5 Key Takeaways From GFF 2025 Shaping India's Fintech Future

5 Key Takeaways From GFF 2025 Shaping India's Fintech Future

5 Key Takeaways From GFF 2025 Shaping India's Fintech Future

With smarter payments, inclusive credit, contextual fraud detection, collaborative defenses, and trust-driven innovation, the Global Fintech Festival 2025.

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

The Global Fintech Festival (GFF) 2025, held from 7-9 October in Mumbai, reaffirmed India’s status as the world’s fintech powerhouse. The event, themed, Empowering Finance for a Better World, Powered by AI, brought together over 100,000 participants, 850 speakers, and 7,500+ companies, and underscored how India is shaping global finance through technology, trust, and inclusion.

India now accounts for over 50% of the world’s real-time digital transactions, led by the success of UPI (Unified Payments Interface). Alongside Aadhaar, DigiLocker, ONDC, and the Digital Public Infrastructure (DPI), India has created a global blueprint for inclusive, secure, and scalable financial systems. Further, with the launch of a foreign-currency settlement system via GIFT City, India now aims to become a global fintech hub. In his keynote, Prime Minister Narendra Modi highlighted that India has democratized technology and is now ready to share it with the world.

Here are the top five takeaways from GFF 2025.

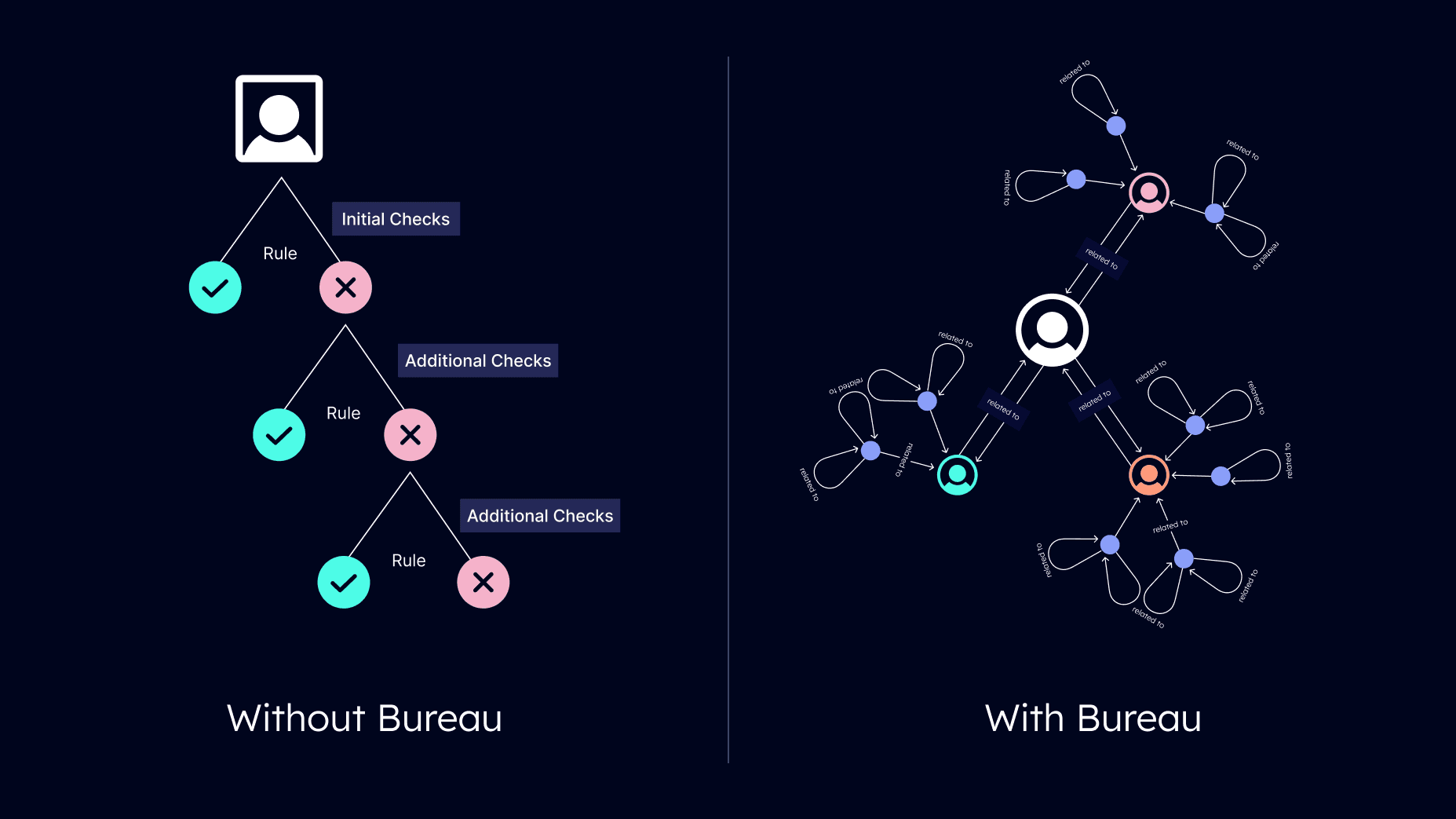

Move beyond static identity checks to contextual verification:

