Top HyperVerge Alternatives for KYC, Onboarding, and Fraud Prevention

Top HyperVerge Alternatives for KYC, Onboarding, and Fraud Prevention

Top HyperVerge Alternatives for KYC, Onboarding, and Fraud Prevention

Explore the top HyperVerge competitors for KYC, AML, fraud prevention, and identity verification. Compare features, fraud detection, pricing, and APIs.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

HyperVerge has built a strong position around KYC onboarding, OCR, face match, and biometric verification workflows. But as onboarding volumes grow and fraud patterns become more sophisticated, many teams start looking for broader capabilities around fraud intelligence, decisioning, device signals, workflow flexibility, and lifecycle risk management.

In fact, Bureau ID’s UK & EU Fraud Report found that synthetic identity fraud increased by 50% while digital fraud attempts across the EU rose 43%, highlighting how onboarding fraud is shifting beyond document verification into coordinated identity, device, and behavioral attacks.

Capabilities like fraud intelligence, behavioral analytics, liveness detection, and real-time decisioning are becoming increasingly important as AI-driven fraud grows more sophisticated.

In this guide, we’ll compare the top HyperVerge competitors, where each platform fits best, and how fintech and BFSI teams evaluate identity verification vendors based on fraud prevention, onboarding workflows, compliance coverage, and lifecycle risk management.

HyperVerge Alternatives & Competitors Compared

HyperVerge competitors include identity verification and KYC vendors that support fraud prevention, biometric authentication, document verification, AML checks, and digital onboarding workflows.

Businesses compare these alternatives based on verification accuracy, onboarding speed, fraud detection depth, API integration, global coverage, and compliance support. The right platforms help reduce onboarding drop-offs, improve risk monitoring, and strengthen protection against synthetic identity fraud and AI-generated document attacks.

The challenge is that most platforms solve different parts of the onboarding and risk stack. While some focus heavily on KYC and document verification, others combine identity, fraud intelligence, device signals, and lifecycle decisioning into a broader trust layer.

Here’s a quick comparison of the top HyperVerge alternatives and where each platform fits best.

Tool | Best for | Core strength | Fraud capability | Integration complexity | Pricing model |

Bureau ID | Unified risk decisioning and network fraud prevention | Identity + fraud + device intellignece + behavior biometrics | High | Low to Moderate | Platform-based |

Persona | Custom onboarding flows | Configurable workflow builder | Moderate | Moderate | Usage-based |

Jumio | Regulated enterprise verification | AI-driven KYC with global compliance | Moderate | High | Enterprise/custom |

Entrust IDV | Global KYC and compliance | Document AI + biometrics | Moderate | Moderate | Per verification |

Veriff | High-assurance verification | Video KYC and face match accuracy | Moderate | Moderate to High | Per verification |

Trulioo | Cross-border verification | Global identity data coverage | Moderate | Moderate to High | Usage-based |

Shufti Pro | Fast deployment | Quick global document coverage | Low to Moderate | Low | Per verification |

IDfy | India-focused KYC | Local data and compliance workflows | Moderate | Moderate | Per verification / API |

Each platform solves a different layer of onboarding, compliance, and fraud prevention. The right choice usually depends on whether the primary challenge is onboarding accuracy, fraud prevention depth, global verification coverage, workflow flexibility, or full lifecycle risk decisioning.

Before we get to a detailed breakdown of each tool, let’s first look at how the evaluation criteria were used.

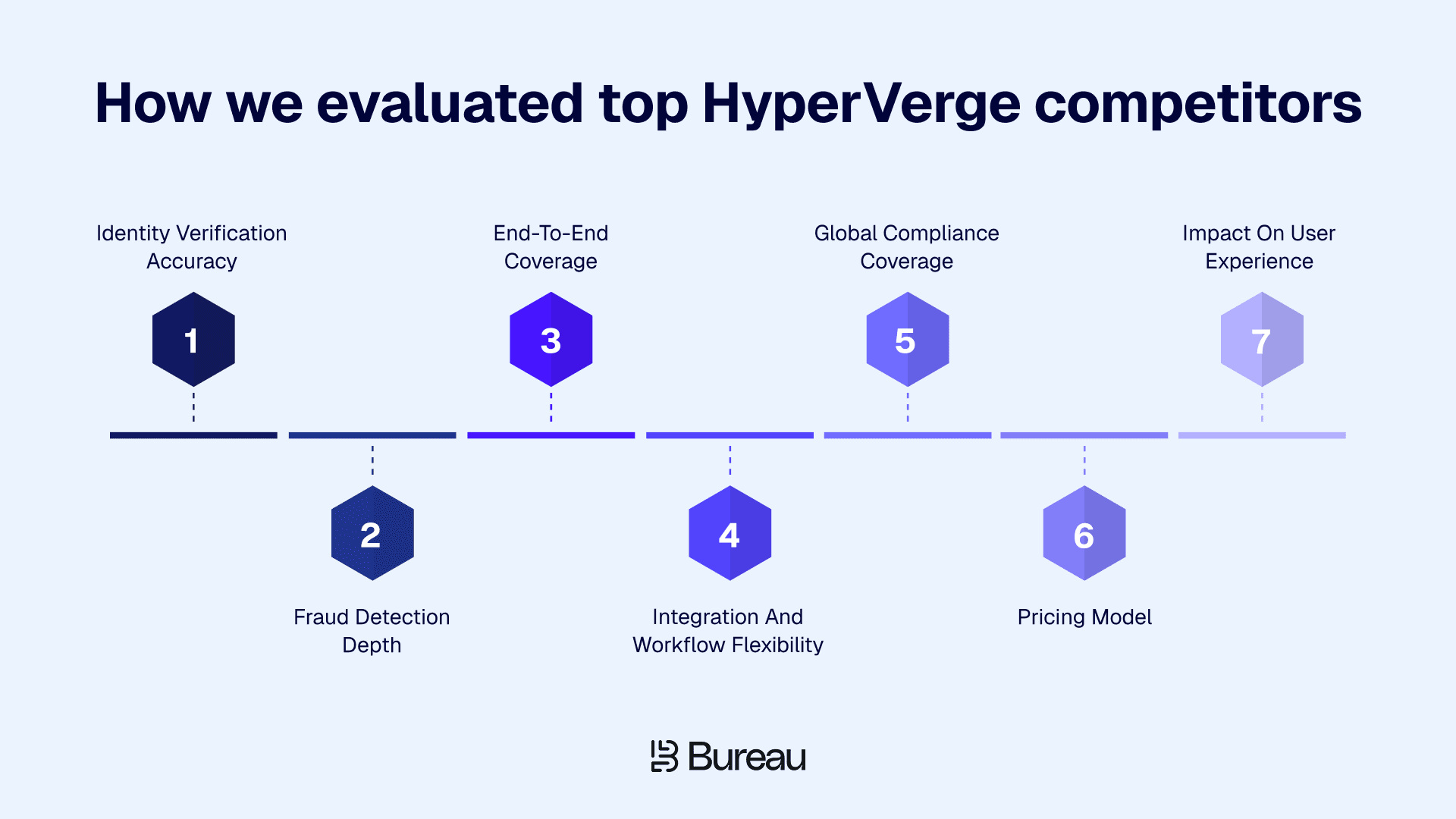

How We Evaluated the Top HyperVerge Competitors

This evaluation focuses on real onboarding and fraud prevention scenarios across fintech, lending, marketplaces, and BFSI workflows. Instead of treating these platforms as simple KYC vendors, we evaluated how they perform across various metrics:

Identity verification accuracy: OCR quality, biometric matching, document verification, and liveness detection performance. Verification accuracy directly affects onboarding approval rates, manual review volume, and customer drop-offs, especially in high-volume onboarding environments.

