6 Strategies Modern Platforms Use to Stop ATO Attacks

6 Strategies Modern Platforms Use to Stop ATO Attacks

6 Strategies Modern Platforms Use to Stop ATO Attacks

Explore account takeover prevention strategies, attack methods, and layered fraud defenses for banks, fintech apps, and digital platforms.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

Account takeover attacks rarely start with obvious fraud signals anymore. The credentials are often correct, MFA gets completed successfully, and the login looks legitimate. But somewhere between authentication and transaction activity, fraudsters quietly take control of the account.

That is why account takeover prevention has become a major priority for fintechs, digital banks, and platforms handling high-value transactions. Modern ATO attacks increasingly blend in with legitimate customer behavior, making standalone MFA and static fraud rules insufficient for detecting sophisticated login fraud or unauthorized account access in real time.

In this guide, we will break down how account takeover attacks work, the most common attack methods fraudsters use today, and the layered prevention strategies your team can use to stop ATO attacks.

How Do Account Takeover Attacks Work?

Account takeover attacks happen when fraudsters gain unauthorized access to legitimate customer accounts using stolen credentials, phishing, session hijacking, malware, or social engineering tactics. Once inside, attackers often exploit accounts for fraudulent transactions, identity abuse, payout manipulation, or account resale.

Modern ATO attacks are increasingly automated, making suspicious activity harder to detect during login itself. In fact, Verizon’s 2025 Data Breach Investigations Report found that credential abuse was the most common initial access vector in breaches at 22%, followed by vulnerability exploitation at 20% and phishing at 16%.

Most account takeover attacks follow a predictable lifecycle:

Credentials get exposed through phishing, malware, data breaches, or underground fraud marketplaces.

Credential stuffing bots test leaked usernames and passwords across banking, fintech, and e-commerce platforms.

Fraudsters gain account access using legitimate credentials.

Device anomalies, session switching, or unusual behavioral patterns begin appearing.

Fraudsters initiate sensitive actions like password resets, payout changes, or wallet transfers.

Funds move rapidly across linked accounts or mule networks before security teams can intervene.

Many of these attacks initially look like normal customer activity. Fraudsters increasingly combine automation, phishing, bots, session abuse, and device manipulation to bypass traditional authentication controls, which makes modern ATO attacks much harder to detect in real time.

Common Account Takeover Attack Methods

Modern account takeover attacks can enter through multiple points across the customer journey. Some target authentication flows directly, while others exploit weak recovery processes, compromised devices, or session vulnerabilities after login succeeds.

Understanding how these attack methods work is important because many fraud patterns only become visible when multiple signals start connecting together.

Credential stuffing attacks: Fraudsters reuse leaked username-password combinations across multiple platforms using automated bots. These attacks succeed largely because users continue reusing passwords across banking, fintech, e-commerce, and SaaS applications.

For instance, Bitwarden’s 2025 World Password Day survey found that 72% of Gen Z reuse passwords, and 59% reuse existing passwords even after updating accounts linked to a company breach. This explains why credential stuffing remains effective across consumer apps.

SIM swap fraud: Attackers manipulate telecom providers into transferring a victim’s phone number onto a fraudulent SIM card, allowing attackers to intercept OTPs, MFA codes, and account recovery messages.

Session hijacking and cookie theft: Malware, browser compromise, or stolen session tokens allow attackers to bypass login workflows entirely and gain access to active authenticated sessions without requiring credentials.

Phishing and social engineering: Fraudsters use fake banking pages, impersonation scams, vishing calls, and customer support manipulation to steal credentials or trick users into approving fraudulent login attempts.

Malware and device compromise: Banking trojans, keyloggers, remote access malware, and mobile banking malware silently capture credentials, session activity, and sensitive transaction data from infected devices.

MFA fatigue and OTP bypass attacks: Attackers repeatedly trigger MFA push notifications or OTP requests until users accidentally approve fraudulent login attempts or reveal authentication codes.

Bot-driven login attacks: Credential stuffing bots, headless browsers, and residential proxy networks mimic human browsing behavior to test stolen credentials at scale while bypassing basic CAPTCHA and WAF protections.

Account recovery abuse: Fraudsters exploit weak password reset flows and identity verification gaps during support interactions to gain unauthorized access to legitimate accounts.

As these attacks become more coordinated, suspicious activity often starts appearing across login behavior, device usage, session activity, and transaction flows. Those signals usually become the first indicators that a platform may already be exposed to ongoing ATO attempts.

Signs Your Platform May Be Exposed to ATO Attacks

Several operational signals often indicate rising account takeover risk:

Spikes in failed login attempts across multiple accounts

Multiple accounts linked to the same device fingerprint

High OTP retry or MFA failure rates

Impossible travel patterns or abnormal session switching

Password resets followed by unusual transactions

Sudden increases in bot-driven login traffic

These warning signs rarely appear in isolation. Fraud teams usually identify ATO risk when suspicious signals begin clustering together across authentication, behavior, devices, sessions, and transactions.