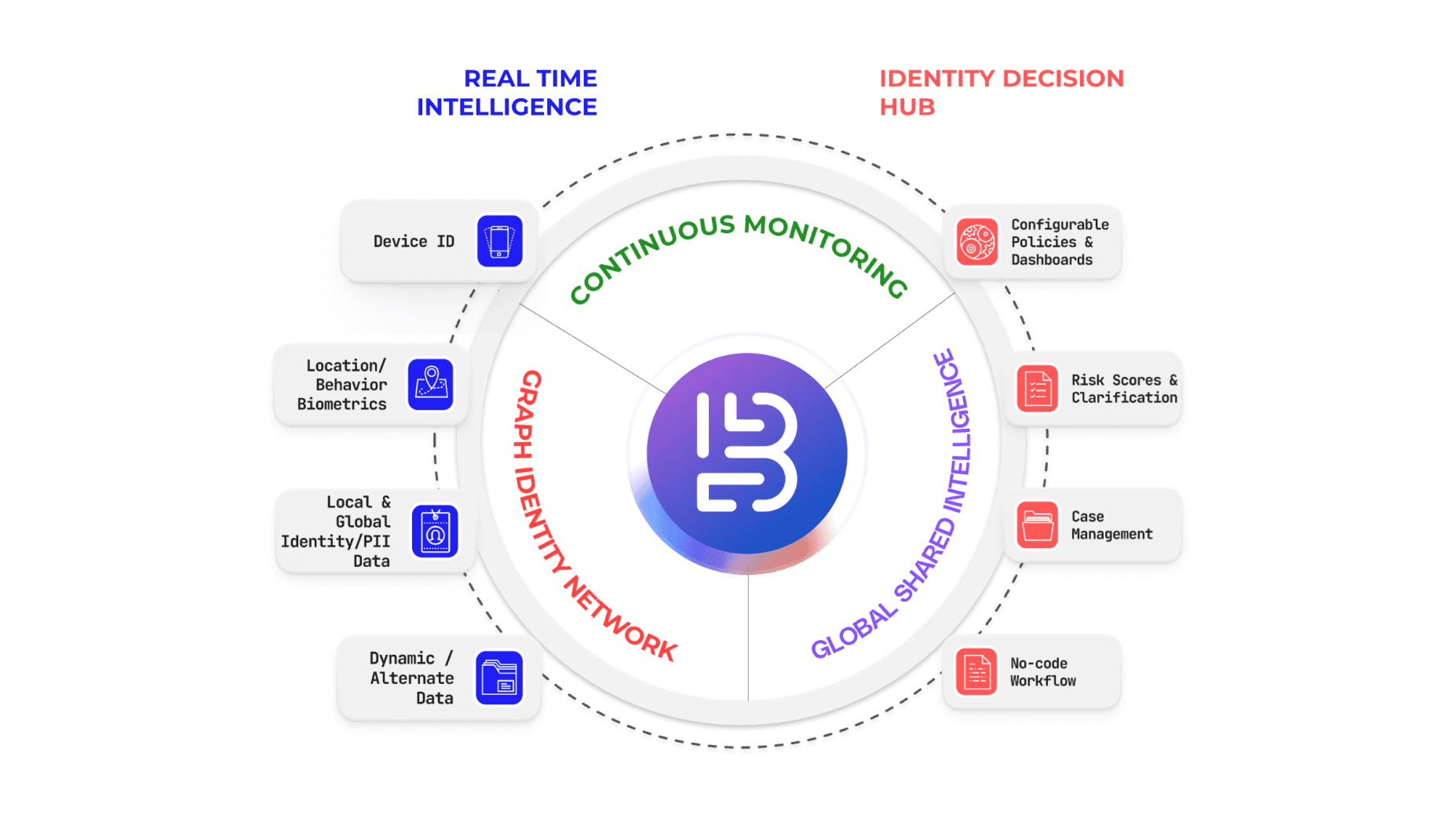

Digital fraud, increasingly powered by generative AI, deepfakes, and synthetic identities, is a big challenge to solve. There’s a need for a new frontline against networked fraud and mule activity, threats that are evolving faster than traditional defense mechanisms can keep pace with. Advanced behavioral analytics, alternate data, and graph intelligence are the new standard for real-time risk decisioning. Graph-based solutions, such as Bureau’s Graph Identity Network (GIN), that connect behavioral and identity data can help reveal collusive rings and synthetic identities, which static rule-based verifications often miss. By enabling fintechs to analyze how users connect and not just who they are, graph intelligence can help detect coordinated fraud early and safeguard the ecosystem.

Innovations in payments must balance convenience with fraud prevention:

The next phase of payments isn’t just about access, it’s about accountability. Therefore, innovations in digital payments must help build fraud-resistant, sustainable systems that strengthen user trust and merchant confidence. At the GFF2025, the RBI announced a new suite of innovations including AI-powered UPI HELP, IoT-based payments, and biometric authentication to make payments smarter and safer. With growing volumes of real-time payments, chargebacks and fraudulent disputes will also surge. Fintechs must, therefore, integrate behavioral analytics, device fingerprinting, and network intelligence into their payment flows to distinguish genuine customers from bots or synthetic IDs and reduce revenue leakage without compromising experience.

Inclusion is a growth engine:

Financial inclusion was a key theme at the GFF2025 with an emphasis on evolving from policy ambition to practical execution. Vernacular interfaces, micro-lending for gig workers, and digital insurance for rural consumers are now mainstream solutions. Powered by the responsible use of data, financial inclusion can drive both social equity and sustainable growth to unlock the next billion digital transactions.