Fraud detection depth: Device intelligence, behavioral biometrics, fraud rings, and synthetic identity detection. Strong fraud intelligence becomes critical when onboarding fraud extends beyond fake documents into coordinated device activity, mule accounts, and AI-generated identities.

End-to-end coverage: Support across onboarding, authentication, transactions, and ongoing monitoring. Many fintech and BFSI teams now prefer platforms that monitor risk continuously instead of limiting fraud checks to the onboarding stage alone.

Integration and workflow flexibility: APIs, SDKs, orchestration, and no-code workflow management. Flexible workflows help risk and operations teams adjust onboarding logic quickly without depending heavily on engineering resources for every change.

Global compliance coverage: KYC, KYB, AML, sanctions, and regional onboarding requirements. Compliance needs vary significantly across regions, making local data coverage and regulatory alignment important evaluation criteria for scaling businesses.

Pricing model: Per verification pricing versus platform-based decisioning models. Pricing structure often impacts long-term scalability, especially for businesses handling high onboarding volumes or layering multiple fraud and compliance tools together.

Impact on user experience: Approval rates, onboarding speed, retry flows, and false declines. Strong onboarding experiences help businesses reduce abandonment rates while balancing fraud prevention with customer conversion goals.

India’s digital financial ecosystem processed 228 billion UPI transactions worth ₹300 trillion in 2025, according to Bureau ID’s 2026 India Fraud Report. As onboarding volumes scale at that pace, fraud detection increasingly depends on real-time risk orchestration across identity, device, behavioral, and transaction signals rather than isolated verification checks alone.

These are the same factors fintech and BFSI procurement teams increasingly prioritize as onboarding fraud becomes harder to detect through verification alone.

The right HyperVerge alternative ultimately depends on what your team is trying to solve beyond onboarding verification. For some businesses, the priority is global compliance coverage. For others, it is fraud intelligence, workflow flexibility, or lifecycle risk management.

With that context in mind, let’s look at the top HyperVerge competitors and where each platform fits best.

8 Best HyperVerge Competitors and Alternatives

1. Bureau ID

Bureau ID is an AI-powered unified risk decisioning platform built for businesses that need more than onboarding verification alone. Instead of treating identity verification, fraud detection, device intelligence, and transaction monitoring as separate workflows, Bureau combines them into a single orchestration layer. The platform evaluates user trust continuously across onboarding, authentication, and transactions, helping teams manage fraud and compliance from one system instead of stitching together multiple tools.

Teams use Bureau ID to replace fragmented onboarding, fraud, and risk systems with a unified decisioning platform that combines identity, device, behavioral, network, and transaction signals in real time.

Key strengths:

Unified decisioning platform: Bureau ID combines identity verification, fraud prevention, device intelligence, behavioral biometrics, and transaction monitoring into a single orchestration layer instead of requiring multiple vendors.

Device intelligence: The platform uses persistent device IDs with 99.97% persistence to detect repeat fraud attempts, emulator usage, spoofing, VPN masking, and multi-account abuse.

Behavioral biometrics: It continuously monitors user interaction patterns like typing behavior, touchscreen gestures, and navigation flow to detect fraud patterns that document verification alone may miss.

Graph Identity Network: Its proprietary network maps over 500M identities, devices, and behavioral relationships to uncover fraud rings, mule accounts, and synthetic identity activity in real time.

No-code workflow orchestration: Risk and operations teams can configure onboarding logic, tune risk thresholds, and adapt workflows without depending heavily on engineering resources.

Lifecycle risk coverage: Bureau ID supports onboarding, authentication, account protection, AML monitoring, and transaction-level risk decisions instead of limiting risk analysis to KYC checkpoints alone.

When teams choose it over HyperVerge:

KYC and OCR workflows pass verification checks, but downstream fraud still increases across onboarding and transactions

Fraud teams want device intelligence, behavioral analytics, and network-level fraud detection inside the same platform

Real-time decisioning becomes difficult when identity, fraud, and risk tools sit across multiple APIs and dashboards

High-risk onboarding environments like lending, BNPL, marketplaces, and gaming expose gaps in verification-only workflows

Internal teams want to reduce vendor sprawl and manage onboarding, fraud prevention, and compliance through one orchestration layer

What changes after adoption:

Faster onboarding: Genuine users move through onboarding faster while higher-risk users get flagged earlier in the flow.

Unified risk visibility: Identity, device, behavioral, and transaction signals stay connected within one operational layer instead of being fragmented across tools.

Real-time decisioning: Teams can trigger adaptive actions instantly during onboarding, login attempts, or transactions.

Lower fraud exposure: Device intelligence and network graph analysis improve detection of mule accounts, fraud rings, and synthetic identities.

Reduced operational overhead: No-code workflows allow fraud and operations teams to iterate without waiting on engineering cycles.

Improved explainability: Explainable risk scoring and audit-ready decision trails simplify compliance reviews and dispute handling.

That combination of onboarding speed, unified risk visibility, and real-time fraud decisioning is one of the main reasons Bureau positions itself differently from verification-first onboarding vendors. The platform focuses on reducing fraud without creating excessive friction for genuine users, especially in high-volume onboarding environments.

How Bureau ID helped a leading insurer reduce fraud and improve onboarding speed

The insurer was dealing with onboarding friction, fraud risk, and operational inefficiencies during customer acquisition. Existing onboarding workflows created delays for genuine users while still leaving gaps in fraud detection and risk visibility.

Bureau ID’s solution:

Unified onboarding verification and fraud screening into one decisioning workflow

Used device intelligence and behavioral signals to improve fraud detection accuracy

Automated onboarding decisions with configurable workflows and risk thresholds

Reduced dependency on manual reviews during customer onboarding

Results achieved:

30% faster onboarding speeds

Detected 100+ fake IDs and reduced fraud during onboarding workflows

Improved onboarding efficiency without increasing operational friction

You can read the full case study here → A Leading Insurer Cuts Fraud to Drive 30% Faster Onboarding

Additional AI and fraud capabilities:

Mule account detection: Bureau’s Mule Score framework identifies potential mule accounts during onboarding, monitoring, and real-time transaction flows.

Bot and emulator detection: The platform analyzes behavioral, device, and network signals to detect automated fraud attacks and scripted account creation attempts.

Alternative data underwriting: Bureau uses telecom, email, IP, device, and digital footprint signals to improve underwriting decisions for thin-file customers.

Location spoofing detection: IP intelligence and behavioral analysis help identify VPN masking, GPS spoofing, and suspicious location-switching activity.

Promo abuse prevention: Persistent device intelligence and graph analysis help detect multi-account abuse and referral fraud across marketplaces and eCommerce platforms.

Things to consider:

Bureau ID is designed primarily for fraud decisioning and lifecycle risk orchestration rather than lightweight standalone KYC workflows.

Teams get the most value when onboarding, fraud, and operational KPIs are clearly defined upfront.