As attacks become more coordinated, layered fraud detection models combining device intelligence, behavioral biometrics, and graph-based fraud intelligence are becoming increasingly important for identifying high-risk activity in real time and strengthening account takeover prevention strategies.

Related Read: Compare Top Account Takeover Prevention Software and Build a Full-Stack ATO Defense

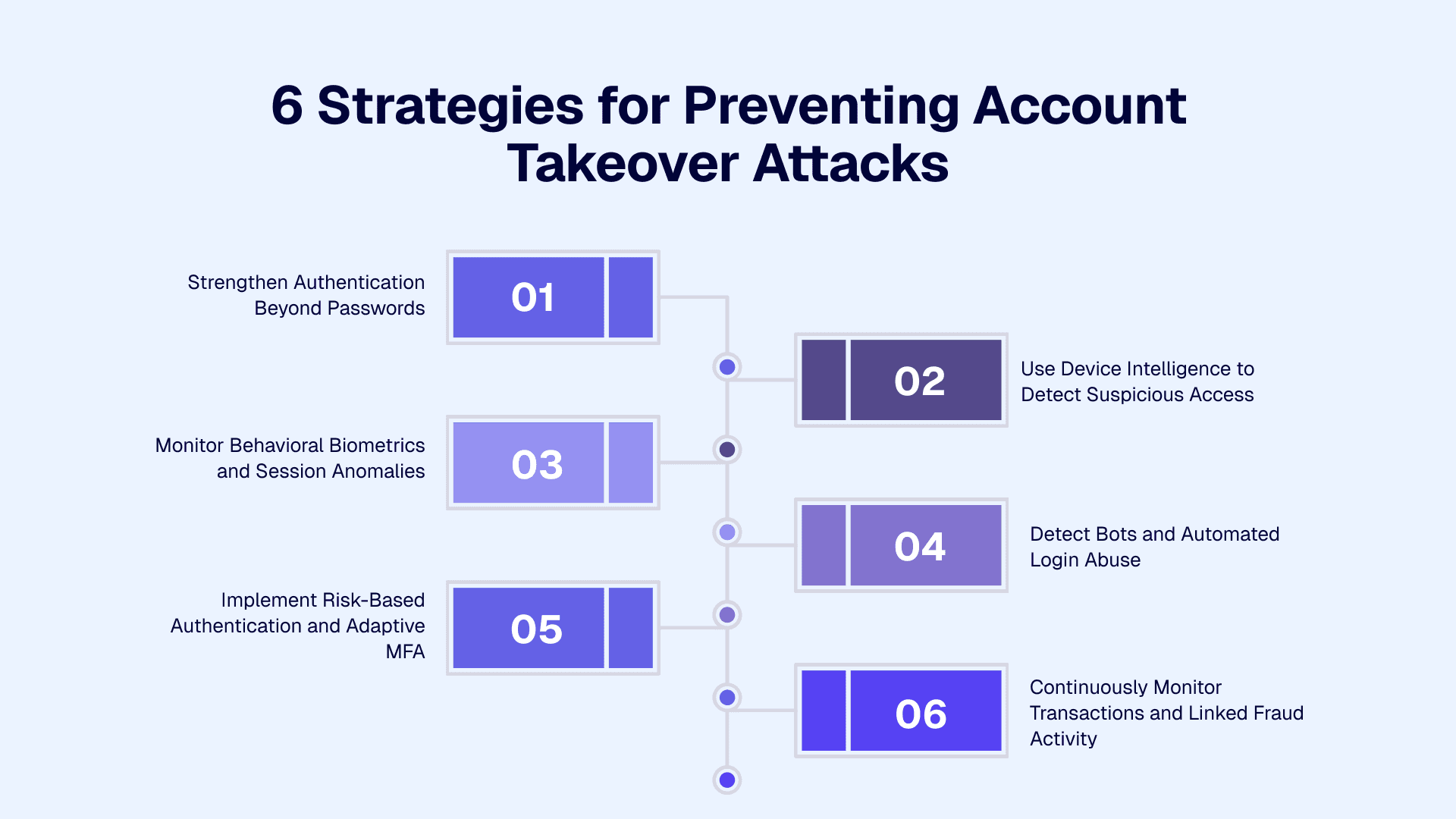

6 Strategies for Preventing Account Takeover Attacks

Effective account takeover prevention requires more than a strong login flow. Modern fraud teams increasingly rely on layered detection models that continuously evaluate authentication, device behavior, session activity, and transaction risk in real time.

The goal is to identify suspicious activity early without slowing down legitimate users across onboarding, login, or payments.

1. Strengthen Authentication Beyond Passwords

Passwords alone no longer provide reliable protection against account compromise, as fraudsters can steal, reuse, or purchase credentials through phishing campaigns, malware, and underground breach marketplaces. That is why many fintechs are moving toward FIDO2, WebAuthn, passkeys, and passwordless authentication models that reduce dependency on reusable credentials.