Collaboration is key to fighting modern fraud:

Fraudsters are weaponizing AI, deepfakes, and automation to execute networked fraud. These modern fraud tactics are evolving too fast for individual or isolated defense. Therefore, there is an urgent need for data silos to dissolve into shared risk ecosystems and collaborative intelligence-sharing frameworks that can support collective defense against next-gen fraud.

Trust, ethics, and compliance will define fintech’s next competitive edge:

As the industry matures, trust becomes its most valuable currency. With AI-driven decisioning becoming ubiquitous, ethical AI and regulatory compliance will become critical, calling for explainable, fair, and auditable AI models. This will create greater transparency and traceability, strengthening the integrity of the entire ecosystem.

Fintech’s next chapter

The Global Fintech Festival 2025 underscored that India is shaping the future of global fintech. And this future will favor businesses that build resilient, inclusive, and trustworthy ecosystems. As volumes of digital transactions grow, advanced solutions and collaborative platforms will be needed to share threat intelligence and fight co-ordinated fraud in real time.

Bureau exemplifies this vision by enabling responsible financial inclusion and credit expansion without increasing risk. Its alternate data and AI-driven credit modeling adds behavioral and contextual layers to identity data, empowering fintechs to evaluate and serve genuine thin-file and underserved consumers.

Bureau’s unified risk decisioning platform adopts the ‘trust-by-design’ approach to help businesses scale up responsibly and build trust through transparent AI governance, explainable models, continuous bias testing, and compliance with RBI, BSP, and GDPR-equivalent frameworks. To learn how Bureau supports cross-platform collaboration to fight networked fraud, talk to an expert now.