Platform-based pricing is generally better suited for scaling onboarding volumes than low-volume verification use cases.

Best for: Fintechs, NBFCs, BNPL platforms, marketplaces, gaming platforms, and high-risk onboarding environments.

Pricing: Platform-based custom pricing.

2. Persona

Persona is a flexible identity verification platform built around configurable onboarding workflows. Instead of offering fixed onboarding templates, the platform allows teams to customize verification logic based on risk policies, geography, product type, or user segment. Many fintech and marketplace teams use Persona when they need more control over onboarding orchestration and user journeys rather than a packaged KYC workflow.

Key strengths:

Custom onboarding workflows: Persona allows teams to configure onboarding logic, verification steps, and risk flows around their own operational requirements.

Segment-based verification: Businesses can apply different onboarding rules based on geography, product type, transaction risk, or customer segment.

Flexible orchestration: The platform integrates with multiple third-party verification and fraud providers within a single workflow.

Developer-friendly APIs: Persona provides APIs and SDKs that support customized onboarding experiences across web and mobile environments.

Workflow visibility: Teams gain stronger visibility into onboarding decisions, retry logic, and user verification paths.

When buyers choose it over HyperVerge:

Teams need more configurable onboarding workflows instead of predefined KYC flows

Risk policies vary significantly across products, geographies, or customer segments

Businesses want flexibility to integrate multiple fraud and verification vendors together

Product and operations teams prioritize onboarding customization and orchestration visibility

Internal teams want greater control over verification logic without rebuilding workflows from scratch

Things to consider:

Workflow customization requires more setup and operational planning than packaged onboarding solutions

Fraud intelligence capabilities often depend on third-party integrations rather than built-in lifecycle decisioning

Teams with simpler onboarding needs may not fully use the platform’s orchestration flexibility

Best for: Fintechs, marketplaces, and businesses building highly customized onboarding workflows.

Pricing: Usage-based pricing.

3. Jumio

Jumio is an enterprise-grade identity verification platform built for regulated industries that require strong compliance workflows and audit-ready onboarding. The platform combines AI-driven document verification, biometric authentication, and AML capabilities with global onboarding support. Jumio is commonly evaluated by banks, fintechs, and enterprises operating across multiple regulated markets.

Key strengths:

AI-driven document verification: Jumio uses AI models to validate identity documents and detect manipulation attempts during onboarding.

Biometric authentication: The platform supports biometric matching and liveness detection for identity verification workflows.

Global compliance support: Jumio supports KYC, AML, and identity verification across multiple regions and regulatory environments.

Enterprise onboarding workflows: The platform is designed for regulated onboarding programs with audit-ready compliance requirements.

Global verification coverage: Businesses can onboard users across multiple countries using one onboarding infrastructure.

When buyers choose it over HyperVerge:

Compliance-heavy onboarding workflows require stronger enterprise governance and audit support

Businesses operate across multiple regulated international markets

Teams prioritize enterprise-scale KYC and AML coverage over onboarding flexibility

Banks and financial institutions require mature compliance infrastructure and SLAs

Global onboarding consistency matters more than localized onboarding optimization

Things to consider:

Enterprise onboarding and implementation cycles can take longer compared to lighter onboarding vendors

Pricing tends to be higher than API-first onboarding platforms

Fraud intelligence focuses more on verification and compliance than lifecycle fraud orchestration

Best for: Regulated industries, enterprise KYC programs, and global compliance workflows.

Pricing: Enterprise custom pricing.

4. Entrust IDV

Entrust IDV, formerly Onfido, focuses on AI-driven document verification and biometric authentication for global onboarding workflows. The platform combines document AI, facial biometrics, and liveness detection with Entrust’s broader enterprise identity portfolio. Many digital businesses evaluate Entrust IDV when they need strong document verification accuracy and global onboarding coverage across multiple markets.

Key strengths:

Document AI verification: Entrust IDV uses AI-based authenticity checks to validate government-issued identity documents.

Facial biometrics and liveness: The platform supports biometric verification and liveness detection to reduce impersonation attempts.

Global onboarding support: Businesses can onboard users across multiple regions using one verification infrastructure.

SDK and API integrations: Entrust IDV offers developer-friendly onboarding integrations across web and mobile applications.

Enterprise identity ecosystem: The platform benefits from Entrust’s broader identity and security portfolio.

When buyers choose it over HyperVerge:

Global onboarding requires broader document verification coverage

Enterprises need stronger international compliance workflows

Teams prioritize AI-driven document authenticity checks and biometric verification

Businesses operate across regions with varying onboarding requirements

Existing enterprise identity infrastructure already includes Entrust products

Things to consider:

The platform remains primarily verification-focused rather than lifecycle fraud decisioning-focused

Businesses often layer external fraud tools alongside Entrust IDV

Enterprise-scale pricing may not suit smaller onboarding programs

Best for: Enterprise-grade global KYC and identity verification workflows.

Pricing: Tiered per-verification pricing.

5. Veriff

Veriff is a global identity verification platform known for high-assurance video verification and face matching accuracy. The platform combines document verification, biometric authentication, and onboarding fraud checks within API-driven onboarding workflows. Businesses commonly evaluate Veriff when onboarding trust, verification precision, and international identity coverage become high operational priorities.

Key strengths:

Video verification accuracy: Veriff focuses heavily on video-based verification and biometric face matching workflows.

Global document coverage: The platform supports document verification across multiple countries and identity types.

Fraud signal detection: Veriff combines onboarding verification with fraud-related onboarding signals during verification flows.

API-led onboarding infrastructure: Businesses can integrate onboarding workflows into digital products through APIs and SDKs.

Cross-border onboarding: The platform supports onboarding across international customer bases and regulated markets.

When buyers choose it over HyperVerge:

High-assurance onboarding workflows require stronger video verification capabilities

International onboarding requires broad global verification coverage

Teams prioritize face match accuracy and liveness verification quality

Businesses want onboarding fraud checks alongside verification workflows

Verification precision matters more than lightweight onboarding speed

Things to consider:

Video-led onboarding workflows can create slightly more friction for users

Lifecycle fraud orchestration remains lighter compared to unified decisioning platforms

Complex onboarding environments may still require external fraud tooling

Best for: High-assurance onboarding and international identity verification.

Pricing: Per-verification pricing.

6. Trulioo

Trulioo is a cross-border identity verification platform built around extensive global identity data coverage. The platform supports KYC, KYB, AML screening, and international verification workflows through a broad network of global data partnerships. Businesses evaluating HyperVerge competitors often shortlist Trulioo when international onboarding scale and geographic coverage matter more than biometric-led verification alone.

Key strengths:

Global identity data coverage: Trulioo supports identity verification across multiple countries and regions using extensive data partnerships.

Cross-border onboarding support: Businesses can onboard international users through one verification infrastructure.

KYC and KYB workflows: The platform supports both individual and business verification workflows.

AML and watchlist screening: Teams can run sanctions checks and AML verification within onboarding flows.

Flexible API integrations: Trulioo offers APIs that support scalable onboarding integrations across markets.