At the same time, MFA alone is no longer enough, because static MFA workflows often create friction while still remaining vulnerable to SIM swaps, OTP interception, and MFA fatigue attacks. Adaptive MFA works more effectively because authentication requirements increase only when suspicious risk signals appear during login or transaction activity.

2. Use Device Intelligence to Detect Suspicious Access

Device intelligence has become one of the most important layers in modern account takeover prevention. Persistent device fingerprinting helps fraud teams identify spoofed devices, emulator usage, VPN masking, TOR traffic, and repeat fraudsters attempting login abuse across multiple accounts.

This also helps improve customer experience for legitimate users. Trusted devices can move through authentication more smoothly, while unknown or suspicious devices trigger additional verification checks behind the scenes.

Platforms like Bureau ID increasingly focus on persistent device intelligence that remains effective even during incognito sessions, browser resets, or device manipulation attempts.

3. Monitor Behavioral Biometrics and Session Anomalies

Behavioral biometrics helps fraud teams evaluate how users interact with applications instead of relying only on login credentials. Typing speed, mouse movement, gesture analysis, navigation behavior, and session rhythm can often reveal suspicious activity long before account compromise becomes obvious.

This becomes especially important because many fraud indicators only appear after login succeeds. According to IBM's 2025 Cost of a Data Breach Report, breaches involving stolen or compromised credentials took 276 days to identify and contain, which underscores why continuous behavioral monitoring throughout the session is critical for detecting account compromise.

It helps identify bots, fraud farms, account sharing, and compromised sessions throughout the customer journey instead of limiting fraud checks to authentication alone. Strong behavioral analytics models also help reduce unnecessary friction for trusted users because risk evaluation happens passively in the background.

4. Detect Bots and Automated Login Abuse

Credential stuffing prevention increasingly depends on identifying sophisticated automation patterns. Fraudsters now use headless browsers, residential proxies, and human-like automation behavior that can bypass basic CAPTCHA systems and traditional login protections.

That is why standalone WAF protections are often not enough for modern ATO prevention. Effective bot detection combines behavioral analysis, device intelligence, network signals, and rate limiting to distinguish genuine users from automated login abuse.

Many fintechs now layer infrastructure-level protections with behavioral fraud detection to improve visibility into credential stuffing attacks and bot-driven login attempts.

5. Implement Risk-Based Authentication and Adaptive MFA

Risk-based authentication allows low-risk users to move through login flows with minimal friction while escalating verification only for suspicious sessions. This creates a more balanced approach to account takeover prevention because security controls adapt dynamically based on risk instead of applying the same authentication flow to every user.

Step-up verification often gets triggered during situations like:

New device access

Unusual geolocation activity

High-risk transactions

Behavioral anomalies

Beneficiary changes

Abnormal session switching

This approach helps fraud teams strengthen authentication controls without overwhelming legitimate users with repeated OTP requests or unnecessary MFA prompts during normal activity.

6. Continuously Monitor Transactions and Linked Fraud Activity

Many account takeover attacks only become visible after authentication succeeds. Bureau ID’s India Fraud Report notes that UPI processed 228 billion transactions worth ₹300 trillion in 2025, showing the scale at which real-time fraud detection must now operate across India’s digital finance ecosystem. Fraudsters often appear legitimate during login before initiating suspicious transfers, payout changes, or rapid fund movement across linked accounts.

Continuous monitoring helps fraud teams identify signals like:

Transaction velocity anomalies

Beneficiary updates

Linked account abuse

Mule account indicators

Behavioral drift after login

Coordinated fraud activity

This is where unified fraud decisioning becomes increasingly important. Platforms like Bureau ID combine device, behavioral, network, and transaction intelligence into centralized fraud orchestration workflows that help teams identify suspicious patterns earlier and respond to high-risk activity in real time.

