How Businesses Can Stop AI Identity Fraud With Connected Risk Intelligence

How Businesses Can Stop AI Identity Fraud With Connected Risk Intelligence

How Businesses Can Stop AI Identity Fraud With Connected Risk Intelligence

Explore AI identity fraud types, risk signals, prevention technologies, and a step-by-step framework for high-risk digital businesses.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

AI can now generate convincing fake identities, deepfake selfies, cloned voices, and synthetic account activity in minutes. As these tools become more accessible, businesses face a growing challenge: fraudsters can appear legitimate long enough to bypass traditional verification checks.

This is what makes AI identity fraud so dangerous. It extends beyond fake documents or stolen credentials and can surface across onboarding, login, account recovery, transactions, promo abuse, and coordinated fraud rings.

In this guide, we will explain what AI identity fraud is, the most common fraud types businesses need to stop, how these attacks bypass traditional identity verification, and what an effective AI identity fraud prevention framework should include.

What Is AI Identity Fraud?

AI identity fraud is the use of artificial intelligence to fake, steal, or misuse a person’s identity. Fraudsters use deepfakes, voice clones, synthetic identities, fake documents, and automated scripts to bypass identity verification, open fake accounts, take over real accounts, or commit financial crime.

Businesses detect and prevent AI identity fraud by connecting identity checks, device signals, behavioral patterns, liveness detection, risk scoring, and continuous monitoring across the customer journey.

Different AI-driven fraud methods tend to appear at different stages of the customer journey. For instance, during onboarding, fraudsters may use synthetic identities, fake documents, or deepfakes to get through verification. Later, they may rely on phishing, stolen credentials, or social engineering to take over legitimate accounts.

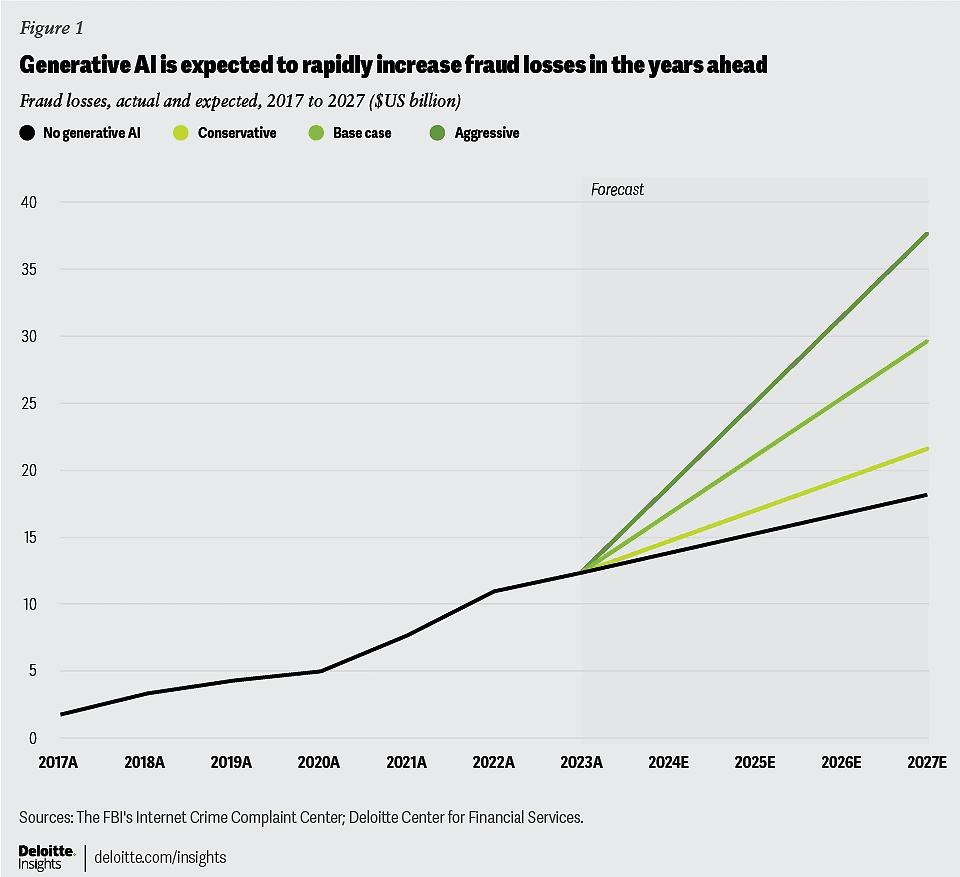

Deloitte Center for Financial Services estimates that GenAI-enabled fraud losses in the U.S. could rise to $40 billion by 2027, showing why AI identity fraud prevention now needs to be treated as a board-level risk.

Image Source: Deloitte Center for Financial Services

The effects go beyond direct fraud losses:

Higher onboarding fraud from convincing fake identities.

More account takeovers through AI-assisted attacks.

Increased manual reviews due to harder-to-spot fraud.

More false positives from broad fraud rules.

Greater exposure to mule accounts and fraud rings.

Higher compliance, financial, and reputational risk.

To prevent AI identity fraud effectively, businesses first need to understand the specific fraud patterns they are dealing with.