When buyers choose it over HyperVerge:

Businesses operate across multiple international markets and geographies

Verification coverage matters more than biometric-heavy onboarding flows

Teams require broad AML, sanctions, and KYB capabilities

International onboarding scale becomes a priority

Cross-border regulatory coverage matters more than localized onboarding optimization

Things to consider:

Fraud detection focuses more heavily on data verification than behavioral or device intelligence

Integration complexity can increase across large multi-region implementations

Businesses seeking deep fraud orchestration may require additional tooling

Best for: Cross-border onboarding, international verification, and KYB workflows.

Pricing: Usage-based pricing.

7. Shufti Pro

Shufti Pro is a fast-deploy identity verification platform focused on quick onboarding setup and broad document coverage. The platform supports KYC verification, biometric checks, AML screening, and liveness detection through lightweight API integrations. Startups and digital businesses often evaluate Shufti Pro when onboarding speed and implementation simplicity matter more than advanced fraud orchestration.

Key strengths:

Fast deployment: Businesses can launch onboarding workflows quickly with relatively low integration overhead.

Global document coverage: The platform supports identity verification across multiple document types and regions.

Biometric verification: Shufti Pro includes biometric checks and liveness verification within onboarding workflows.

AML screening modules: Teams can add AML and sanctions checks during onboarding.

Simple API integration: Lightweight APIs make onboarding implementation relatively straightforward for smaller teams.

When buyers choose it over HyperVerge:

Businesses prioritize faster onboarding and deployment timelines

Teams want simpler onboarding integrations with lower setup complexity

International document coverage matters more than deep fraud intelligence

Smaller onboarding teams prefer lightweight operational workflows

Verification-first onboarding fits the current business stage

Things to consider:

Fraud intelligence depth is lighter compared to decisioning-focused platforms

Behavioral analytics and device intelligence capabilities remain limited

High-risk onboarding environments may still require separate fraud tooling

Best for: Fast deployment, lightweight onboarding, and global verification workflows.

Pricing: Per-verification pricing.

8. IDfy

IDfy is a strong India-focused HyperVerge alternative for regulated BFSI onboarding workflows. The platform focuses heavily on local compliance workflows, Aadhaar-aligned onboarding, and Indian verification infrastructure. Many fintechs, NBFCs, and financial institutions evaluate IDfy when India-specific onboarding compliance matters more than global onboarding scale.

Key strengths:

India-focused KYC workflows: IDfy supports onboarding flows aligned with Indian regulatory and compliance requirements.

Video KYC support: The platform provides Video KYC workflows commonly used across BFSI onboarding.

Local data integrations: IDfy connects with Indian verification databases and onboarding systems.

Document and biometric verification: Teams can run document checks, facial matching, and onboarding verification within one workflow.

Regulated onboarding support: The platform supports onboarding requirements commonly used across Indian BFSI environments.

When buyers choose it over HyperVerge:

India-first onboarding workflows require deeper local compliance alignment

Businesses prioritize Aadhaar-based verification and local data integrations

BFSI onboarding requires region-specific KYC infrastructure

Teams already operate within Indian onboarding ecosystems and workflows

Local compliance requirements matter more than global onboarding coverage

Things to consider:

Global onboarding capabilities remain more limited compared to international verification platforms

Fraud intelligence depth focuses more on onboarding verification than lifecycle decisioning

Businesses expanding internationally may require broader cross-border verification infrastructure

Best for: India-focused onboarding and BFSI compliance workflows.

Pricing: Per verification and API-based pricing.

Related Read: The Key Reasons Fraud Continues to Outpace Defenses in the UK and EU

Bureau ID vs HyperVerge: Side-by-Side Comparison

At first glance, Bureau ID and HyperVerge can look similar because both support identity verification and onboarding workflows. But the difference becomes clearer once fraud prevention, risk orchestration, and lifecycle monitoring enter the picture.

HyperVerge primarily focuses on onboarding verification through OCR, face match, and Video KYC workflows. Bureau ID takes a broader approach by combining identity, fraud intelligence, device signals, behavioral analytics, and decisioning into one operational layer that extends beyond onboarding.

Criteria | Bureau ID | HyperVerge |

Positioning | Unified risk decisioning platform | KYC and onboarding verification platform |

Core capability | Identity + fraud + device + behavior | OCR, face match, Video KYC |

Fraud intelligence | High, with graph + device + behavioral signals | Moderate, verification-led |

Real-time decisioning | Built-in explainable scoring | Often requires external systems |

Device intelligence | 99.97% persistent device ID | Not a core capability |

Behavioral biometrics | Yes | No |

Identity graph | 500M+ mapped identities | Not available |

Workflow orchestration | No-code configurable workflows | API-driven onboarding |

Vendor consolidation | High | Often paired with fraud tools |

Lifecycle coverage | Onboarding to transactions | Mostly onboarding |

Best fit | Fintechs, NBFCs, marketplaces | KYC-heavy onboarding |

When HyperVerge fits better

HyperVerge works well for teams whose primary focus is onboarding verification accuracy, OCR performance, and Video KYC workflows. It is often a strong fit when fraud prevention, transaction monitoring, or risk decisioning already sit in separate downstream systems.

When Bureau ID fits better

Bureau ID becomes more relevant when onboarding verification is only one part of the problem. Fintechs, lending platforms, gaming companies, and marketplaces often evaluate Bureau ID when they want onboarding, fraud prevention, authentication, and risk decisioning managed through one system instead of layering multiple tools together.

Gartner’s 2024 AI & Cybersecurity report predicted that by 2026, 30% of enterprises will no longer consider identity verification and authentication solutions reliable in isolation because of AI-generated deepfake attacks on face biometrics. The report specifically highlights device intelligence and behavioral analytics as increasingly important layers in modern onboarding and fraud prevention.

This usually becomes a priority when teams start dealing with synthetic identities, account takeovers, promo abuse, mule accounts, or high-risk onboarding flows that verification alone cannot fully address.

If you’re curious about how a unified decisioning platform would fit into your current onboarding and fraud stack, a 30-minute demo with Bureau ID can help map where identity verification, fraud detection, and operational workflows can be consolidated without adding more complexity.

Choose a stack built for the full risk lifecycle

When fraud teams realize verification alone cannot explain why risky users still keep getting through, many fintech and BFSI teams start rethinking their identity stack.

HyperVerge remains a strong choice for OCR, biometric verification, and Video KYC workflows. But if your team now needs fraud intelligence, device signals, behavioral analytics, and real-time decisioning inside the same system, Bureau ID is one of the strongest HyperVerge alternatives to evaluate.

Instead of adding more disconnected fraud and onboarding tools, Bureau focuses on consolidating onboarding, fraud prevention, authentication, and lifecycle risk management into one operational layer.

If you switch to Bureau ID, this is what the next steps look like:

Map onboarding and fraud gaps across your current stack

Consolidate fragmented verification and fraud workflows

Configure onboarding and risk rules around your fraud patterns

Improve approval rates without increasing fraud exposure

Reduce operational overhead through no-code orchestration

If you want to see how that would work inside your existing onboarding flow, schedule a demo with Bureau ID today, and evaluate your current setup, fraud gaps, and lifecycle risk workflows in more detail.

FAQs

1. What are the best HyperVerge competitors in 2026?

Some of the top HyperVerge competitors in 2026 include Bureau ID, Persona, Jumio, Entrust IDV, Veriff, Trulioo, Shufti Pro, and IDfy. These platforms support identity verification, KYC automation, AML screening, fraud prevention, and onboarding workflows. Businesses usually compare them based on fraud detection, global coverage, API integrations, pricing, and onboarding conversion.