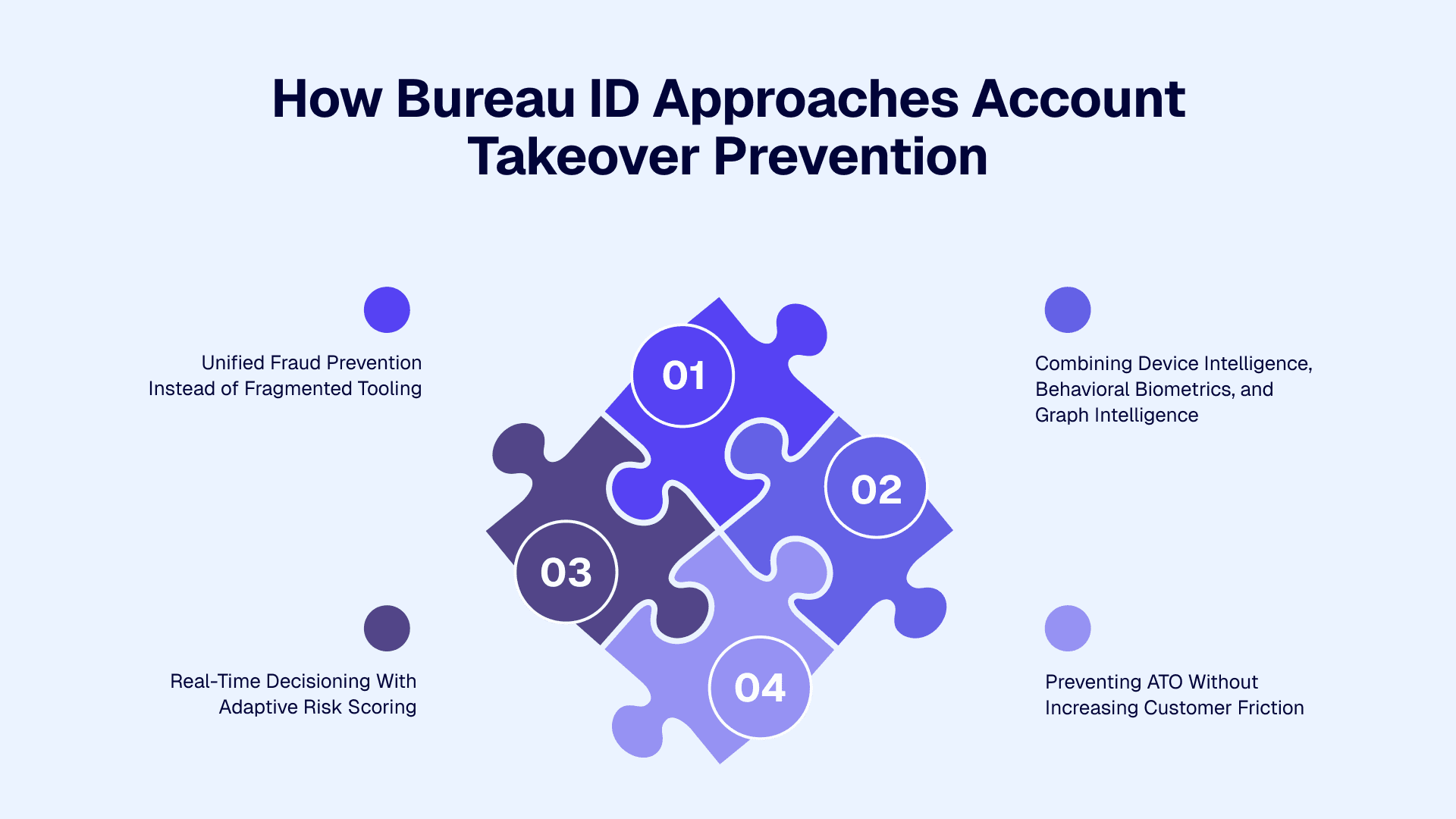

How Bureau ID Approaches Account Takeover Prevention

Modern account takeover prevention requires connected fraud intelligence across onboarding, login, sessions, transactions, and account recovery workflows. Bureau ID approaches this through a unified risk decisioning model that combines device, behavioral, network, and transactional signals into a centralized fraud prevention workflow.

Unified Fraud Prevention Instead of Fragmented Tooling

Many fintechs still manage onboarding, authentication, and transaction fraud through disconnected systems. That often creates operational blind spots because fraud signals remain siloed across teams and workflows.

Bureau ID combines identity, device, behavioral, network, and transaction intelligence into a single orchestration layer so fraud teams can evaluate risk more contextually instead of relying on isolated alerts.

This helps teams:

Correlate suspicious activity across the customer journey

Reduce operational inefficiencies from fragmented tooling

Improve visibility into linked fraud behavior

Respond faster to high-risk account activity

The result is a more connected approach to account takeover prevention that improves both fraud detection and operational decision-making.

Combining Device Intelligence, Behavioral Biometrics, and Graph Intelligence

Modern ATO attacks increasingly use legitimate credentials, which makes login success alone a weak trust signal. Bureau ID combines persistent device intelligence, behavioral biometrics, and graph intelligence to identify suspicious relationships between accounts, devices, fraud rings, and mule-linked activity.

The platform evaluates:

Device reputation and persistence

Behavioral anomalies during sessions

Linked account relationships

Repeat fraud patterns across ecosystems

This layered approach helps teams identify suspicious access patterns even when credentials appear valid. It also improves visibility into coordinated fraud activity that traditional authentication systems often miss, especially during large-scale credential stuffing or bot-driven login attacks.

Real-Time Decisioning With Adaptive Risk Scoring

Static fraud rules often struggle to keep up with evolving attack patterns. Bureau ID focuses on real-time risk decisioning models that continuously adapt based on live behavioral signals, linked fraud activity, and session-level anomalies instead of relying entirely on fixed authentication rules.