Related Read: A Buyer’s Guide To Fraud Detection Software For Fintech Teams

Common Types of AI Identity Fraud Businesses Need to Stop

AI identity fraud evolves quickly because fraudsters can adapt their tactics to different stages of the customer journey. Some attacks are designed to bypass onboarding checks, while others target existing accounts through login abuse, account recovery, transaction fraud, or promotional exploitation.

Understanding where and how these attacks occur helps businesses identify the trust signals being manipulated and build stronger defenses against them.

AI identity fraud type | What fraudsters do | Business risk |

Deepfake fraud | Use AI-generated or manipulated face, video, or voice media to impersonate a real person. | Bypass selfie checks, video KYC, human review, or support verification. |

AI-generated fake IDs | Create or alter identity documents using AI tools. | Pass weak document checks and open fraudulent accounts. |

Synthetic identity fraud | Combine real and fake identity details to create a new persona. | Access credit, wallets, accounts, or services with no intent to repay or comply. |

Biometric spoofing | Attack face, voice, or liveness systems using replays, masks, injections, or generated media. | Defeat biometric verification and impersonate legitimate users. |

Account takeover fraud | Use stolen credentials, AI phishing, or social engineering to access genuine accounts. | Move funds, change account details, steal data, or enable mule activity. |

Mule accounts and fraud rings | Use networks of linked accounts to move money, exploit offers, or hide coordinated abuse. | Individual users may appear legitimate while the network creates large-scale losses. |

Bot-driven fake account creation | Automate signups using synthetic data, proxies, emulators, or scripted behavior. | Increase promo abuse, spam, fake listings, scraping, and platform manipulation. |

These types often overlap in practice. A fraudster may use a synthetic identity during onboarding, a spoofed device to avoid detection, behavioral automation to scale signups, and linked accounts to exploit promotions or move money.

This is why identity checks cannot work in isolation anymore. Gartner predicted that by 2026, 30% of enterprises will no longer consider identity verification and authentication solutions reliable on their own because AI-generated deepfakes can undermine face biometrics.

For businesses, this reinforces the need to pair identity checks with device, behavior, network, and risk signals.

How AI Identity Fraud Bypasses Traditional Identity Verification

Traditional identity verification is still important, but it was not designed to catch every AI-driven fraud pattern on its own. A document check, selfie match, OTP, or password may confirm one part of the user journey, but AI identity fraud often works by exploiting the gaps between those checks.

Some of the most common weaknesses include:

Static document checks can be manipulated: AI-generated or altered documents can look realistic enough to pass basic review, especially when document checks are not connected to device, behavioral, and network signals.

Selfie and face-match checks can be attacked: Deepfake videos, face swaps, replay attacks, and injection attacks can target biometric flows, particularly when liveness detection is weak or isolated.

OTPs and passwords do not prove user trust: A fraudster with stolen credentials, SIM access, or social-engineered recovery access can still appear legitimate at login.

Rules alone miss adaptive fraud: Static rules may catch known patterns, but AI-enabled fraudsters can change devices, IPs, emails, phone numbers, and behavior to avoid simple thresholds.

Siloed tools create blind spots: A KYC tool may approve the identity, a device tool may detect risk, and a transaction tool may flag unusual activity later. If these signals are not connected, the business may miss the broader fraud pattern.

Individual reviews miss fraud rings: Many mule accounts, promo abuse rings, and synthetic identity clusters look harmless when reviewed one by one. The risk becomes visible only when businesses connect shared devices, phone numbers, emails, IPs, and behavioral patterns.

Bureau ID’s UK & EU Fraud Report found that 67% of organizations said siloed systems prevent early signal correlation. It also reported that 83% had observed AI or automation in attacks, which makes fragmented fraud controls even harder to rely on.

This is why identity verification needs to evolve from a one-time checkpoint into a continuous risk layer. Businesses need controls that evaluate whether the device, behavior, account history, and connected network support who the user claims to be.

AI Identity Fraud Prevention Technologies and Approaches

AI identity fraud is difficult to stop with isolated controls alone. Fraudsters attack from different angles, so businesses need a combination of connected capabilities that work together to build a complete picture of risk:

Identity Verification: Validates documents, selfies, biometrics, and other user-submitted information to confirm that a person is who they claim to be.

Document Forensics: Identifies signs of tampering, fake IDs, manipulated fields, and template-level inconsistencies that may indicate fraud.

Liveness and Face Intelligence: Detects spoofing attempts, deepfakes, replay attacks, and other forms of biometric manipulation.

Device Intelligence: Reveals spoofed devices, emulators, VPNs, proxies, repeat devices, and suspicious device-account relationships.

Behavioral Biometrics: Analyzes how users interact with their devices to detect bots, scripted behavior, fraud farms, and unusual session patterns.

Graph Intelligence: Uncovers hidden links between accounts, devices, emails, phone numbers, transactions, and known risk indicators that may not be visible through isolated checks.

Real-Time Risk Decisioning: Allows businesses to approve, reject, review, or step up users while they are still moving through the customer journey.

Adaptive Authentication: Introduces additional verification only when risk increases, helping balance security with user experience.

Most fraud signals become far more meaningful when they are viewed together rather than in isolation. For instance, a device anomaly on its own may not seem serious, but pair it with suspicious behavior, linked accounts, and unusual transaction activity, and a much clearer risk picture starts to emerge.

