Guide

For every legitimate transaction that gets completed in seconds, there’s a fraudster attempting to test stolen credentials, synthetic identities, or compromised gateways. The scale of payment fraud is staggering and continuously growing. According to Fintech Futures’ 2024 Global Online Payments Fraud Report , the global B2C eCommerce losses from online payment fraud will likely grow at a CAGR of +40% between 2023 and 2028.

Unlike account takeovers or promo abuse, payment fraud often hides behind legitimate credentials and trusted devices. Fraudsters don’t break the systems; they behave like real customers, bypassing rule-based engines and static blacklists.

For eCommerce businesses, striking a balance between frictionless experience and fraud prevention is a big challenge, as they must drive conversion while also defending against increasingly sophisticated, AI-powered attacks. Payment fraud detection, therefore, can no longer be a backend security function; it must be a core enabler of trust and sustainable growth in digital commerce. Which means the equation is: fraud detection through intelligent experience.

What is payment fraud in e-commerce

Payment fraud in eCommerce refers to any unauthorized transaction that results in stealing money, goods, or sensitive data during the online payment process. Unlike cyberattacks that disrupt systems, payment fraud targets the trust layer and exploits digital payment infrastructure, user behavior, and merchant vulnerabilities. As eCommerce becomes real-time and borderless, the sophistication of payment fraud continues to evolve from single-point breaches to coordinated, cross-channel operations.

Impersonation and manipulation form the core of payment fraud. Fraudsters often pose as customers using stolen or synthetic identities, manipulate checkout flows, or exploit weaknesses in card-not-present (CNP) channels or instant payment systems. Payment fraud not only impacts revenue, but also customer confidence, brand reputation, and regulatory standing.

Common types of payment fraud in eCommerce

Payment fraud can take many forms with the intensity varying by region. Regulatory maturity, consumer behavior, and preferred payment methods shape how it manifests across markets. Some of the common types of payment fraud in eCommerce are as described below:

Card-Not-Present (CNP) Fraud

CNP fraud occurs when fraudsters use stolen or synthetic card credentials to make unauthorized purchases online. It thrives on automation, bots, and scripts that test thousands of card numbers in parallel, until one works. The CNP fraud is most prevalent in North America, APAC, and Australia, where eCommerce and mobile checkout dominate. Despite 3D Secure and tokenization, Australia reported AUD $913 million in CNP losses in 2024, highlighting persistent vulnerabilities in high-volume, low-friction payment environments.

Authorized Push Payment (APP) Scams

In APP scams, fraudsters impersonate trusted parties, such as banks, vendors, or customer support and trick victims into transferring funds to fraudulent accounts. Because customers initiate the transfer, traditional controls often fail to block it. Concentrated in the UK and Europe, APP scams are driven by instant-payment rails like Faster Payments and SEPA Instant. According to the UK Payment Systems Regulator (PSR), £341 million in APP scam losses were recorded in 2023.

Account Takeover (ATO) Fraud

ATO fraud involves unauthorized access to legitimate user accounts via stolen credentials or credential stuffing attacks. Fraudsters then use stored cards, saved addresses, and loyalty points to make fraudulent purchases undetected. ATO fraud is a frequent occurrence in North America, MENA, and Latin America, where credential reuse is common and businesses heavily rely on password-based logins.

Refund and Chargeback Abuse

Also known as friendly fraud, refund and chargeback abuse occurs when customers falsely claim non-delivery or dispute legitimate charges to obtain refunds while retaining the product. This fraud type is widespread in Europe and North America, where consumer protections favor buyers and frictionless refund policies are common. Subscription and BNPL merchants face maximum losses, as repeated low-value disputes often go unnoticed.

Synthetic Identity Fraud

Fraudsters stitch together real and fake identity elements, such as valid government ID numbers, false emails, and use burner devices to create hybrid personas that pass KYC checks, open new accounts, and generate high downstream fraud losses. Synthetic identity fraud is particularly rampant in the US, Latin America, and emerging APAC markets. This is due to fragmented credit bureaus and growing digital onboarding pipelines making identity stitching easier.

Triangulation Fraud

Accelerated by the rise of social commerce, triangulation fraud is a multi-layered scheme. Fraudsters set up fake storefronts to accept orders using stolen cards. They then fulfill the orders via legitimate retailers using different stolen payment details, masking the origin. Common in North America and Europe, where high consumer trust in marketplace platforms allows fake merchants to operate briefly before detection.