This allows fraud teams to:

Escalate verification only for high-risk sessions

Reduce unnecessary MFA prompts

Adjust fraud rules faster without engineering dependency

Improve visibility into suspicious transaction activity

The platform also supports explainable risk scoring and adaptive orchestration workflows, helping fraud teams make faster and more accurate decisions without adding operational complexity.

Preventing ATO Without Increasing Customer Friction

One of the biggest challenges in account takeover prevention is strengthening fraud controls without slowing down genuine users. Bureau ID uses layered risk intelligence and adaptive authentication workflows to evaluate suspicious behavior continuously in the background while allowing trusted users to move through onboarding and authentication more smoothly.

A strong example comes from Bureau ID’s fraud ring detection case study with a food delivery platform. Using Bureau ID’s Graph Identity Network, the platform identified coordinated fraud activity across thousands of linked accounts instead of catching fraudulent users one at a time.

Key outcomes included:

A 2,700+ user fraud ring operating through 150 devices was mapped and blocked

1,750+ accounts linked to just 3 devices were removed

97% of collusive users with high-risk scores were flagged for investigation

Repeat offenders were blocked to strengthen future fraud prevention workflows

Read the full case study here → Food Delivery Company Eliminates a 2,700+ User Fraud Ring

Protect Accounts With Layered Security

Fintechs and digital platforms increasingly need continuous visibility across authentication, devices, sessions, behavior, and transactions to identify suspicious activity before it escalates into account compromise or fraud losses.

Bureau ID helps fraud and risk teams approach this through unified fraud decisioning, behavioral intelligence, device risk analysis, adaptive authentication, and real-time orchestration workflows designed for modern digital platforms. Instead of relying on static rules alone, teams can evaluate risk continuously across the customer journey while reducing operational blind spots and unnecessary friction for trusted users.

If your team is evaluating gaps in its current ATO prevention strategy, this is a good time to assess whether your fraud stack can detect coordinated fraud activity in real time across login, onboarding, and transaction workflows.

Book a demo with Bureau ID to explore how unified risk decisioning can help strengthen account takeover prevention without slowing down genuine users.

FAQs

1. What is account takeover prevention?

Account takeover prevention is the process of protecting user accounts from unauthorized access caused by phishing, credential stuffing, bots, session hijacking, and stolen credentials. Modern account takeover prevention combines device intelligence, behavioral biometrics, adaptive authentication, AI risk scoring, and real-time monitoring to detect suspicious activity and stop fraud before attackers gain control of an account.

2. How do account takeover attacks happen?

Account takeover attacks typically start when fraudsters gain access to stolen usernames, passwords, session cookies, or OTPs through phishing, malware, credential stuffing, or social engineering. Attackers then attempt automated logins, bypass authentication controls, and take control of customer accounts to commit fraud, steal funds, or access sensitive information.

3. How can fintech companies prevent account takeover fraud?

Fintech companies prevent account takeover fraud by combining layered security controls such as device fingerprinting, behavioral biometrics, adaptive MFA, bot detection, and continuous session monitoring. Many fintech platforms also use AI-driven risk scoring and real-time fraud decisioning to identify suspicious login behavior without creating excessive friction for legitimate users.

4. How does behavioral biometrics help stop ATO attacks?

Behavioral biometrics helps stop ATO attacks by analyzing how users interact with devices during login and account activity. Systems monitor typing speed, swipe behavior, mouse movement, navigation patterns, and session behavior to identify anomalies that may indicate fraud. This approach improves fraud detection while reducing unnecessary authentication challenges for trusted users.

5. What role does device fingerprinting play in ATO prevention?

Device fingerprinting helps identify suspicious devices attempting unauthorized account access. Fraud prevention systems analyze browser settings, IP reputation, device configuration, geolocation mismatches, emulator usage, and network behavior to detect risky login attempts. Device intelligence adds an additional security layer beyond passwords and OTPs.

6. What are the best practices for preventing account takeover attacks?

The best practices for preventing account takeover attacks include strengthening authentication beyond passwords, implementing adaptive MFA, monitoring behavioral biometrics, detecting bots and automated login abuse, using device intelligence, and continuously monitoring transactions and session activity. Organizations also reduce risk by combining fraud detection signals into a unified real-time decisioning system.

Account takeover attacks rarely start with obvious fraud signals anymore. The credentials are often correct, MFA gets completed successfully, and the login looks legitimate. But somewhere between authentication and transaction activity, fraudsters quietly take control of the account.

That is why account takeover prevention has become a major priority for fintechs, digital banks, and platforms handling high-value transactions. Modern ATO attacks increasingly blend in with legitimate customer behavior, making standalone MFA and static fraud rules insufficient for detecting sophisticated login fraud or unauthorized account access in real time.

In this guide, we will break down how account takeover attacks work, the most common attack methods fraudsters use today, and the layered prevention strategies your team can use to stop ATO attacks.

How Do Account Takeover Attacks Work?

Account takeover attacks happen when fraudsters gain unauthorized access to legitimate customer accounts using stolen credentials, phishing, session hijacking, malware, or social engineering tactics. Once inside, attackers often exploit accounts for fraudulent transactions, identity abuse, payout manipulation, or account resale.