This is also where unified risk decisioning becomes especially valuable. Instead of forcing teams to piece together signals from multiple tools, Bureau ID brings device, behavior, identity, network, and transaction intelligence into a single real-time decisioning layer.

The result is a more complete view of risk and fewer blind spots that can allow AI-driven fraud to slip through unnoticed.

Related Read: A Modern Framework for Fraud Prevention in Middle East Banking

AI Identity Fraud Prevention Framework for High-Risk Digital Businesses

AI identity fraud prevention works best when businesses treat identity risk as a lifecycle problem. Effective prevention focuses on identifying risk as early as possible, connecting the right signals across the user journey, and making informed decisions at the moments where fraud can have the greatest impact.

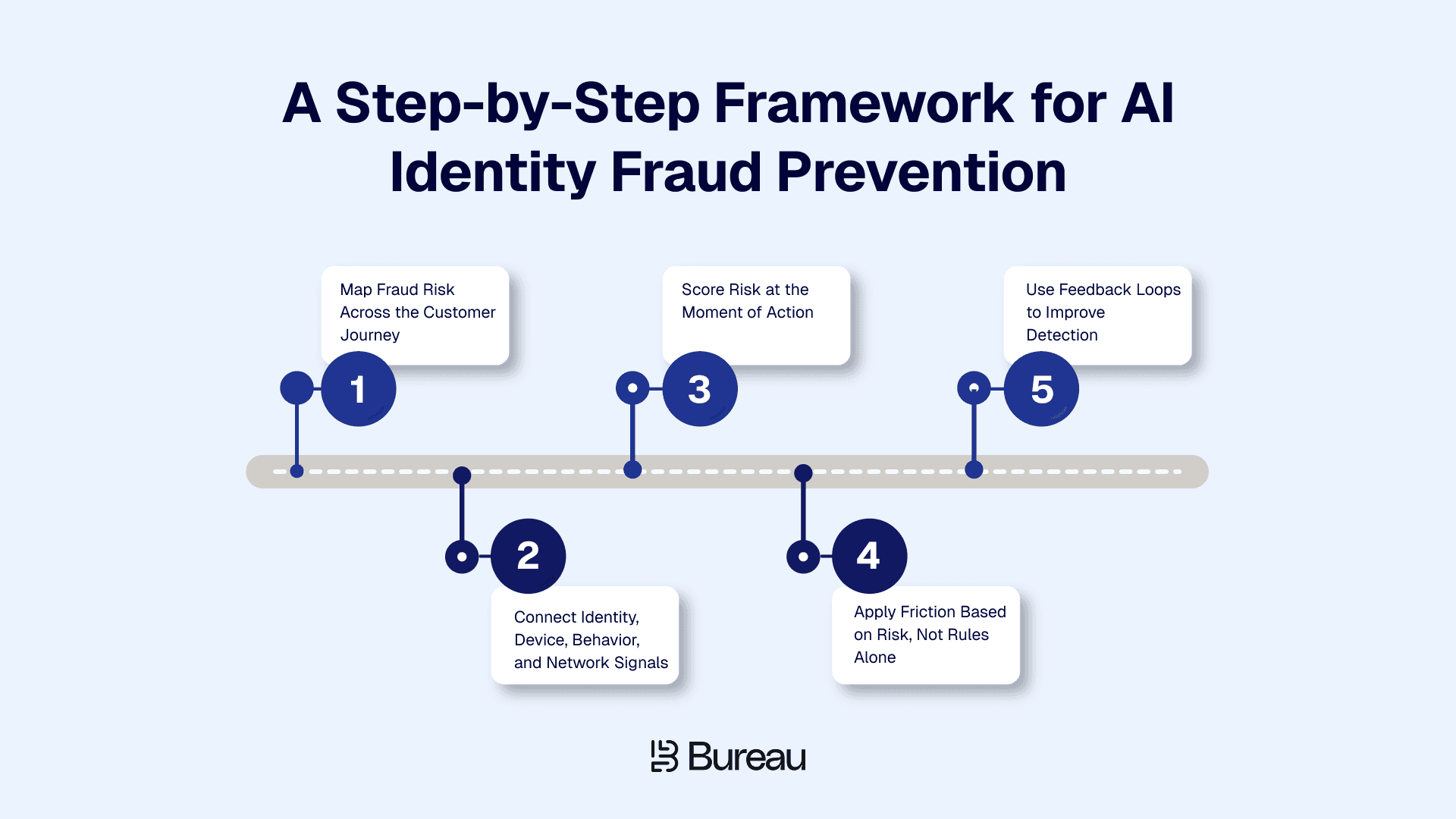

Step 1: Map Fraud Risk Across the Customer Journey

Risk teams should first map where AI identity fraud can appear across the full user journey. This includes account signup, identity verification, login, password reset, account recovery, profile changes, payment method changes, promo redemption, transactions, withdrawals, payouts, and repeat account creation.

A simple mapping exercise can reveal where controls are too narrow.