Payment Gateway Fraud

Fraudsters exploit vulnerabilities in poorly secured or unverified payment gateways to inject malicious code, intercept API calls, or use stolen merchant credentials for fake transactions. It is more frequent in APAC and MENA, where smaller or emerging eCommerce platforms usually lack advanced encryption or monitoring tools.

SMS and Phishing-based Payment Scams

Attackers send deceptive messages or links mimicking banks, courier services, or marketplaces to trick consumers into revealing card details or OTPs. This type of fraud is heavily concentrated in Asia-Pacific, MENA, and Latin America, as mobile-first consumers often transact through chat-based or informal platforms with weaker buyer protections.

Account Enumeration and Bot-driven Testing Attacks

Fraudsters use automated bots to test stolen card or credential combinations across multiple eCommerce sites until a match is found. AI-powered bots can mimic human typing speed and browsing behavior, evading legacy detection systems. Even failed attempts can harm merchants by triggering chargebacks or inflated authorization costs. This type of fraud is more common in North America, Europe, and Australia, where card-issuing networks and payment processors have broad digital exposure.

How payment fraud impacts the eCommerce ecosystem

Payment fraud doesn’t just drain revenue, it also erodes trust, increases operational costs, and destabilizes the foundations of digital commerce. Its ripple effects touch every participant in the payment chain, from merchants and acquirers to payment service providers (PSPs) and consumers. The losses extend beyond chargebacks or refunds to reputational damage, customer churn, and regulatory scrutiny.

Impact on Businesses and Merchants

Every fraudulent transaction translates into direct financial loss. It drives up chargeback ratios, often crossing thresholds set by card networks. This triggers penalties, stricter monitoring programs, or even termination of merchant accounts. It also adds to covert losses in the form of operational overheads. These include additional authentication hoops, customer dispute resolution, and compliance audits. Stricter fraud control measures may lead to false declines, further eroding conversion rates and customer trust. The stakes are even higher for global eCommerce brands, as fraudulent activity in one geography can cascade into higher authorization costs and damaged relationships with global acquirers.

Impact on payment service providers (PSPs) and acquirers

Payment processors, gateways, and acquirers sit at the heart of the digital transaction flow; and, therefore, absorb a disproportionate share of risk when fraud volumes surge.

Every fraudulent payment impacts authorization performance and fraud ratio, directly affecting reputation and compliance with the card network rules. To stay competitive, PSPs invest in fraud monitoring infrastructure, data-sharing partnerships, and real-time risk scoring, costs that smaller providers often struggle to bear.

Additionally, the liability frameworks differ across markets. In some regions, acquirers share responsibility with merchants for fraudulent transactions. In the UK, for example, the Payment Systems Regulator’s APP reimbursement rules require PSPs to share liability for authorized push payment scams, significantly reshaping accountability across the payment stack

Impact on banks and issuers

Banks and card issuers face the dual challenge of fraud reimbursement and customer retention. Every disputed charge triggers not just investigation costs but also the potential loss of trust in the issuer’s security protocols.

In regulated markets like the EU and the US, failure to maintain adequate fraud safeguards can invite regulatory enforcement or fines under PSD2 or the FTC’s unfair practices framework. Issuers, therefore, invest in advanced transaction monitoring, device-level identity verification, and AI-based anomaly detection to fight repeated attacks. This leads to an increase in compliance and operational costs.

Impact on consumers

Consumers pay the emotional and practical price of fraud. Victims of unauthorized transactions face financial loss, account lockouts, and delayed reimbursements, often with limited clarity on who bears the responsibility.

Equally damaging is the erosion of trust in digital channels. When consumers perceive online transactions as unsafe, they abandon digital wallets or revert to cash-on-delivery options. This can reverse years of progress in payment modernization. Moreover, widespread phishing and SMS fraud disproportionately affect first-time or mobile-first users in emerging markets, widening the trust gap in digital inclusion.

Impact on the broader eCommerce ecosystem

The effects of payment fraud ripple outward.

Marketplaces suffer reputational damage when fraudulent listings or transactions grow.

Logistics partners face returns abuse and delivery rerouting from fake orders.

Regulators tighten compliance, raising the bar, and costs, for all participants.