2. Which HyperVerge alternative is best for fintech KYC?

The best HyperVerge alternative for fintech KYC depends on the use case. Bureau ID focuses on fraud prevention and risk orchestration across the onboarding lifecycle. Persona offers flexible workflow customization. Jumio and Trulioo provide broader global verification coverage. IDfy and Signzy are commonly evaluated for India-focused compliance and onboarding requirements.

3. How is Bureau ID different from HyperVerge?

Bureau ID focuses on connecting identity verification with broader fraud prevention and risk decisioning workflows. In addition to KYC and onboarding checks, it supports device intelligence, behavioral risk analysis, fraud orchestration, and lifecycle risk monitoring. Businesses evaluating HyperVerge competitors may consider Bureau ID when they want onboarding, fraud detection, and risk operations managed within a single stack.

4. Why do businesses choose Bureau ID for India-focused KYC?

Businesses choose Bureau ID for India-focused KYC because it supports onboarding workflows commonly used by fintechs, banks, NBFCs, and marketplaces in the region. The platform supports identity verification, fraud checks, onboarding automation, and risk-based decisioning while helping teams reduce onboarding friction and improve fraud detection during customer acquisition.

5. Why is it important to evaluate HyperVerge competitors?

Evaluating HyperVerge competitors helps businesses compare onboarding accuracy, fraud prevention capabilities, compliance coverage, integration flexibility, and pricing models. Different vendors specialize in different areas, such as India-focused KYC, global identity verification, AML screening, no-code workflows, or deepfake detection. Comparing platforms helps teams choose a solution that matches their fraud risk, regulatory requirements, onboarding scale, and customer experience goals.

6. Which HyperVerge alternative is best for deepfake and synthetic identity fraud detection?

Vendors like Bureau ID, Veriff, Persona, and Jumio focus heavily on AI-driven fraud detection, including deepfake detection, liveness verification, document tampering checks, and synthetic identity prevention. Businesses evaluating HyperVerge competitors increasingly prioritize these capabilities because AI-generated identity fraud continues to grow across digital onboarding workflows.

HyperVerge has built a strong position around KYC onboarding, OCR, face match, and biometric verification workflows. But as onboarding volumes grow and fraud patterns become more sophisticated, many teams start looking for broader capabilities around fraud intelligence, decisioning, device signals, workflow flexibility, and lifecycle risk management.

In fact, Bureau ID’s UK & EU Fraud Report found that synthetic identity fraud increased by 50% while digital fraud attempts across the EU rose 43%, highlighting how onboarding fraud is shifting beyond document verification into coordinated identity, device, and behavioral attacks.

Capabilities like fraud intelligence, behavioral analytics, liveness detection, and real-time decisioning are becoming increasingly important as AI-driven fraud grows more sophisticated.

In this guide, we’ll compare the top HyperVerge competitors, where each platform fits best, and how fintech and BFSI teams evaluate identity verification vendors based on fraud prevention, onboarding workflows, compliance coverage, and lifecycle risk management.

HyperVerge Alternatives & Competitors Compared

HyperVerge competitors include identity verification and KYC vendors that support fraud prevention, biometric authentication, document verification, AML checks, and digital onboarding workflows.

Businesses compare these alternatives based on verification accuracy, onboarding speed, fraud detection depth, API integration, global coverage, and compliance support. The right platforms help reduce onboarding drop-offs, improve risk monitoring, and strengthen protection against synthetic identity fraud and AI-generated document attacks.

The challenge is that most platforms solve different parts of the onboarding and risk stack. While some focus heavily on KYC and document verification, others combine identity, fraud intelligence, device signals, and lifecycle decisioning into a broader trust layer.

Here’s a quick comparison of the top HyperVerge alternatives and where each platform fits best.

Tool | Best for | Core strength | Fraud capability | Integration complexity | Pricing model |

Bureau ID | Unified risk decisioning and network fraud prevention | Identity + fraud + device intellignece + behavior biometrics | High | Low to Moderate | Platform-based |

Persona | Custom onboarding flows | Configurable workflow builder | Moderate | Moderate | Usage-based |

Jumio | Regulated enterprise verification | AI-driven KYC with global compliance | Moderate | High | Enterprise/custom |

Entrust IDV | Global KYC and compliance | Document AI + biometrics | Moderate | Moderate | Per verification |

Veriff | High-assurance verification | Video KYC and face match accuracy | Moderate | Moderate to High | Per verification |

Trulioo | Cross-border verification | Global identity data coverage | Moderate | Moderate to High | Usage-based |

Shufti Pro | Fast deployment | Quick global document coverage | Low to Moderate | Low | Per verification |

IDfy | India-focused KYC | Local data and compliance workflows | Moderate | Moderate | Per verification / API |

Each platform solves a different layer of onboarding, compliance, and fraud prevention. The right choice usually depends on whether the primary challenge is onboarding accuracy, fraud prevention depth, global verification coverage, workflow flexibility, or full lifecycle risk decisioning.

Before we get to a detailed breakdown of each tool, let’s first look at how the evaluation criteria were used.

How We Evaluated the Top HyperVerge Competitors

This evaluation focuses on real onboarding and fraud prevention scenarios across fintech, lending, marketplaces, and BFSI workflows. Instead of treating these platforms as simple KYC vendors, we evaluated how they perform across various metrics:

Identity verification accuracy: OCR quality, biometric matching, document verification, and liveness detection performance. Verification accuracy directly affects onboarding approval rates, manual review volume, and customer drop-offs, especially in high-volume onboarding environments.

Fraud detection depth: Device intelligence, behavioral biometrics, fraud rings, and synthetic identity detection. Strong fraud intelligence becomes critical when onboarding fraud extends beyond fake documents into coordinated device activity, mule accounts, and AI-generated identities.

End-to-end coverage: Support across onboarding, authentication, transactions, and ongoing monitoring. Many fintech and BFSI teams now prefer platforms that monitor risk continuously instead of limiting fraud checks to the onboarding stage alone.

Integration and workflow flexibility: APIs, SDKs, orchestration, and no-code workflow management. Flexible workflows help risk and operations teams adjust onboarding logic quickly without depending heavily on engineering resources for every change.

Global compliance coverage: KYC, KYB, AML, sanctions, and regional onboarding requirements. Compliance needs vary significantly across regions, making local data coverage and regulatory alignment important evaluation criteria for scaling businesses.

Pricing model: Per verification pricing versus platform-based decisioning models. Pricing structure often impacts long-term scalability, especially for businesses handling high onboarding volumes or layering multiple fraud and compliance tools together.

Impact on user experience: Approval rates, onboarding speed, retry flows, and false declines. Strong onboarding experiences help businesses reduce abandonment rates while balancing fraud prevention with customer conversion goals.

India’s digital financial ecosystem processed 228 billion UPI transactions worth ₹300 trillion in 2025, according to Bureau ID’s 2026 India Fraud Report. As onboarding volumes scale at that pace, fraud detection increasingly depends on real-time risk orchestration across identity, device, behavioral, and transaction signals rather than isolated verification checks alone.

These are the same factors fintech and BFSI procurement teams increasingly prioritize as onboarding fraud becomes harder to detect through verification alone.

