprint Analysis

Identity verification helps reduce mule risk before an account becomes active. Banks and fintechs can check whether a person, phone number, email address, device, and digital footprint point to a real and consistent identity.

This is especially useful for synthetic identity mule accounts and ghost account detection. A document check may confirm that an ID looks valid, but digital footprint analysis can show whether the identity behaves like a real customer. Phone reputation, email history, device history, and identity consistency all support stronger mule account identification.

6. Real-Time Risk Scoring and Adaptive Decisioning

Real-time risk scoring helps institutions act while the transaction is still in progress. A modern system can continuously evaluate risk, trigger alerts, hold suspicious transactions, request step-up verification, or escalate a case for review.

This approach also gives fraud and AML teams more context behind each decision. When a case moves toward suspicious activity reporting or SAR filing, teams need to understand why an account was flagged. Adaptive scoring improves over time by learning from confirmed fraud, false positives, analyst feedback, and changing mule typologies.

When these techniques work together, fraud teams get a clearer view of what each signal can and cannot detect on its own.

Detection technique | Detects | Limitation if used alone |

Device intelligence | Shared fraud infrastructure | Misses transaction context |

Behavioral biometrics | Scripted or coordinated activity | Limited network visibility |

Transaction monitoring | Pass-through movement patterns | Reactive without an identity context |

Graph intelligence | Fraud rings and linked accounts | Requires connected datasets |

Identity verification | Synthetic and risky identities | Limited post-onboarding visibility |

Adaptive risk scoring | Real-time suspicious behavior | Depends on signal quality |

This comparison also shows why single-signal detection often falls short. Mule account detection becomes stronger when fraud teams connect onboarding risk, device behavior, transaction activity, and network relationships in one decision flow.

Related Read: The Growing Threat of Remote Access Trojans and Money Mules to Digital Trust

How Banks and Fintechs Detect Mule Accounts in Real Time

Banks and fintechs usually detect mule accounts through a layered workflow that starts at onboarding and continues through every high-risk transaction. The goal is to spot risky accounts early, connect suspicious behavior across accounts, and act before funds move further.

Step 1: Screen Accounts During Onboarding

The first opportunity to detect mule risk appears before the account becomes active. Banks and fintechs can check identity documents, device signals, phone and email reputation, digital footprint, and synthetic identity indicators during onboarding.

This step matters because many mule accounts are prepared before the actual fraud event. A weak onboarding process gives fraudsters room to create or control accounts and activate them later for pass-through movement.

Step 2: Monitor Transaction and Pass-Through Behavior

Once the account is active, transaction behavior becomes a critical signal. Fraud teams need to watch for rapid inflows, fast fund movement, high-velocity transfers, repeated beneficiary changes, and quick cash-outs.

This is especially important in APP fraud and digital payment fraud, where funds can move quickly from the victim to a receiving account and then to another destination. Receiving-side monitoring helps banks and fintechs identify suspicious movement before the mule account becomes only one more step in a longer laundering chain.

Step 3: Identify Connected Mule Networks

Mule activity often becomes clearer when teams look beyond a single account. Shared devices, linked beneficiaries, reused phone numbers, similar onboarding patterns, and repeated transaction paths can expose accounts that belong to the same fraud ring.

This is where mule network detection becomes more useful than isolated account review. A new account may not look risky on its own, but its connection to several suspicious accounts can change how the risk team treats it.

Step 4: Trigger Real-Time Interdiction and Escalation

Detection only helps when the institution can act quickly, because speed can change the outcome. According to the FBI’s 2024 Internet Crime Report, the Financial Fraud Kill Chain handled 3,020 complaints involving USD 848.4 million in attempted theft and achieved a 66% success rate in freezing funds.

Real-time interdiction may include transaction holds, step-up verification, account restrictions, AML escalation, or fraud investigation.

At the same time, the process needs to protect legitimate customers. Risk teams need enough context to understand why an account was flagged, so they can decide whether to approve, hold, escalate, or prepare suspicious activity reporting.

Step 5: Continuously Optimize Detection Without Increasing False Positives

False positives create extra work for analysts and unnecessary friction for customers. A strong framework uses feedback loops to improve risk scoring, reduce low-quality alerts, and focus attention on high-risk mule activity.

Financial institutions should track confirmed mule accounts, blocked losses, alert quality, case resolution time, and customer impact. These metrics help teams improve detection without slowing down genuine users.

A strong real-time workflow connects onboarding risk, transaction behavior, and mule network signals into decisions that fraud teams can act on before suspicious funds move out of reach.

How Bureau ID Helps Detect and Prevent Money Mule Activity

Bureau ID helps banks and fintechs detect mule activity through unified risk decisioning across identity, device, behavior, network, and transaction signals. Its money mule detection solution uses a dynamic Mule Score to flag mule risk across onboarding, account monitoring, and transaction activity.

Instead of treating mule detection as a single alerting problem, Bureau ID connects multiple signals that often reveal risk only when viewed together. This helps fraud and AML teams identify suspicious accounts, uncover linked mule networks, and act before pass-through movement becomes harder to stop.