Fintech lenders and BNPL providers struggle with inflated default rates driven by synthetic or mule-linked identities.

How fraudsters execute these fraud types

In eCommerce, fraud starts long before checkout: in data breaches, dark web markets, and social channels. Here, stolen identities and payment credentials circulate freely. Fraudsters use automation, AI, and social engineering to exploit merchant systems, mimic shopper behavior, and blend real and synthetic data to evade detection.

Here’s how the playbook for these fraud types usually looks:

Card-Not-Present (CNP)

Acquire data: Purchase card dumps or stolen credentials on dark web marketplaces, or harvest via skimmers, breaches, or phishing.

Validate: Use low-value transactions or authorization probes across multiple merchants to test and verify card validity and AVS/3DS behavior.

Scale attacks: Once validated, launch high-value purchases or bulk automated purchases via botnets or sneaker-bot frameworks.

Cash out: Ship goods to mule addresses or forward to drop networks; resell on secondary marketplaces.

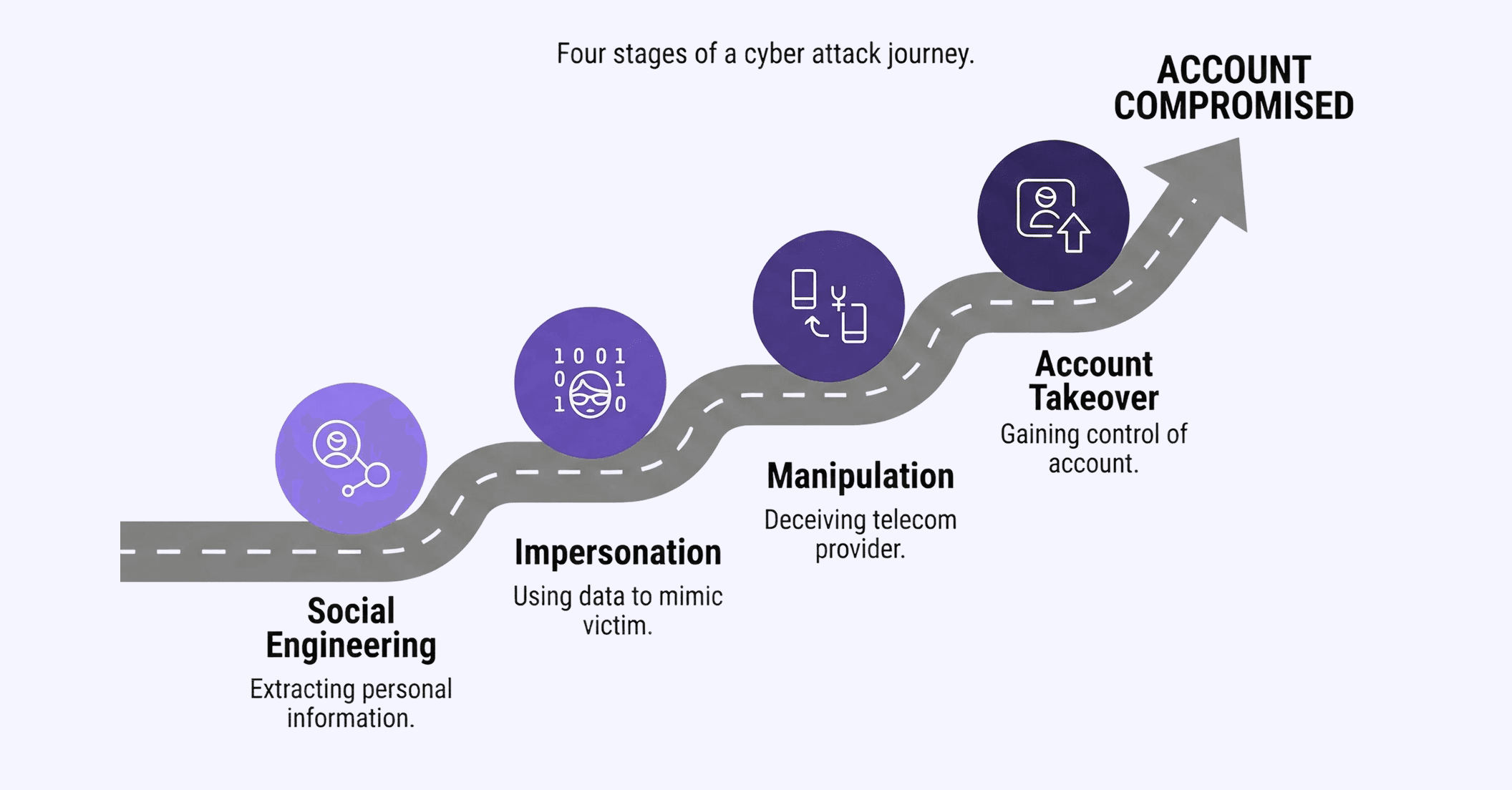

Authorized Push Payment (APP)

Reconnaissance: Identify targets via phishing, social media research, or compromised email threads.