The right HyperVerge alternative ultimately depends on what your team is trying to solve beyond onboarding verification. For some businesses, the priority is global compliance coverage. For others, it is fraud intelligence, workflow flexibility, or lifecycle risk management.

With that context in mind, let’s look at the top HyperVerge competitors and where each platform fits best.

8 Best HyperVerge Competitors and Alternatives

1. Bureau ID

Bureau ID is an AI-powered unified risk decisioning platform built for businesses that need more than onboarding verification alone. Instead of treating identity verification, fraud detection, device intelligence, and transaction monitoring as separate workflows, Bureau combines them into a single orchestration layer. The platform evaluates user trust continuously across onboarding, authentication, and transactions, helping teams manage fraud and compliance from one system instead of stitching together multiple tools.

Teams use Bureau ID to replace fragmented onboarding, fraud, and risk systems with a unified decisioning platform that combines identity, device, behavioral, network, and transaction signals in real time.

Key strengths:

Unified decisioning platform: Bureau ID combines identity verification, fraud prevention, device intelligence, behavioral biometrics, and transaction monitoring into a single orchestration layer instead of requiring multiple vendors.

Device intelligence: The platform uses persistent device IDs with 99.97% persistence to detect repeat fraud attempts, emulator usage, spoofing, VPN masking, and multi-account abuse.

Behavioral biometrics: It continuously monitors user interaction patterns like typing behavior, touchscreen gestures, and navigation flow to detect fraud patterns that document verification alone may miss.

Graph Identity Network: Its proprietary network maps over 500M identities, devices, and behavioral relationships to uncover fraud rings, mule accounts, and synthetic identity activity in real time.

No-code workflow orchestration: Risk and operations teams can configure onboarding logic, tune risk thresholds, and adapt workflows without depending heavily on engineering resources.

Lifecycle risk coverage: Bureau ID supports onboarding, authentication, account protection, AML monitoring, and transaction-level risk decisions instead of limiting risk analysis to KYC checkpoints alone.

When teams choose it over HyperVerge:

KYC and OCR workflows pass verification checks, but downstream fraud still increases across onboarding and transactions

Fraud teams want device intelligence, behavioral analytics, and network-level fraud detection inside the same platform

Real-time decisioning becomes difficult when identity, fraud, and risk tools sit across multiple APIs and dashboards

High-risk onboarding environments like lending, BNPL, marketplaces, and gaming expose gaps in verification-only workflows

Internal teams want to reduce vendor sprawl and manage onboarding, fraud prevention, and compliance through one orchestration layer

What changes after adoption:

Faster onboarding: Genuine users move through onboarding faster while higher-risk users get flagged earlier in the flow.

Unified risk visibility: Identity, device, behavioral, and transaction signals stay connected within one operational layer instead of being fragmented across tools.

Real-time decisioning: Teams can trigger adaptive actions instantly during onboarding, login attempts, or transactions.

Lower fraud exposure: Device intelligence and network graph analysis improve detection of mule accounts, fraud rings, and synthetic identities.

Reduced operational overhead: No-code workflows allow fraud and operations teams to iterate without waiting on engineering cycles.

Improved explainability: Explainable risk scoring and audit-ready decision trails simplify compliance reviews and dispute handling.

That combination of onboarding speed, unified risk visibility, and real-time fraud decisioning is one of the main reasons Bureau positions itself differently from verification-first onboarding vendors. The platform focuses on reducing fraud without creating excessive friction for genuine users, especially in high-volume onboarding environments.

How Bureau ID helped a leading insurer reduce fraud and improve onboarding speed

The insurer was dealing with onboarding friction, fraud risk, and operational inefficiencies during customer acquisition. Existing onboarding workflows created delays for genuine users while still leaving gaps in fraud detection and risk visibility.

Bureau ID’s solution:

Unified onboarding verification and fraud screening into one decisioning workflow

Used device intelligence and behavioral signals to improve fraud detection accuracy

Automated onboarding decisions with configurable workflows and risk thresholds

Reduced dependency on manual reviews during customer onboarding

Results achieved:

30% faster onboarding speeds

Detected 100+ fake IDs and reduced fraud during onboarding workflows

Improved onboarding efficiency without increasing operational friction

You can read the full case study here → A Leading Insurer Cuts Fraud to Drive 30% Faster Onboarding

Additional AI and fraud capabilities:

Mule account detection: Bureau’s Mule Score framework identifies potential mule accounts during onboarding, monitoring, and real-time transaction flows.

Bot and emulator detection: The platform analyzes behavioral, device, and network signals to detect automated fraud attacks and scripted account creation attempts.

Alternative data underwriting: Bureau uses telecom, email, IP, device, and digital footprint signals to improve underwriting decisions for thin-file customers.

Location spoofing detection: IP intelligence and behavioral analysis help identify VPN masking, GPS spoofing, and suspicious location-switching activity.

Promo abuse prevention: Persistent device intelligence and graph analysis help detect multi-account abuse and referral fraud across marketplaces and eCommerce platforms.

Things to consider:

Bureau ID is designed primarily for fraud decisioning and lifecycle risk orchestration rather than lightweight standalone KYC workflows.

Teams get the most value when onboarding, fraud, and operational KPIs are clearly defined upfront.

Platform-based pricing is generally better suited for scaling onboarding volumes than low-volume verification use cases.

Best for: Fintechs, NBFCs, BNPL platforms, marketplaces, gaming platforms, and high-risk onboarding environments.

Pricing: Platform-based custom pricing.

2. Persona

Persona is a flexible identity verification platform built around configurable onboarding workflows. Instead of offering fixed onboarding templates, the platform allows teams to customize verification logic based on risk policies, geography, product type, or user segment. Many fintech and marketplace teams use Persona when they need more control over onboarding orchestration and user journeys rather than a packaged KYC workflow.

Key strengths:

Custom onboarding workflows: Persona allows teams to configure onboarding logic, verification steps, and risk flows around their own operational requirements.

Segment-based verification: Businesses can apply different onboarding rules based on geography, product type, transaction risk, or customer segment.

Flexible orchestration: The platform integrates with multiple third-party verification and fraud providers within a single workflow.

Developer-friendly APIs: Persona provides APIs and SDKs that support customized onboarding experiences across web and mobile environments.

Workflow visibility: Teams gain stronger visibility into onboarding decisions, retry logic, and user verification paths.

When buyers choose it over HyperVerge:

Teams need more configurable onboarding workflows instead of predefined KYC flows

Risk policies vary significantly across products, geographies, or customer segments

Businesses want flexibility to integrate multiple fraud and verification vendors together

Product and operations teams prioritize onboarding customization and orchestration visibility

Internal teams want greater control over verification logic without rebuilding workflows from scratch

Things to consider:

Workflow customization requires more setup and operational planning than packaged onboarding solutions

Fraud intelligence capabilities often depend on third-party integrations rather than built-in lifecycle decisioning

Teams with simpler onboarding needs may not fully use the platform’s orchestration flexibility

Best for: Fintechs, marketplaces, and businesses building highly customized onboarding workflows.

Pricing: Usage-based pricing.

3. Jumio

Jumio is an enterprise-grade identity verification platform built for regulated industries that require strong compliance workflows and audit-ready onboarding. The platform combines AI-driven document verification, biometric authentication, and AML capabilities with global onboarding support. Jumio is commonly evaluated by banks, fintechs, and enterprises operating across multiple regulated markets.