Journey point | Possible AI identity fraud risk | Current control | Missing signal |

Signup | Synthetic identity or AI-generated ID | Document verification | Device and network intelligence |

KYC | Deepfake selfie or biometric spoof | Face match | Liveness and injection attack detection |

Login | Account takeover | Password and OTP | Device and behavioral risk |

Promo redemption | Multi-accounting | Basic eligibility rules | Device-account linking |

Transaction | Mule activity | Transaction rules | Graph and identity network signals |

This mapping gives risk teams actionable insights, and helps product teams understand where friction should stay low and where step-up checks make sense.

Step 2: Connect Identity, Device, Behavior, and Network Signals

Each signal becomes more useful when viewed in context.

A new account may look normal, but a new account from a device linked to 50 other accounts needs closer review.

Similarly, a clean selfie match may look valid, but a clean selfie match from a spoofed device with bot-like behavior should not receive the same decision as a trusted user on a known device.

Connected risk intelligence helps teams spot these patterns before individual events become larger losses.

Step 3: Score Risk at the Moment of Action

Identity risk does not stay the same throughout the customer journey. Someone who looks completely legitimate during onboarding can become risky later, whether they log in from an unfamiliar device, attempt an account recovery, or initiate an unusually large transaction.

That is why risk evaluation should happen at the moments that matter most. Key touchpoints include KYC submission, login, device changes, password resets, payment method updates, promo redemption, transactions, withdrawals, and payouts.

Connected risk intelligence enables businesses to make smarter decisions in real time rather than treating every user and every action the same way.

Step 4: Apply Friction Based on Risk, Not Rules Alone

Since adding the same verification hurdles for every user can backfire, frustrating legitimate customers and increasing drop-offs, businesses need a more balanced approach.

A better model applies friction based on the level of risk.

Risk level | User scenario | Recommended action |

Low risk | Known user, trusted device, consistent behavior | Approve with minimal friction |

Medium risk | New device, unusual behavior, partial mismatch | Step-up verification |

High risk | Spoofed device, linked fraud pattern, deepfake risk | Block or send to review |

Network risk | Account linked to mule or fraud-ring cluster | Investigate connected accounts |

This approach helps risk teams stop fraud while helping product teams protect conversion. In fact, practitioner discussions around deepfake-enabled social engineering point in the same direction.

While discussing why teams should not rely only on detecting whether a voice, video, or image is fake, security professionals pointed out that the stronger approach is to add verification for sensitive actions through trusted channels, device-bound authentication, and step-up checks when the risk level changes.

Step 5: Use Feedback Loops to Improve Detection

Fraud patterns change quickly, so prevention systems need continuous learning. Feedback loops help teams improve detection without relying only on static rules.

Useful feedback inputs include confirmed fraud cases, false positives, manual review outcomes, chargebacks, account takeover reports, mule account findings, promo abuse patterns, compliance flags, and customer support escalations.

Over time, these inputs improve risk models, reduce false positives, and help teams respond faster to new AI-driven identity fraud patterns.

Taken together, these five steps create a more resilient approach to AI identity fraud prevention. To put this framework into practice effectively, risk teams need technology that can unify signals, surface hidden connections, and support real-time decisioning at scale.

How Bureau ID Helps Prevent AI-Driven Identity Fraud

Bureau ID helps businesses prevent AI-driven identity fraud by connecting identity, device, behavior, network, and transaction signals in one risk decisioning layer. Instead of treating document verification, device intelligence, account behavior, and fraud networks as separate checks, the platform helps risk teams evaluate the full context behind each user action.

Its role is especially relevant for high-risk digital businesses that face synthetic identity fraud, deepfake fraud prevention challenges, biometric spoofing, account takeover fraud, mule networks, and repeat abuse.

Bureau ID supports this through:

Unified Risk Decisioning: Bureau ID combines multiple risk signals through its platform, enabling real-time decisions across onboarding, authentication, and ongoing monitoring.

Device ID: The platform’s Device ID capability creates persistent device identifiers that help detect spoofed devices, emulators, VPN usage, repeat offenders, and device-account relationships.

Identity Document Verification: It helps validate user authenticity through biometric matching and liveness detection, reducing the risk of spoofing and impersonation attempts.

Behavioral Biometrics: It uses behavioral biometrics to analyze how users interact with devices to identify bots, scripted behavior, fraud farms, and suspicious sessions.

Graph Identity Network: Bureau ID's Graph Identity Network maps relationships between identities, devices, behaviors, phone numbers, emails, and accounts to uncover fraud rings, mule networks, and synthetic identity clusters.

No-Code Workflows: Risk teams can also configure rules, thresholds, review flows, and step-up actions using no-code workflows, reducing dependence on engineering resources for every change.

Explainable Decisions: Fraud investigators gain additional context through explainable decisions, which provide visibility into the signals and factors behind risk scores.

For high-risk digital businesses, this means moving beyond one-off verification checks and looking at the bigger picture. Instead of evaluating each event in isolation, teams can see how identity, device, and behavior signals connect in real time.

That makes it easier to spot AI-driven fraud whether it appears during signup, login, account recovery, transactions, or through repeat account creation.

Case Study: How Bureau ID Helped an Insurer Cut Fraud and Speed Up Onboarding by 30%

A leading insurance company was struggling with a growing number of fraudulent applications during onboarding. The challenge was finding a way to stop bad actors without creating more friction for genuine customers, increasing manual reviews, or slowing down the onboarding experience.