Impersonation: Create convincing communications, such as fake invoices, spoofed bank emails, and voice calls that appear urgent and legitimate.

Redirect payment: Instruct the victim to transfer funds to an account controlled by the fraudster.

Rapid laundering: Move funds through multiple accounts, convert to crypto or cash, or withdraw via mule networks before detection.

Account Takeover (ATO)

Credential acquisition: Use credential stuffing, phishing, or SIM swap attacks to obtain login credentials.

Silent probing: Log in, change recovery details, and probe for saved payment instruments or loyalty balances without triggering alerts.

Monetization: Place orders using stored cards, request refunds to new accounts, or use account privileges to change shipping addresses.

Persistence and pivot: Establish backdoors, such as through changed MFA or alternate emails, for repeat abuse or to sell the account.

Refund and Chargeback

Initial purchase: Use stolen card or legitimate account to purchase goods, usually low-value, repeated transactions.

Claim dispute: Raise disputes shortly after delivery, citing non-delivery, unauthorized charges, or defective goods.

Exploit policies: Exploit lack of proof of delivery, merchant return windows, or lenient refund policies to secure refunds.

Repeat: Scale the scheme across accounts or engage mule buyers to mask repeat patterns.

Synthetic Identities

Assemble identity: Combine real user data with fabricated names, emails, or phone numbers.

Establish legitimacy: Open accounts, make small, timely, and low-risk payments to build credit or reputation.

Scale access: Leverage established credibility to access credit, BNPL, or higher-risk purchase channels.

Cash out: Default or withdraw credit lines, then disappear; or use accounts for ongoing transactional fraud.

Triangulation

Create storefront: Fraudsters list desirable items on a fake or temporary storefront at competitive prices.

Accept payment: A legitimate buyer pays the fake storefront using their own card.

Fulfill via stolen card: Fraudster purchases the same item from a legitimate merchant using stolen card details and ships it to the buyer.

Profit / evade: The fraudster pockets the buyer’s payment; when chargebacks occur, tracing the origin becomes difficult.

Payment Gateway and API

Identify weak endpoints: Scan for misconfigured gateways, outdated API keys, or exposed merchant credentials.

Exploit integration: Inject malicious payloads or reroute transactions through fake merchant accounts; perform automated test transactions.

Process fraudulent payouts: Use compromised gateway access to approve or route transactions that would otherwise be blocked.

Cover tracks: Rotate API keys, delete logs, or exploit limited observability in smaller PSPs.

SMS + Phishing (Smishing)

Spoof and send: Create convincing SMS messages or emails that mimic couriers, banks, or marketplaces.

Create urgency: Use delivery problems, payment confirmations, or security alerts to urge quick action.

Capture credentials: Direct victims to fake payment pages to capture card data, OTPs, or login credentials.

Exploit access: Immediately use harvested data for purchases or credential stuffing elsewhere.

Bot-driven Testing and Account Enumeration

Automate testing: Deploy bots and botnets to enumerate accounts, test credential combinations, or flood endpoints with authorization attempts.

Mimic humans: Use headless browsers, randomized mouse movements, and throttled timing to evade traditional bot detectors.

Harvest valid targets: Identify successfully authenticated accounts or valid card numbers for monetization.

Follow-on attacks: Pivot into ATO, CNP purchases, or credential stuffing across other merchants.