Key strengths:

AI-driven document verification: Jumio uses AI models to validate identity documents and detect manipulation attempts during onboarding.

Biometric authentication: The platform supports biometric matching and liveness detection for identity verification workflows.

Global compliance support: Jumio supports KYC, AML, and identity verification across multiple regions and regulatory environments.

Enterprise onboarding workflows: The platform is designed for regulated onboarding programs with audit-ready compliance requirements.

Global verification coverage: Businesses can onboard users across multiple countries using one onboarding infrastructure.

When buyers choose it over HyperVerge:

Compliance-heavy onboarding workflows require stronger enterprise governance and audit support

Businesses operate across multiple regulated international markets

Teams prioritize enterprise-scale KYC and AML coverage over onboarding flexibility

Banks and financial institutions require mature compliance infrastructure and SLAs

Global onboarding consistency matters more than localized onboarding optimization

Things to consider:

Enterprise onboarding and implementation cycles can take longer compared to lighter onboarding vendors

Pricing tends to be higher than API-first onboarding platforms

Fraud intelligence focuses more on verification and compliance than lifecycle fraud orchestration

Best for: Regulated industries, enterprise KYC programs, and global compliance workflows.

Pricing: Enterprise custom pricing.

4. Entrust IDV

Entrust IDV, formerly Onfido, focuses on AI-driven document verification and biometric authentication for global onboarding workflows. The platform combines document AI, facial biometrics, and liveness detection with Entrust’s broader enterprise identity portfolio. Many digital businesses evaluate Entrust IDV when they need strong document verification accuracy and global onboarding coverage across multiple markets.

Key strengths:

Document AI verification: Entrust IDV uses AI-based authenticity checks to validate government-issued identity documents.

Facial biometrics and liveness: The platform supports biometric verification and liveness detection to reduce impersonation attempts.

Global onboarding support: Businesses can onboard users across multiple regions using one verification infrastructure.

SDK and API integrations: Entrust IDV offers developer-friendly onboarding integrations across web and mobile applications.

Enterprise identity ecosystem: The platform benefits from Entrust’s broader identity and security portfolio.

When buyers choose it over HyperVerge:

Global onboarding requires broader document verification coverage

Enterprises need stronger international compliance workflows

Teams prioritize AI-driven document authenticity checks and biometric verification

Businesses operate across regions with varying onboarding requirements

Existing enterprise identity infrastructure already includes Entrust products

Things to consider:

The platform remains primarily verification-focused rather than lifecycle fraud decisioning-focused

Businesses often layer external fraud tools alongside Entrust IDV

Enterprise-scale pricing may not suit smaller onboarding programs

Best for: Enterprise-grade global KYC and identity verification workflows.

Pricing: Tiered per-verification pricing.

5. Veriff

Veriff is a global identity verification platform known for high-assurance video verification and face matching accuracy. The platform combines document verification, biometric authentication, and onboarding fraud checks within API-driven onboarding workflows. Businesses commonly evaluate Veriff when onboarding trust, verification precision, and international identity coverage become high operational priorities.

Key strengths:

Video verification accuracy: Veriff focuses heavily on video-based verification and biometric face matching workflows.

Global document coverage: The platform supports document verification across multiple countries and identity types.

Fraud signal detection: Veriff combines onboarding verification with fraud-related onboarding signals during verification flows.

API-led onboarding infrastructure: Businesses can integrate onboarding workflows into digital products through APIs and SDKs.

Cross-border onboarding: The platform supports onboarding across international customer bases and regulated markets.

When buyers choose it over HyperVerge:

High-assurance onboarding workflows require stronger video verification capabilities

International onboarding requires broad global verification coverage

Teams prioritize face match accuracy and liveness verification quality

Businesses want onboarding fraud checks alongside verification workflows

Verification precision matters more than lightweight onboarding speed

Things to consider:

Video-led onboarding workflows can create slightly more friction for users

Lifecycle fraud orchestration remains lighter compared to unified decisioning platforms

Complex onboarding environments may still require external fraud tooling

Best for: High-assurance onboarding and international identity verification.

Pricing: Per-verification pricing.

6. Trulioo

Trulioo is a cross-border identity verification platform built around extensive global identity data coverage. The platform supports KYC, KYB, AML screening, and international verification workflows through a broad network of global data partnerships. Businesses evaluating HyperVerge competitors often shortlist Trulioo when international onboarding scale and geographic coverage matter more than biometric-led verification alone.

Key strengths:

Global identity data coverage: Trulioo supports identity verification across multiple countries and regions using extensive data partnerships.

Cross-border onboarding support: Businesses can onboard international users through one verification infrastructure.

KYC and KYB workflows: The platform supports both individual and business verification workflows.

AML and watchlist screening: Teams can run sanctions checks and AML verification within onboarding flows.

Flexible API integrations: Trulioo offers APIs that support scalable onboarding integrations across markets.

When buyers choose it over HyperVerge:

Businesses operate across multiple international markets and geographies

Verification coverage matters more than biometric-heavy onboarding flows

Teams require broad AML, sanctions, and KYB capabilities

International onboarding scale becomes a priority

Cross-border regulatory coverage matters more than localized onboarding optimization

Things to consider:

Fraud detection focuses more heavily on data verification than behavioral or device intelligence

Integration complexity can increase across large multi-region implementations

Businesses seeking deep fraud orchestration may require additional tooling

Best for: Cross-border onboarding, international verification, and KYB workflows.

Pricing: Usage-based pricing.

7. Shufti Pro

Shufti Pro is a fast-deploy identity verification platform focused on quick onboarding setup and broad document coverage. The platform supports KYC verification, biometric checks, AML screening, and liveness detection through lightweight API integrations. Startups and digital businesses often evaluate Shufti Pro when onboarding speed and implementation simplicity matter more than advanced fraud orchestration.

Key strengths:

Fast deployment: Businesses can launch onboarding workflows quickly with relatively low integration overhead.

Global document coverage: The platform supports identity verification across multiple document types and regions.

Biometric verification: Shufti Pro includes biometric checks and liveness verification within onboarding workflows.

AML screening modules: Teams can add AML and sanctions checks during onboarding.

Simple API integration: Lightweight APIs make onboarding implementation relatively straightforward for smaller teams.

When buyers choose it over HyperVerge:

Businesses prioritize faster onboarding and deployment timelines

Teams want simpler onboarding integrations with lower setup complexity

International document coverage matters more than deep fraud intelligence

Smaller onboarding teams prefer lightweight operational workflows

Verification-first onboarding fits the current business stage

Things to consider:

Fraud intelligence depth is lighter compared to decisioning-focused platforms

Behavioral analytics and device intelligence capabilities remain limited

High-risk onboarding environments may still require separate fraud tooling

Best for: Fast deployment, lightweight onboarding, and global verification workflows.

Pricing: Per-verification pricing.

8. IDfy

IDfy is a strong India-focused HyperVerge alternative for regulated BFSI onboarding workflows. The platform focuses heavily on local compliance workflows, Aadhaar-aligned onboarding, and Indian verification infrastructure. Many fintechs, NBFCs, and financial institutions evaluate IDfy when India-specific onboarding compliance matters more than global onboarding scale.