The insurer implemented Bureau ID’s fraud detection and identity intelligence capabilities to identify suspicious applications earlier in the onboarding journey. This allowed the company to flag fraudulent activity at the source while streamlining onboarding for legitimate applicants.

Within the first week, the company was able to:

Uncover and correct 100+ fraudulent or inaccurate applications.

Lower the volume of customer complaints related to unauthorized account activity.

Accelerate onboarding by 30%, helping improve conversion rates and customer satisfaction.

Replace a fraud-prone, high-friction onboarding process with a faster and more reliable customer experience.

Read the full case study here → A Leading Insurer Cuts Fraud to Drive 30% Faster Onboarding

A simple takeaway from this case study: businesses that combine identity verification with real-time fraud intelligence will be better positioned to protect customers, reduce losses, and maintain a seamless onboarding experience. The organizations that succeed will be those that treat identity fraud prevention as an ongoing strategy rather than a one-time check.

Stop AI Identity Fraud With Connected Risk Intelligence

The most dangerous AI-generated identity is often the one that looks completely legitimate.

Now that fraudsters can use AI to create convincing identities and behaviors that slip past isolated verification checks, the next step is to gain a connected view of risk, so your team can detect fraud patterns throughout the customer lifecycle.

By combining identity verification, device intelligence, behavioral biometrics, graph intelligence, and real-time risk decisioning in a single platform, Bureau ID helps businesses uncover hidden fraud signals, identify linked abuse, and stop sophisticated fraud before it impacts growth, revenue, or customer trust.

If you are looking to strengthen your defenses against AI-driven identity fraud, schedule a demo with Bureau ID today and explore how connected risk intelligence can help you detect, investigate, and prevent AI identity fraud at scale.

FAQs

1. What is AI identity fraud?

AI identity fraud is the use of artificial intelligence to fake, steal, or impersonate a person’s identity. Fraudsters use deepfakes, voice clones, fake documents, synthetic identities, and automated scripts to bypass KYC, open fake accounts, take over real accounts, and commit fraud.

2. How does AI identity fraud work?

AI identity fraud works by using AI-generated content and automation to make fake identities look real. Fraudsters may create realistic selfies, forge documents, clone voices, spoof video verification, or combine stolen personal data with synthetic details to pass onboarding and account checks.

3. What are the main types of AI identity fraud?

The main types of AI identity fraud include deepfake identity fraud, synthetic identity fraud, voice cloning scams, fake document fraud, account takeover, fake-account creation, and KYC bypass. These attacks often target onboarding, login, account recovery, payments, and high-risk transactions.

4. How can AI-generated documents bypass KYC checks?

AI-generated documents can bypass KYC checks when verification systems rely only on static document review or basic image matching. Fraudsters can alter IDs, create fake documents, pair them with deepfake selfies, and use scripted responses to make the identity appear legitimate.

5. How can businesses detect AI-generated identities?

Businesses can detect AI-generated identities by connecting identity, device, behavior, and network signals. Strong detection methods include liveness detection, document verification, device intelligence, behavioral biometrics, velocity checks, anomaly detection, risk scoring, and human review for high-risk cases.

6. How can companies build a multi-layered AI identity fraud prevention strategy?

Companies can prevent AI identity fraud by mapping fraud risk across the customer journey, connecting identity and device signals, scoring risk at key actions, applying friction based on risk, and improving detection through feedback loops. Platforms like Bureau ID help unify these signals to stop fraud without slowing legitimate users.

AI can now generate convincing fake identities, deepfake selfies, cloned voices, and synthetic account activity in minutes. As these tools become more accessible, businesses face a growing challenge: fraudsters can appear legitimate long enough to bypass traditional verification checks.

This is what makes AI identity fraud so dangerous. It extends beyond fake documents or stolen credentials and can surface across onboarding, login, account recovery, transactions, promo abuse, and coordinated fraud rings.

In this guide, we will explain what AI identity fraud is, the most common fraud types businesses need to stop, how these attacks bypass traditional identity verification, and what an effective AI identity fraud prevention framework should include.

What Is AI Identity Fraud?

AI identity fraud is the use of artificial intelligence to fake, steal, or misuse a person’s identity. Fraudsters use deepfakes, voice clones, synthetic identities, fake documents, and automated scripts to bypass identity verification, open fake accounts, take over real accounts, or commit financial crime.

Businesses detect and prevent AI identity fraud by connecting identity checks, device signals, behavioral patterns, liveness detection, risk scoring, and continuous monitoring across the customer journey.

Different AI-driven fraud methods tend to appear at different stages of the customer journey. For instance, during onboarding, fraudsters may use synthetic identities, fake documents, or deepfakes to get through verification. Later, they may rely on phishing, stolen credentials, or social engineering to take over legitimate accounts.

Deloitte Center for Financial Services estimates that GenAI-enabled fraud losses in the U.S. could rise to $40 billion by 2027, showing why AI identity fraud prevention now needs to be treated as a board-level risk.

Image Source: Deloitte Center for Financial Services

The effects go beyond direct fraud losses:

Higher onboarding fraud from convincing fake identities.