Existing fraud prevention methods and their limitations

As fraud grows more organized, so must the defenses against it. Across regions, eCommerce businesses are combining legacy tools, AI-based detection, and regulatory mandates to keep up with the speed of digital transactions. However, shaped by consumer behavior, payment infrastructure, and data protection laws, fraud prevention approaches differ in each market, as described below:

North America (United States and Canada)

Fraud prevention strategies, in the region, lean heavily on machine learning-based transaction scoring, behavioral analytics, and device fingerprinting integrated into payment gateways. Commonly used tools include real-time velocity checks, IP and device intelligence, BIN verification, and post-transaction chargeback monitoring. Major merchants and payment processors use 3D Secure 2.0 (3DS2) with a growing adoption of link analysis and graph-based intelligence to detect organized fraud rings and mule networks.

Europe (EU and the UK)

The European market is more compliance-driven. Under PSD2 and Strong Customer Authentication (SCA) mandates, multi-factor verification and dynamic linking are now baseline requirements with 3DS2. Biometric step-ups, EMV tokenization, and consortium data sharing through fraud intelligence networks are other tools used to fight Authorized Push Payment (APP) scams. There is growing reliance on risk-based authentication (RBA) to exempt low-risk transactions and preserve checkout speed.

Asia-Pacific (APAC)

Fraud detection in APAC reflects the diversity of markets, from mature ecosystems like Singapore and Australia to rapidly digitizing economies such as India, Indonesia, and the Philippines. Common fraud prevention tools include device intelligence, mobile app telemetry, and real-time transaction monitoring supported by national ID-linked KYC systems. Furthermore, eCommerce businesses in the region are investing in AI-driven behavioral analytics and cross-border fraud telemetry as payment rails expand through QR codes and instant transfers.

Middle East and North Africa (MENA)

In MENA, rapid fintech growth and digital wallet adoption have triggered both opportunity and vulnerability. The commonly used tools include regional payment gateways with built-in fraud scoring, geo-location validation, and OTP-based verification. Banks and merchants in the region are increasingly partnering with AI-native fraud orchestration platforms to manage multi-rail payments (cards, wallets, BNPL).

Latin America (LATAM)

Countries like Brazil, Mexico, and Colombia face high fraud volumes due to fast-growing digital payment adoption and uneven KYC enforcement. Businesses rely on real-time monitoring integrated with national instant payment systems like Pix (Brazil) and CoDi (Mexico), coupled with biometric verification. Collaborative fraud data exchanges are emerging in the region to help tackle organized cross-border attacks.

Telltales of payment fraud

Understanding telltales or subtle indicators of the fraud playbooks can help fraud teams initiate appropriate countermeasures before funds leave the merchant or customer accounts. These indicators include:

Payments and Orders: Several payment attempts from brand-new locations, many small test payments before one big purchase, billing and shipping addresses that don’t match, and heavy use of prepaid cards.

Bank Transfers: Sudden last-minute changes to where money should go, new bank accounts added, users acting strangely, urgent or secretive, money being routed to unknown countries.

Account Activity: New devices or IPs logging in, password resets in quick succession, changes to recovery settings, unexpected changes to delivery addresses.

Disputes and Deliveries: Many complaints from devices that look the same, delivery tracking that doesn’t match the truth, high dispute counts for certain products or customer groups.

Identity Checks: Personal details that don’t add up (such as a new email but an old credit history), new accounts seeking for big credits, the same device being used to create multiple "new" accounts.

Marketplace Sellers: Prices that are way too low, sellers with little or no history, multiple orders for the same item from different buyers and payment methods.

Merchant and API Activity: Unusual API activity patterns, new merchant accounts that look suspicious, mismatched financial records between payment systems and banks.

Customer Support Signals: Spike in helpdesk complaints about fake SMS links, customers reporting fake delivery messages, calls from people reporting unsolicited OTPs.

Login and Payment Attempts: Large bursts of fast, failed login or payment tries from the same IP areas, unusual browser and device details, repeated actions that look automated.

Techniques for more effective payment fraud prevention

Modern eCommerce fraud prevention requires precision on two counts: in blocking bad actors and instantly recognizing legitimate customers. This is made possible by connected intelligence. Businesses that unify identity, behavior, and transactional insights within adaptive AI frameworks can reduce losses, enhance trust, and deliver frictionless experiences globally, regardless of the payment rail or regulatory environment.

The key techniques and technologies reshaping payment fraud detection include:

Machine learning-driven risk scoring

Adaptive machine learning models continuously evaluate each transaction across variables, including device ID, geolocation, behavioral velocity, and purchase patterns, among others to assign a fraud risk score. Unlike static rules, these models evolve as fraud patterns shift, reducing both false positives and manual reviews. The emerging “human-in-the-loop” ML frameworks combine analyst feedback with automation for greater precision and explainability.