Key strengths:

India-focused KYC workflows: IDfy supports onboarding flows aligned with Indian regulatory and compliance requirements.

Video KYC support: The platform provides Video KYC workflows commonly used across BFSI onboarding.

Local data integrations: IDfy connects with Indian verification databases and onboarding systems.

Document and biometric verification: Teams can run document checks, facial matching, and onboarding verification within one workflow.

Regulated onboarding support: The platform supports onboarding requirements commonly used across Indian BFSI environments.

When buyers choose it over HyperVerge:

India-first onboarding workflows require deeper local compliance alignment

Businesses prioritize Aadhaar-based verification and local data integrations

BFSI onboarding requires region-specific KYC infrastructure

Teams already operate within Indian onboarding ecosystems and workflows

Local compliance requirements matter more than global onboarding coverage

Things to consider:

Global onboarding capabilities remain more limited compared to international verification platforms

Fraud intelligence depth focuses more on onboarding verification than lifecycle decisioning

Businesses expanding internationally may require broader cross-border verification infrastructure

Best for: India-focused onboarding and BFSI compliance workflows.

Pricing: Per verification and API-based pricing.

Related Read: The Key Reasons Fraud Continues to Outpace Defenses in the UK and EU

Bureau ID vs HyperVerge: Side-by-Side Comparison

At first glance, Bureau ID and HyperVerge can look similar because both support identity verification and onboarding workflows. But the difference becomes clearer once fraud prevention, risk orchestration, and lifecycle monitoring enter the picture.

HyperVerge primarily focuses on onboarding verification through OCR, face match, and Video KYC workflows. Bureau ID takes a broader approach by combining identity, fraud intelligence, device signals, behavioral analytics, and decisioning into one operational layer that extends beyond onboarding.

Criteria | Bureau ID | HyperVerge |

Positioning | Unified risk decisioning platform | KYC and onboarding verification platform |

Core capability | Identity + fraud + device + behavior | OCR, face match, Video KYC |

Fraud intelligence | High, with graph + device + behavioral signals | Moderate, verification-led |

Real-time decisioning | Built-in explainable scoring | Often requires external systems |

Device intelligence | 99.97% persistent device ID | Not a core capability |

Behavioral biometrics | Yes | No |

Identity graph | 500M+ mapped identities | Not available |

Workflow orchestration | No-code configurable workflows | API-driven onboarding |

Vendor consolidation | High | Often paired with fraud tools |

Lifecycle coverage | Onboarding to transactions | Mostly onboarding |

Best fit | Fintechs, NBFCs, marketplaces | KYC-heavy onboarding |

When HyperVerge fits better

HyperVerge works well for teams whose primary focus is onboarding verification accuracy, OCR performance, and Video KYC workflows. It is often a strong fit when fraud prevention, transaction monitoring, or risk decisioning already sit in separate downstream systems.

When Bureau ID fits better

Bureau ID becomes more relevant when onboarding verification is only one part of the problem. Fintechs, lending platforms, gaming companies, and marketplaces often evaluate Bureau ID when they want onboarding, fraud prevention, authentication, and risk decisioning managed through one system instead of layering multiple tools together.

Gartner’s 2024 AI & Cybersecurity report predicted that by 2026, 30% of enterprises will no longer consider identity verification and authentication solutions reliable in isolation because of AI-generated deepfake attacks on face biometrics. The report specifically highlights device intelligence and behavioral analytics as increasingly important layers in modern onboarding and fraud prevention.

This usually becomes a priority when teams start dealing with synthetic identities, account takeovers, promo abuse, mule accounts, or high-risk onboarding flows that verification alone cannot fully address.

If you’re curious about how a unified decisioning platform would fit into your current onboarding and fraud stack, a 30-minute demo with Bureau ID can help map where identity verification, fraud detection, and operational workflows can be consolidated without adding more complexity.

Choose a stack built for the full risk lifecycle

When fraud teams realize verification alone cannot explain why risky users still keep getting through, many fintech and BFSI teams start rethinking their identity stack.

HyperVerge remains a strong choice for OCR, biometric verification, and Video KYC workflows. But if your team now needs fraud intelligence, device signals, behavioral analytics, and real-time decisioning inside the same system, Bureau ID is one of the strongest HyperVerge alternatives to evaluate.

Instead of adding more disconnected fraud and onboarding tools, Bureau focuses on consolidating onboarding, fraud prevention, authentication, and lifecycle risk management into one operational layer.

If you switch to Bureau ID, this is what the next steps look like:

Map onboarding and fraud gaps across your current stack

Consolidate fragmented verification and fraud workflows

Configure onboarding and risk rules around your fraud patterns

Improve approval rates without increasing fraud exposure

Reduce operational overhead through no-code orchestration

If you want to see how that would work inside your existing onboarding flow, schedule a demo with Bureau ID today, and evaluate your current setup, fraud gaps, and lifecycle risk workflows in more detail.

FAQs

1. What are the best HyperVerge competitors in 2026?

Some of the top HyperVerge competitors in 2026 include Bureau ID, Persona, Jumio, Entrust IDV, Veriff, Trulioo, Shufti Pro, and IDfy. These platforms support identity verification, KYC automation, AML screening, fraud prevention, and onboarding workflows. Businesses usually compare them based on fraud detection, global coverage, API integrations, pricing, and onboarding conversion.

2. Which HyperVerge alternative is best for fintech KYC?

The best HyperVerge alternative for fintech KYC depends on the use case. Bureau ID focuses on fraud prevention and risk orchestration across the onboarding lifecycle. Persona offers flexible workflow customization. Jumio and Trulioo provide broader global verification coverage. IDfy and Signzy are commonly evaluated for India-focused compliance and onboarding requirements.

3. How is Bureau ID different from HyperVerge?

Bureau ID focuses on connecting identity verification with broader fraud prevention and risk decisioning workflows. In addition to KYC and onboarding checks, it supports device intelligence, behavioral risk analysis, fraud orchestration, and lifecycle risk monitoring. Businesses evaluating HyperVerge competitors may consider Bureau ID when they want onboarding, fraud detection, and risk operations managed within a single stack.

4. Why do businesses choose Bureau ID for India-focused KYC?

Businesses choose Bureau ID for India-focused KYC because it supports onboarding workflows commonly used by fintechs, banks, NBFCs, and marketplaces in the region. The platform supports identity verification, fraud checks, onboarding automation, and risk-based decisioning while helping teams reduce onboarding friction and improve fraud detection during customer acquisition.

5. Why is it important to evaluate HyperVerge competitors?

Evaluating HyperVerge competitors helps businesses compare onboarding accuracy, fraud prevention capabilities, compliance coverage, integration flexibility, and pricing models. Different vendors specialize in different areas, such as India-focused KYC, global identity verification, AML screening, no-code workflows, or deepfake detection. Comparing platforms helps teams choose a solution that matches their fraud risk, regulatory requirements, onboarding scale, and customer experience goals.

6. Which HyperVerge alternative is best for deepfake and synthetic identity fraud detection?

Vendors like Bureau ID, Veriff, Persona, and Jumio focus heavily on AI-driven fraud detection, including deepfake detection, liveness verification, document tampering checks, and synthetic identity prevention. Businesses evaluating HyperVerge competitors increasingly prioritize these capabilities because AI-generated identity fraud continues to grow across digital onboarding workflows.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.