More account takeovers through AI-assisted attacks.

Increased manual reviews due to harder-to-spot fraud.

More false positives from broad fraud rules.

Greater exposure to mule accounts and fraud rings.

Higher compliance, financial, and reputational risk.

To prevent AI identity fraud effectively, businesses first need to understand the specific fraud patterns they are dealing with.

Related Read: A Buyer’s Guide To Fraud Detection Software For Fintech Teams

Common Types of AI Identity Fraud Businesses Need to Stop

AI identity fraud evolves quickly because fraudsters can adapt their tactics to different stages of the customer journey. Some attacks are designed to bypass onboarding checks, while others target existing accounts through login abuse, account recovery, transaction fraud, or promotional exploitation.

Understanding where and how these attacks occur helps businesses identify the trust signals being manipulated and build stronger defenses against them.

AI identity fraud type | What fraudsters do | Business risk |

Deepfake fraud | Use AI-generated or manipulated face, video, or voice media to impersonate a real person. | Bypass selfie checks, video KYC, human review, or support verification. |

AI-generated fake IDs | Create or alter identity documents using AI tools. | Pass weak document checks and open fraudulent accounts. |

Synthetic identity fraud | Combine real and fake identity details to create a new persona. | Access credit, wallets, accounts, or services with no intent to repay or comply. |

Biometric spoofing | Attack face, voice, or liveness systems using replays, masks, injections, or generated media. | Defeat biometric verification and impersonate legitimate users. |

Account takeover fraud | Use stolen credentials, AI phishing, or social engineering to access genuine accounts. | Move funds, change account details, steal data, or enable mule activity. |

Mule accounts and fraud rings | Use networks of linked accounts to move money, exploit offers, or hide coordinated abuse. | Individual users may appear legitimate while the network creates large-scale losses. |

Bot-driven fake account creation | Automate signups using synthetic data, proxies, emulators, or scripted behavior. | Increase promo abuse, spam, fake listings, scraping, and platform manipulation. |

These types often overlap in practice. A fraudster may use a synthetic identity during onboarding, a spoofed device to avoid detection, behavioral automation to scale signups, and linked accounts to exploit promotions or move money.

This is why identity checks cannot work in isolation anymore. Gartner predicted that by 2026, 30% of enterprises will no longer consider identity verification and authentication solutions reliable on their own because AI-generated deepfakes can undermine face biometrics.

For businesses, this reinforces the need to pair identity checks with device, behavior, network, and risk signals.

How AI Identity Fraud Bypasses Traditional Identity Verification

Traditional identity verification is still important, but it was not designed to catch every AI-driven fraud pattern on its own. A document check, selfie match, OTP, or password may confirm one part of the user journey, but AI identity fraud often works by exploiting the gaps between those checks.

Some of the most common weaknesses include:

Static document checks can be manipulated: AI-generated or altered documents can look realistic enough to pass basic review, especially when document checks are not connected to device, behavioral, and network signals.

Selfie and face-match checks can be attacked: Deepfake videos, face swaps, replay attacks, and injection attacks can target biometric flows, particularly when liveness detection is weak or isolated.

OTPs and passwords do not prove user trust: A fraudster with stolen credentials, SIM access, or social-engineered recovery access can still appear legitimate at login.

Rules alone miss adaptive fraud: Static rules may catch known patterns, but AI-enabled fraudsters can change devices, IPs, emails, phone numbers, and behavior to avoid simple thresholds.

Siloed tools create blind spots: A KYC tool may approve the identity, a device tool may detect risk, and a transaction tool may flag unusual activity later. If these signals are not connected, the business may miss the broader fraud pattern.

Individual reviews miss fraud rings: Many mule accounts, promo abuse rings, and synthetic identity clusters look harmless when reviewed one by one. The risk becomes visible only when businesses connect shared devices, phone numbers, emails, IPs, and behavioral patterns.

Bureau ID’s UK & EU Fraud Report found that 67% of organizations said siloed systems prevent early signal correlation. It also reported that 83% had observed AI or automation in attacks, which makes fragmented fraud controls even harder to rely on.

This is why identity verification needs to evolve from a one-time checkpoint into a continuous risk layer. Businesses need controls that evaluate whether the device, behavior, account history, and connected network support who the user claims to be.

AI Identity Fraud Prevention Technologies and Approaches

AI identity fraud is difficult to stop with isolated controls alone. Fraudsters attack from different angles, so businesses need a combination of connected capabilities that work together to build a complete picture of risk:

Identity Verification: Validates documents, selfies, biometrics, and other user-submitted information to confirm that a person is who they claim to be.

Document Forensics: Identifies signs of tampering, fake IDs, manipulated fields, and template-level inconsistencies that may indicate fraud.

Liveness and Face Intelligence: Detects spoofing attempts, deepfakes, replay attacks, and other forms of biometric manipulation.

Device Intelligence: Reveals spoofed devices, emulators, VPNs, proxies, repeat devices, and suspicious device-account relationships.

Behavioral Biometrics: Analyzes how users interact with their devices to detect bots, scripted behavior, fraud farms, and unusual session patterns.

Graph Intelligence: Uncovers hidden links between accounts, devices, emails, phone numbers, transactions, and known risk indicators that may not be visible through isolated checks.