Modern ATO attacks are increasingly automated, making suspicious activity harder to detect during login itself. In fact, Verizon’s 2025 Data Breach Investigations Report found that credential abuse was the most common initial access vector in breaches at 22%, followed by vulnerability exploitation at 20% and phishing at 16%.

Most account takeover attacks follow a predictable lifecycle:

Credentials get exposed through phishing, malware, data breaches, or underground fraud marketplaces.

Credential stuffing bots test leaked usernames and passwords across banking, fintech, and e-commerce platforms.

Fraudsters gain account access using legitimate credentials.

Device anomalies, session switching, or unusual behavioral patterns begin appearing.

Fraudsters initiate sensitive actions like password resets, payout changes, or wallet transfers.

Funds move rapidly across linked accounts or mule networks before security teams can intervene.

Many of these attacks initially look like normal customer activity. Fraudsters increasingly combine automation, phishing, bots, session abuse, and device manipulation to bypass traditional authentication controls, which makes modern ATO attacks much harder to detect in real time.

Common Account Takeover Attack Methods

Modern account takeover attacks can enter through multiple points across the customer journey. Some target authentication flows directly, while others exploit weak recovery processes, compromised devices, or session vulnerabilities after login succeeds.

Understanding how these attack methods work is important because many fraud patterns only become visible when multiple signals start connecting together.

Credential stuffing attacks: Fraudsters reuse leaked username-password combinations across multiple platforms using automated bots. These attacks succeed largely because users continue reusing passwords across banking, fintech, e-commerce, and SaaS applications.

For instance, Bitwarden’s 2025 World Password Day survey found that 72% of Gen Z reuse passwords, and 59% reuse existing passwords even after updating accounts linked to a company breach. This explains why credential stuffing remains effective across consumer apps.

SIM swap fraud: Attackers manipulate telecom providers into transferring a victim’s phone number onto a fraudulent SIM card, allowing attackers to intercept OTPs, MFA codes, and account recovery messages.

Session hijacking and cookie theft: Malware, browser compromise, or stolen session tokens allow attackers to bypass login workflows entirely and gain access to active authenticated sessions without requiring credentials.

Phishing and social engineering: Fraudsters use fake banking pages, impersonation scams, vishing calls, and customer support manipulation to steal credentials or trick users into approving fraudulent login attempts.

Malware and device compromise: Banking trojans, keyloggers, remote access malware, and mobile banking malware silently capture credentials, session activity, and sensitive transaction data from infected devices.

MFA fatigue and OTP bypass attacks: Attackers repeatedly trigger MFA push notifications or OTP requests until users accidentally approve fraudulent login attempts or reveal authentication codes.

Bot-driven login attacks: Credential stuffing bots, headless browsers, and residential proxy networks mimic human browsing behavior to test stolen credentials at scale while bypassing basic CAPTCHA and WAF protections.

Account recovery abuse: Fraudsters exploit weak password reset flows and identity verification gaps during support interactions to gain unauthorized access to legitimate accounts.

As these attacks become more coordinated, suspicious activity often starts appearing across login behavior, device usage, session activity, and transaction flows. Those signals usually become the first indicators that a platform may already be exposed to ongoing ATO attempts.

Signs Your Platform May Be Exposed to ATO Attacks

Several operational signals often indicate rising account takeover risk:

Spikes in failed login attempts across multiple accounts

Multiple accounts linked to the same device fingerprint

High OTP retry or MFA failure rates

Impossible travel patterns or abnormal session switching

Password resets followed by unusual transactions

Sudden increases in bot-driven login traffic

These warning signs rarely appear in isolation. Fraud teams usually identify ATO risk when suspicious signals begin clustering together across authentication, behavior, devices, sessions, and transactions.

As attacks become more coordinated, layered fraud detection models combining device intelligence, behavioral biometrics, and graph-based fraud intelligence are becoming increasingly important for identifying high-risk activity in real time and strengthening account takeover prevention strategies.

Related Read: Compare Top Account Takeover Prevention Software and Build a Full-Stack ATO Defense

6 Strategies for Preventing Account Takeover Attacks

Effective account takeover prevention requires more than a strong login flow. Modern fraud teams increasingly rely on layered detection models that continuously evaluate authentication, device behavior, session activity, and transaction risk in real time.

The goal is to identify suspicious activity early without slowing down legitimate users across onboarding, login, or payments.

1. Strengthen Authentication Beyond Passwords

Passwords alone no longer provide reliable protection against account compromise, as fraudsters can steal, reuse, or purchase credentials through phishing campaigns, malware, and underground breach marketplaces. That is why many fintechs are moving toward FIDO2, WebAuthn, passkeys, and passwordless authentication models that reduce dependency on reusable credentials.