The platform supports money mule detection through capabilities such as:

Mule Score for onboarding, monitoring, and interdiction: Risk teams can assess mule risk before an account becomes active and continue monitoring suspicious behavior after onboarding.

Graph Identity Network for mule network detection: Instead of reviewing accounts one by one, teams can uncover connected accounts, shared patterns, and fraud-ring behavior across Bureau ID’s network of 500M+ identities.

Device intelligence for repeat fraud actors: Fraudsters may change account details, but reused devices, suspicious device behavior, and coordinated mule infrastructure can still reveal repeat risk.

Behavioral biometrics for coordinated activity: User interaction signals can surface scripted behavior, unusual session patterns, and fraud-farm activity that basic credential checks may miss.

Real-time transaction monitoring and adaptive scoring: Bureau ID evaluates 200+ risk signals across device, identity, behavior, email, phone, and network data, giving teams faster context before risky activity moves further.

Explainable risk decisions: Fraud and compliance teams can see why an account or transaction was flagged, which makes reviews, escalations, and investigations easier to manage.

No-code workflow orchestration: Risk teams can adjust decision flows, rules, and thresholds more quickly without depending on engineering teams for every workflow change.

Together, these capabilities help Bureau ID support mule account detection at the points where risk usually appears: during onboarding, when accounts start behaving differently, and when connected accounts begin moving funds in coordinated patterns.

A relevant example is Bureau ID’s Mule Score work with a leading Indian bank, where early-stage detection helped the bank stop high-risk mule accounts before they became active channels.

Case Study: How a leading Indian bank increased high-risk mule detection by 60%

A leading Indian bank needed to identify mule accounts earlier during onboarding. Besides detecting suspicious transactions after they occurred, the bank needed to spot high-risk accounts before they could be used for pass-through fund movement, account layering, or downstream fraud.

What Bureau ID implemented:

Bureau ID deployed its Mule Score to evaluate mule risk during onboarding.

The solution used identity, device, behavioral, and network signals to identify high-risk accounts earlier.

Bureau ID’s risk intelligence helped surface accounts that may not have appeared suspicious through basic onboarding checks alone.

The bank used Bureau ID’s scoring to improve early interdiction and reduce the chance of mule accounts entering the active customer base.

Results achieved:

60% increase in high-risk account identification during onboarding.

300,000 potential mule accounts stopped.

$40M in potential losses prevented.

The key takeaway is simple: mule detection works better when risk teams identify mule accounts before funds start moving. Bureau ID’s approach gives banks and fintechs a way to connect early identity risk, device intelligence, network relationships, and transaction behavior into decisions that can be acted on in real time.

If you're curious about how this would work across your onboarding, transaction monitoring, and fraud investigation workflows, a quick 30-minute demo with Bureau ID can help you map the right mule detection approach for your risk environment.

Build a Real-Time Mule Detection Framework

By the time a mule account looks obvious, the money may already be gone.

That is why the next step is to move from isolated alert review to a real-time mule detection framework. That means connecting onboarding checks, device intelligence, behavioral signals, transaction monitoring, graph intelligence, and risk scoring into one decision flow. Fraud teams need to see not just whether one account looks risky, but whether that account is connected to a larger mule network.

Bureau ID helps banks and fintechs bring these signals together through Mule Score, Graph Identity Network, device intelligence, behavioral biometrics, and real-time risk decisioning. This gives risk teams a clearer way to identify mule accounts earlier, uncover connected fraud patterns, and act before suspicious funds move further.

If mule account detection is becoming harder to manage with rules, manual reviews, or disconnected systems, schedule a demo with Bureau ID and see how real-time mule detection could work for your team.

FAQs

1. What is money mule detection?

Money mule detection is the process of identifying accounts, transactions, and networks used to move illegally obtained funds. Banks and fintechs use transaction monitoring, identity checks, device intelligence, behavioral signals, and risk scoring to flag mule activity before stolen money moves further.

2. How does money mule detection work in banking?

Money mule detection in banking works by monitoring account behavior, transaction speed, fund movement, device usage, and customer identity signals. Banks look for unusual inflows, fast withdrawals, shared devices, weak KYC details, and links between suspicious accounts.

3. What are the common red flags of money mule activity?

Common money mule red flags include sudden account activity, rapid fund transfers, multiple unrelated beneficiaries, high transaction velocity, new accounts receiving large inflows, dormant accounts becoming active, and quick withdrawals after money enters the account.

4. How does Bureau ID help with money mule detection?

Bureau ID helps banks and fintechs detect money mule activity by combining device intelligence, behavioral signals, identity checks, graph intelligence, and real-time risk scoring. This helps risk teams identify suspicious accounts, connected mule networks, and high-risk transactions before funds move further.

5. What role does graph analytics play in detecting money mules?

Graph analytics helps detect money mules by mapping relationships between accounts, devices, phone numbers, IP addresses, beneficiaries, and transaction paths. This helps fraud teams identify connected mule networks instead of reviewing suspicious accounts in isolation.

6. How can banks reduce false positives in mule detection?

Banks can reduce false positives by combining multiple signals instead of relying on single transaction rules. Strong detection uses identity data, transaction history, device signals, behavioral patterns, network links, and real-time risk scoring to separate risky activity from legitimate customer behavior.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.