Real-Time Risk Decisioning: Allows businesses to approve, reject, review, or step up users while they are still moving through the customer journey.

Adaptive Authentication: Introduces additional verification only when risk increases, helping balance security with user experience.

Most fraud signals become far more meaningful when they are viewed together rather than in isolation. For instance, a device anomaly on its own may not seem serious, but pair it with suspicious behavior, linked accounts, and unusual transaction activity, and a much clearer risk picture starts to emerge.

This is also where unified risk decisioning becomes especially valuable. Instead of forcing teams to piece together signals from multiple tools, Bureau ID brings device, behavior, identity, network, and transaction intelligence into a single real-time decisioning layer.

The result is a more complete view of risk and fewer blind spots that can allow AI-driven fraud to slip through unnoticed.

Related Read: A Modern Framework for Fraud Prevention in Middle East Banking

AI Identity Fraud Prevention Framework for High-Risk Digital Businesses

AI identity fraud prevention works best when businesses treat identity risk as a lifecycle problem. Effective prevention focuses on identifying risk as early as possible, connecting the right signals across the user journey, and making informed decisions at the moments where fraud can have the greatest impact.

Step 1: Map Fraud Risk Across the Customer Journey

Risk teams should first map where AI identity fraud can appear across the full user journey. This includes account signup, identity verification, login, password reset, account recovery, profile changes, payment method changes, promo redemption, transactions, withdrawals, payouts, and repeat account creation.

A simple mapping exercise can reveal where controls are too narrow.

Journey point | Possible AI identity fraud risk | Current control | Missing signal |

Signup | Synthetic identity or AI-generated ID | Document verification | Device and network intelligence |

KYC | Deepfake selfie or biometric spoof | Face match | Liveness and injection attack detection |

Login | Account takeover | Password and OTP | Device and behavioral risk |

Promo redemption | Multi-accounting | Basic eligibility rules | Device-account linking |

Transaction | Mule activity | Transaction rules | Graph and identity network signals |

This mapping gives risk teams actionable insights, and helps product teams understand where friction should stay low and where step-up checks make sense.

Step 2: Connect Identity, Device, Behavior, and Network Signals

Each signal becomes more useful when viewed in context.

A new account may look normal, but a new account from a device linked to 50 other accounts needs closer review.

Similarly, a clean selfie match may look valid, but a clean selfie match from a spoofed device with bot-like behavior should not receive the same decision as a trusted user on a known device.

Connected risk intelligence helps teams spot these patterns before individual events become larger losses.

Step 3: Score Risk at the Moment of Action

Identity risk does not stay the same throughout the customer journey. Someone who looks completely legitimate during onboarding can become risky later, whether they log in from an unfamiliar device, attempt an account recovery, or initiate an unusually large transaction.

That is why risk evaluation should happen at the moments that matter most. Key touchpoints include KYC submission, login, device changes, password resets, payment method updates, promo redemption, transactions, withdrawals, and payouts.

Connected risk intelligence enables businesses to make smarter decisions in real time rather than treating every user and every action the same way.

Step 4: Apply Friction Based on Risk, Not Rules Alone

Since adding the same verification hurdles for every user can backfire, frustrating legitimate customers and increasing drop-offs, businesses need a more balanced approach.

A better model applies friction based on the level of risk.

Risk level | User scenario | Recommended action |

Low risk | Known user, trusted device, consistent behavior | Approve with minimal friction |

Medium risk | New device, unusual behavior, partial mismatch | Step-up verification |

High risk | Spoofed device, linked fraud pattern, deepfake risk | Block or send to review |

Network risk | Account linked to mule or fraud-ring cluster | Investigate connected accounts |

This approach helps risk teams stop fraud while helping product teams protect conversion. In fact, practitioner discussions around deepfake-enabled social engineering point in the same direction.

While discussing why teams should not rely only on detecting whether a voice, video, or image is fake, security professionals pointed out that the stronger approach is to add verification for sensitive actions through trusted channels, device-bound authentication, and step-up checks when the risk level changes.

Step 5: Use Feedback Loops to Improve Detection

Fraud patterns change quickly, so prevention systems need continuous learning. Feedback loops help teams improve detection without relying only on static rules.

Useful feedback inputs include confirmed fraud cases, false positives, manual review outcomes, chargebacks, account takeover reports, mule account findings, promo abuse patterns, compliance flags, and customer support escalations.

Over time, these inputs improve risk models, reduce false positives, and help teams respond faster to new AI-driven identity fraud patterns.

Taken together, these five steps create a more resilient approach to AI identity fraud prevention. To put this framework into practice effectively, risk teams need technology that can unify signals, surface hidden connections, and support real-time decisioning at scale.

How Bureau ID Helps Prevent AI-Driven Identity Fraud

Bureau ID helps businesses prevent AI-driven identity fraud by connecting identity, device, behavior, network, and transaction signals in one risk decisioning layer. Instead of treating document verification, device intelligence, account behavior, and fraud networks as separate checks, the platform helps risk teams evaluate the full context behind each user action.

Its role is especially relevant for high-risk digital businesses that face synthetic identity fraud, deepfake fraud prevention challenges, biometric spoofing, account takeover fraud, mule networks, and repeat abuse.