At the same time, MFA alone is no longer enough, because static MFA workflows often create friction while still remaining vulnerable to SIM swaps, OTP interception, and MFA fatigue attacks. Adaptive MFA works more effectively because authentication requirements increase only when suspicious risk signals appear during login or transaction activity.

2. Use Device Intelligence to Detect Suspicious Access

Device intelligence has become one of the most important layers in modern account takeover prevention. Persistent device fingerprinting helps fraud teams identify spoofed devices, emulator usage, VPN masking, TOR traffic, and repeat fraudsters attempting login abuse across multiple accounts.

This also helps improve customer experience for legitimate users. Trusted devices can move through authentication more smoothly, while unknown or suspicious devices trigger additional verification checks behind the scenes.

Platforms like Bureau ID increasingly focus on persistent device intelligence that remains effective even during incognito sessions, browser resets, or device manipulation attempts.

3. Monitor Behavioral Biometrics and Session Anomalies

Behavioral biometrics helps fraud teams evaluate how users interact with applications instead of relying only on login credentials. Typing speed, mouse movement, gesture analysis, navigation behavior, and session rhythm can often reveal suspicious activity long before account compromise becomes obvious.

This becomes especially important because many fraud indicators only appear after login succeeds. According to IBM's 2025 Cost of a Data Breach Report, breaches involving stolen or compromised credentials took 276 days to identify and contain, which underscores why continuous behavioral monitoring throughout the session is critical for detecting account compromise.

It helps identify bots, fraud farms, account sharing, and compromised sessions throughout the customer journey instead of limiting fraud checks to authentication alone. Strong behavioral analytics models also help reduce unnecessary friction for trusted users because risk evaluation happens passively in the background.

4. Detect Bots and Automated Login Abuse

Credential stuffing prevention increasingly depends on identifying sophisticated automation patterns. Fraudsters now use headless browsers, residential proxies, and human-like automation behavior that can bypass basic CAPTCHA systems and traditional login protections.

That is why standalone WAF protections are often not enough for modern ATO prevention. Effective bot detection combines behavioral analysis, device intelligence, network signals, and rate limiting to distinguish genuine users from automated login abuse.

Many fintechs now layer infrastructure-level protections with behavioral fraud detection to improve visibility into credential stuffing attacks and bot-driven login attempts.

5. Implement Risk-Based Authentication and Adaptive MFA

Risk-based authentication allows low-risk users to move through login flows with minimal friction while escalating verification only for suspicious sessions. This creates a more balanced approach to account takeover prevention because security controls adapt dynamically based on risk instead of applying the same authentication flow to every user.

Step-up verification often gets triggered during situations like:

New device access

Unusual geolocation activity

High-risk transactions

Behavioral anomalies

Beneficiary changes

Abnormal session switching

This approach helps fraud teams strengthen authentication controls without overwhelming legitimate users with repeated OTP requests or unnecessary MFA prompts during normal activity.

6. Continuously Monitor Transactions and Linked Fraud Activity

Many account takeover attacks only become visible after authentication succeeds. Bureau ID’s India Fraud Report notes that UPI processed 228 billion transactions worth ₹300 trillion in 2025, showing the scale at which real-time fraud detection must now operate across India’s digital finance ecosystem. Fraudsters often appear legitimate during login before initiating suspicious transfers, payout changes, or rapid fund movement across linked accounts.

Continuous monitoring helps fraud teams identify signals like:

Transaction velocity anomalies

Beneficiary updates

Linked account abuse

Mule account indicators

Behavioral drift after login

Coordinated fraud activity

This is where unified fraud decisioning becomes increasingly important. Platforms like Bureau ID combine device, behavioral, network, and transaction intelligence into centralized fraud orchestration workflows that help teams identify suspicious patterns earlier and respond to high-risk activity in real time.

How Bureau ID Approaches Account Takeover Prevention

Modern account takeover prevention requires connected fraud intelligence across onboarding, login, sessions, transactions, and account recovery workflows. Bureau ID approaches this through a unified risk decisioning model that combines device, behavioral, network, and transactional signals into a centralized fraud prevention workflow.

Unified Fraud Prevention Instead of Fragmented Tooling

Many fintechs still manage onboarding, authentication, and transaction fraud through disconnected systems. That often creates operational blind spots because fraud signals remain siloed across teams and workflows.

Bureau ID combines identity, device, behavioral, network, and transaction intelligence into a single orchestration layer so fraud teams can evaluate risk more contextually instead of relying on isolated alerts.

This helps teams:

Correlate suspicious activity across the customer journey

Reduce operational inefficiencies from fragmented tooling

Improve visibility into linked fraud behavior

Respond faster to high-risk account activity

The result is a more connected approach to account takeover prevention that improves both fraud detection and operational decision-making.

Combining Device Intelligence, Behavioral Biometrics, and Graph Intelligence

Modern ATO attacks increasingly use legitimate credentials, which makes login success alone a weak trust signal. Bureau ID combines persistent device intelligence, behavioral biometrics, and graph intelligence to identify suspicious relationships between accounts, devices, fraud rings, and mule-linked activity.