Behavioral Biometrics and Session Intelligence

Behavioral biometrics analyzes how users type, swipe, scroll, or move their cursor to determine whether it is a real customer or a bot behind the screen. Combined with session analytics, such as navigation paths and dwell time, it provides a strong behavioral signature that’s difficult for fraudsters to imitate.

Device Intelligence and Fingerprinting

Device fingerprinting identifies unique attributes of a customer’s device, such as browser version, OS type, screen resolution, IP patterns, and links them to known identities or prior risk events. This helps uncover hidden connections between seemingly unrelated transactions or accounts. Advanced persistent device identity graphs can track risk across multiple sessions and payment methods.

Identity Graphs and Entity Linking

An identity graph consolidates data from multiple touchpoints, namely: payments, logins, devices, and delivery addresses, to reveal how entities (users, accounts, cards, devices) interact. Graph intelligence helps identify synthetic identities, mule networks, coordinated fraud rings, and collusion patterns invisible to linear models, in near real time.

Consortium and Shared Intelligence Networks

Because no single business can detect all fraud alone, businesses are collaborating through shared fraud networks and consortium data models. These systems anonymize data while surfacing shared risk indicators across merchants, acquirers, and payment processors, while also providing visibility into and learning from attacks seen elsewhere, improving accuracy for everyone.

Risk-Based Authentication (RBA)

Instead of enforcing the same level of friction for every transaction, RBA dynamically adjusts authentication based on contextual risk, stepping up only when anomalies are detected. Common tools include 3DS2, biometric authentication, and adaptive step-up logic based on user history. This approach optimizes user experience while maintaining compliance with PSD2, SCA, and similar mandates.

Real-time Orchestration Platforms

Fraud prevention no longer happens in silos. Modern orchestration platforms integrate identity verification, behavioral analysis, and payment decisioning under a single layer, enabling businesses to route each transaction through the right risk checks instantly. This provides businesses with a unified view of the customer journey and supports real-time decisioning across multiple fraud tools and data sources.

Explainable AI (XAI) and Transparent Decisioning

Enhances model transparency by showing why a transaction was flagged or cleared. This not only helps in compliance audits but also builds trust between merchants, regulators, and customers.

Generative AI for Synthetic Fraud Detection

Countering fraud driven by generative AI, deepfake identities and synthetic profiles, requires AI systems that can detect anomalies in text, imagery, and document consistency, such as mismatched metadata or linguistic fingerprints.

Continuous Identity Verification and Lifecycle Monitoring

Fraud prevention is no longer a one-time KYC event. Continuous identity monitoring tracks signals throughout the customer lifecycle, from onboarding to checkout to refund, ensuring that the user remains genuine at every step.

Regulatory and other challenges

The intersection of technology, law, and human behavior, being used to manage payment fraud defense, is disorganized. As a result, even the most advanced detection systems struggle to deliver consistent outcomes across jurisdictions and infrastructures. This complexity arises not just from fraud itself. It is a combination of varied regulations, legacy technology, adversarial AI, and structural bottlenecks that slow down detection and decisioning, as described below:

Regulatory Complexity and Fragmentation

Rules on authentication, data protection, liability, and consumer rights, differ by region.For instance, PSD2/SCA in Europe, reimbursement frameworks for APP fraud in the UK, and emerging payment data regulations across APAC and MENA, make unified global fraud strategies difficult. This is because authentication methods that comply in one region may increase friction in another.

Data Privacy, Consent, and Residency Constraints

The most valuable fraud indicators, namely: device telemetry, behavioral signals, and cross-merchant data, are often restricted by privacy laws or residency mandates. This causes the data that could otherwise reveal synthetic identities or coordinated attacks, to remain fragmented across systems and borders, limiting the precision of real-time risk assessments.

Legacy Fraud Systems and Siloed Data

A patchwork of legacy rule engines, manual review teams, and standalone tools that don’t communicate with one another can create operational blind spots, inconsistent risk scoring, and an inability to detect cross-channel fraud patterns. Data silos also prevent timely model retraining and unified case management.