Bureau ID supports this through:

Unified Risk Decisioning: Bureau ID combines multiple risk signals through its platform, enabling real-time decisions across onboarding, authentication, and ongoing monitoring.

Device ID: The platform’s Device ID capability creates persistent device identifiers that help detect spoofed devices, emulators, VPN usage, repeat offenders, and device-account relationships.

Identity Document Verification: It helps validate user authenticity through biometric matching and liveness detection, reducing the risk of spoofing and impersonation attempts.

Behavioral Biometrics: It uses behavioral biometrics to analyze how users interact with devices to identify bots, scripted behavior, fraud farms, and suspicious sessions.

Graph Identity Network: Bureau ID's Graph Identity Network maps relationships between identities, devices, behaviors, phone numbers, emails, and accounts to uncover fraud rings, mule networks, and synthetic identity clusters.

No-Code Workflows: Risk teams can also configure rules, thresholds, review flows, and step-up actions using no-code workflows, reducing dependence on engineering resources for every change.

Explainable Decisions: Fraud investigators gain additional context through explainable decisions, which provide visibility into the signals and factors behind risk scores.

For high-risk digital businesses, this means moving beyond one-off verification checks and looking at the bigger picture. Instead of evaluating each event in isolation, teams can see how identity, device, and behavior signals connect in real time.

That makes it easier to spot AI-driven fraud whether it appears during signup, login, account recovery, transactions, or through repeat account creation.

Case Study: How Bureau ID Helped an Insurer Cut Fraud and Speed Up Onboarding by 30%

A leading insurance company was struggling with a growing number of fraudulent applications during onboarding. The challenge was finding a way to stop bad actors without creating more friction for genuine customers, increasing manual reviews, or slowing down the onboarding experience.

The insurer implemented Bureau ID’s fraud detection and identity intelligence capabilities to identify suspicious applications earlier in the onboarding journey. This allowed the company to flag fraudulent activity at the source while streamlining onboarding for legitimate applicants.

Within the first week, the company was able to:

Uncover and correct 100+ fraudulent or inaccurate applications.

Lower the volume of customer complaints related to unauthorized account activity.

Accelerate onboarding by 30%, helping improve conversion rates and customer satisfaction.

Replace a fraud-prone, high-friction onboarding process with a faster and more reliable customer experience.

Read the full case study here → A Leading Insurer Cuts Fraud to Drive 30% Faster Onboarding

A simple takeaway from this case study: businesses that combine identity verification with real-time fraud intelligence will be better positioned to protect customers, reduce losses, and maintain a seamless onboarding experience. The organizations that succeed will be those that treat identity fraud prevention as an ongoing strategy rather than a one-time check.

Stop AI Identity Fraud With Connected Risk Intelligence

The most dangerous AI-generated identity is often the one that looks completely legitimate.

Now that fraudsters can use AI to create convincing identities and behaviors that slip past isolated verification checks, the next step is to gain a connected view of risk, so your team can detect fraud patterns throughout the customer lifecycle.

By combining identity verification, device intelligence, behavioral biometrics, graph intelligence, and real-time risk decisioning in a single platform, Bureau ID helps businesses uncover hidden fraud signals, identify linked abuse, and stop sophisticated fraud before it impacts growth, revenue, or customer trust.

If you are looking to strengthen your defenses against AI-driven identity fraud, schedule a demo with Bureau ID today and explore how connected risk intelligence can help you detect, investigate, and prevent AI identity fraud at scale.

FAQs

1. What is AI identity fraud?

AI identity fraud is the use of artificial intelligence to fake, steal, or impersonate a person’s identity. Fraudsters use deepfakes, voice clones, fake documents, synthetic identities, and automated scripts to bypass KYC, open fake accounts, take over real accounts, and commit fraud.

2. How does AI identity fraud work?

AI identity fraud works by using AI-generated content and automation to make fake identities look real. Fraudsters may create realistic selfies, forge documents, clone voices, spoof video verification, or combine stolen personal data with synthetic details to pass onboarding and account checks.

3. What are the main types of AI identity fraud?

The main types of AI identity fraud include deepfake identity fraud, synthetic identity fraud, voice cloning scams, fake document fraud, account takeover, fake-account creation, and KYC bypass. These attacks often target onboarding, login, account recovery, payments, and high-risk transactions.

4. How can AI-generated documents bypass KYC checks?

AI-generated documents can bypass KYC checks when verification systems rely only on static document review or basic image matching. Fraudsters can alter IDs, create fake documents, pair them with deepfake selfies, and use scripted responses to make the identity appear legitimate.

5. How can businesses detect AI-generated identities?

Businesses can detect AI-generated identities by connecting identity, device, behavior, and network signals. Strong detection methods include liveness detection, document verification, device intelligence, behavioral biometrics, velocity checks, anomaly detection, risk scoring, and human review for high-risk cases.

6. How can companies build a multi-layered AI identity fraud prevention strategy?

Companies can prevent AI identity fraud by mapping fraud risk across the customer journey, connecting identity and device signals, scoring risk at key actions, applying friction based on risk, and improving detection through feedback loops. Platforms like Bureau ID help unify these signals to stop fraud without slowing legitimate users.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.