The platform evaluates:

Device reputation and persistence

Behavioral anomalies during sessions

Linked account relationships

Repeat fraud patterns across ecosystems

This layered approach helps teams identify suspicious access patterns even when credentials appear valid. It also improves visibility into coordinated fraud activity that traditional authentication systems often miss, especially during large-scale credential stuffing or bot-driven login attacks.

Real-Time Decisioning With Adaptive Risk Scoring

Static fraud rules often struggle to keep up with evolving attack patterns. Bureau ID focuses on real-time risk decisioning models that continuously adapt based on live behavioral signals, linked fraud activity, and session-level anomalies instead of relying entirely on fixed authentication rules.

This allows fraud teams to:

Escalate verification only for high-risk sessions

Reduce unnecessary MFA prompts

Adjust fraud rules faster without engineering dependency

Improve visibility into suspicious transaction activity

The platform also supports explainable risk scoring and adaptive orchestration workflows, helping fraud teams make faster and more accurate decisions without adding operational complexity.

Preventing ATO Without Increasing Customer Friction

One of the biggest challenges in account takeover prevention is strengthening fraud controls without slowing down genuine users. Bureau ID uses layered risk intelligence and adaptive authentication workflows to evaluate suspicious behavior continuously in the background while allowing trusted users to move through onboarding and authentication more smoothly.

A strong example comes from Bureau ID’s fraud ring detection case study with a food delivery platform. Using Bureau ID’s Graph Identity Network, the platform identified coordinated fraud activity across thousands of linked accounts instead of catching fraudulent users one at a time.

Key outcomes included:

A 2,700+ user fraud ring operating through 150 devices was mapped and blocked

1,750+ accounts linked to just 3 devices were removed

97% of collusive users with high-risk scores were flagged for investigation

Repeat offenders were blocked to strengthen future fraud prevention workflows

Read the full case study here → Food Delivery Company Eliminates a 2,700+ User Fraud Ring

Protect Accounts With Layered Security

Fintechs and digital platforms increasingly need continuous visibility across authentication, devices, sessions, behavior, and transactions to identify suspicious activity before it escalates into account compromise or fraud losses.

Bureau ID helps fraud and risk teams approach this through unified fraud decisioning, behavioral intelligence, device risk analysis, adaptive authentication, and real-time orchestration workflows designed for modern digital platforms. Instead of relying on static rules alone, teams can evaluate risk continuously across the customer journey while reducing operational blind spots and unnecessary friction for trusted users.

If your team is evaluating gaps in its current ATO prevention strategy, this is a good time to assess whether your fraud stack can detect coordinated fraud activity in real time across login, onboarding, and transaction workflows.

Book a demo with Bureau ID to explore how unified risk decisioning can help strengthen account takeover prevention without slowing down genuine users.

FAQs

1. What is account takeover prevention?

Account takeover prevention is the process of protecting user accounts from unauthorized access caused by phishing, credential stuffing, bots, session hijacking, and stolen credentials. Modern account takeover prevention combines device intelligence, behavioral biometrics, adaptive authentication, AI risk scoring, and real-time monitoring to detect suspicious activity and stop fraud before attackers gain control of an account.

2. How do account takeover attacks happen?

Account takeover attacks typically start when fraudsters gain access to stolen usernames, passwords, session cookies, or OTPs through phishing, malware, credential stuffing, or social engineering. Attackers then attempt automated logins, bypass authentication controls, and take control of customer accounts to commit fraud, steal funds, or access sensitive information.

3. How can fintech companies prevent account takeover fraud?

Fintech companies prevent account takeover fraud by combining layered security controls such as device fingerprinting, behavioral biometrics, adaptive MFA, bot detection, and continuous session monitoring. Many fintech platforms also use AI-driven risk scoring and real-time fraud decisioning to identify suspicious login behavior without creating excessive friction for legitimate users.

4. How does behavioral biometrics help stop ATO attacks?

Behavioral biometrics helps stop ATO attacks by analyzing how users interact with devices during login and account activity. Systems monitor typing speed, swipe behavior, mouse movement, navigation patterns, and session behavior to identify anomalies that may indicate fraud. This approach improves fraud detection while reducing unnecessary authentication challenges for trusted users.

5. What role does device fingerprinting play in ATO prevention?

Device fingerprinting helps identify suspicious devices attempting unauthorized account access. Fraud prevention systems analyze browser settings, IP reputation, device configuration, geolocation mismatches, emulator usage, and network behavior to detect risky login attempts. Device intelligence adds an additional security layer beyond passwords and OTPs.

6. What are the best practices for preventing account takeover attacks?

The best practices for preventing account takeover attacks include strengthening authentication beyond passwords, implementing adaptive MFA, monitoring behavioral biometrics, detecting bots and automated login abuse, using device intelligence, and continuously monitoring transactions and session activity. Organizations also reduce risk by combining fraud detection signals into a unified real-time decisioning system.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.