The AI Arms Race and Adversarial Techniques

AI is a double-edged sword. It can transform both defense and offense. Using machine learning, fraudsters can mimic legitimate shopper behavior, automate credential testing, and generate synthetic identities or documents. On the other hand, many businesses continue to use black-box AI models that are not only difficult to interpret or audit, but also create compliance and governance challenges.

Cross-border Reconciliation, Currency and Liability Issues

Global eCommerce works on a complex network of acquirers, issuers, and gateways that operate under different rules. Diverse chargeback procedures, multi-currency settlement delays, instant payment systems, and conflicting liability clauses can make funds recovery or determining accountability in cross-border fraud cases challenging.

Operational Bottlenecks: Talent, Tools and Processes

Manual investigations are prone to human errors. Overworked review teams increase response times. This can be especially challenging for smaller organizations that may lack dedicated fraud operations. Furthermore, shortage of skilled fraud analysts, data scientists, and risk engineers may make businesses vulnerable.

False Positives, CX Friction and Revenue Tradeoffs

Excessive controls add authentication hoops that may help stop fraud but end up frustrating customers. False declines, repetitive authentication, and rigid rule thresholds can lead to cart abandonment and long-term churn. This inability to balance friction and user experience remains a major source of lost revenue and competitive disadvantage.

Technology Scalability and Cost

Advanced fraud detection, including real-time orchestration, persistent device tracking, and graph analytics requires significant infrastructure and compute resources. For many merchants, these costs may be prohibitive, leading to gaps in protection against evolving fraud tactics.

Relevant Data Types for Payment Fraud Detection

Isolated data points can only tell incomplete stories. When layered and correlated, these signals can expose the hidden structure of payment fraud. In eCommerce, fraudsters constantly manipulate identity, devices, and payment vectors. Therefore, modern fraud detection systems must move from rule-based checks to network-informed intelligence to reveal how entities relate, not just what they do. Important data types that can make this happen include:

Data Type | Key Indicators | Helps Detect | Regional Relevance |

|---|---|---|---|

Identity Data | Mismatched billing or shipping addresses, newly created emails, unverifiable IDs | Synthetic identity fraud, account opening fraud | High in the US, UK, and India, where synthetic IDs and fake KYC are rising. |

Device and Network Data | Proxy/VPN use, device fingerprint mismatch, rapid location change | Account takeover, bot-driven card testing, payment gateway fraud | Critical in SEA and LATAM where shared or low-cost devices are common |

Behavioral Data | Unnatural typing speed, repetitive navigation, erratic session timing | Bot attacks, credential stuffing, fake account creation | Major concern in mature eCommerce markets like U.S. and Australia |

Transactional Data | Sudden spending spikes, unusual payment method use, high refund ratios | Chargeback fraud, triangulation fraud, APP scams | Common in the UK (APP scams) and India (BNPL/wallet exploitation) |

Alternate/Consortium Data | Reused phone numbers, shared device IDs across merchants | Cross-platform mule networks, repeat offenders | Expanding use in Australia and Singapore with data-sharing mandates |

Graph and Relationship Data | Clusters of linked accounts, shared payment credentials | Coordinated fraud rings, merchant collusion, social-engineered networks | Effective across cross-border eCommerce and marketplace ecosystems |

Key Takeaways

Payment fraud is evolving faster than traditional defenses can adapt.

Fraud types differ by region, demanding localized detection strategies.

Correlating identity, device, behavioral, and transactional data is crucial for early detection.

Legacy systems and compliance silos leave critical fraud blind spots.

AI and graph intelligence enable accurate, low-friction fraud prevention.

Fight payment fraud with Bureau

Fighting payment fraud today demands more than just detection. It requires intelligence, interoperability, and compliance by design. Bureau’s unified risk decisioning platform empowers eCommerce businesses, payment providers, and marketplaces to detect, prevent, and respond to complex payment fraud while meeting regional data protection and regulatory mandates.

Bureau’s intelligence-driven, regulation-aware platform helps global eCommerce players detect payment fraud in real time. It enables eCommerce platforms to adapt to regional nuances, including as GDPR (Europe), CCPA (US), PDPA (Singapore), and DPDP (India). With modular APIs and low-latency decision engine, Bureau bridges the divide between trust and compliance. This helps eCommerce platforms ensure customer experiences stay frictionless, secure, and compliant, regardless of where they operate.

Learn how Bureau empowers businesses to scale across new markets and payment methods without rewriting compliance or risk frameworks. Book a free demo now.