The Global Fintech Festival (GFF) 2025, held from 7-9 October in Mumbai, reaffirmed India’s status as the world’s fintech powerhouse. The event, themed, Empowering Finance for a Better World, Powered by AI, brought together over 100,000 participants, 850 speakers, and 7,500+ companies, and underscored how India is shaping global finance through technology, trust, and inclusion.

India now accounts for over 50% of the world’s real-time digital transactions, led by the success of UPI (Unified Payments Interface). Alongside Aadhaar, DigiLocker, ONDC, and the Digital Public Infrastructure (DPI), India has created a global blueprint for inclusive, secure, and scalable financial systems. Further, with the launch of a foreign-currency settlement system via GIFT City, India now aims to become a global fintech hub. In his keynote, Prime Minister Narendra Modi highlighted that India has democratized technology and is now ready to share it with the world.

Here are the top five takeaways from GFF 2025.

Move beyond static identity checks to contextual verification:

Digital fraud, increasingly powered by generative AI, deepfakes, and synthetic identities, is a big challenge to solve. There’s a need for a new frontline against networked fraud and mule activity, threats that are evolving faster than traditional defense mechanisms can keep pace with. Advanced behavioral analytics, alternate data, and graph intelligence are the new standard for real-time risk decisioning. Graph-based solutions, such as Bureau’s Graph Identity Network (GIN), that connect behavioral and identity data can help reveal collusive rings and synthetic identities, which static rule-based verifications often miss. By enabling fintechs to analyze how users connect and not just who they are, graph intelligence can help detect coordinated fraud early and safeguard the ecosystem.

Innovations in payments must balance convenience with fraud prevention:

The next phase of payments isn’t just about access, it’s about accountability. Therefore, innovations in digital payments must help build fraud-resistant, sustainable systems that strengthen user trust and merchant confidence. At the GFF2025, the RBI announced a new suite of innovations including AI-powered UPI HELP, IoT-based payments, and biometric authentication to make payments smarter and safer. With growing volumes of real-time payments, chargebacks and fraudulent disputes will also surge. Fintechs must, therefore, integrate behavioral analytics, device fingerprinting, and network intelligence into their payment flows to distinguish genuine customers from bots or synthetic IDs and reduce revenue leakage without compromising experience.

Inclusion is a growth engine:

Financial inclusion was a key theme at the GFF2025 with an emphasis on evolving from policy ambition to practical execution. Vernacular interfaces, micro-lending for gig workers, and digital insurance for rural consumers are now mainstream solutions. Powered by the responsible use of data, financial inclusion can drive both social equity and sustainable growth to unlock the next billion digital transactions.

Collaboration is key to fighting modern fraud:

Fraudsters are weaponizing AI, deepfakes, and automation to execute networked fraud. These modern fraud tactics are evolving too fast for individual or isolated defense. Therefore, there is an urgent need for data silos to dissolve into shared risk ecosystems and collaborative intelligence-sharing frameworks that can support collective defense against next-gen fraud.

Trust, ethics, and compliance will define fintech’s next competitive edge:

As the industry matures, trust becomes its most valuable currency. With AI-driven decisioning becoming ubiquitous, ethical AI and regulatory compliance will become critical, calling for explainable, fair, and auditable AI models. This will create greater transparency and traceability, strengthening the integrity of the entire ecosystem.

Fintech’s next chapter

The Global Fintech Festival 2025 underscored that India is shaping the future of global fintech. And this future will favor businesses that build resilient, inclusive, and trustworthy ecosystems. As volumes of digital transactions grow, advanced solutions and collaborative platforms will be needed to share threat intelligence and fight co-ordinated fraud in real time.

Bureau exemplifies this vision by enabling responsible financial inclusion and credit expansion without increasing risk. Its alternate data and AI-driven credit modeling adds behavioral and contextual layers to identity data, empowering fintechs to evaluate and serve genuine thin-file and underserved consumers.

Bureau’s unified risk decisioning platform adopts the ‘trust-by-design’ approach to help businesses scale up responsibly and build trust through transparent AI governance, explainable models, continuous bias testing, and compliance with RBI, BSP, and GDPR-equivalent frameworks. To learn how Bureau supports cross-platform collaboration to fight networked fraud, talk to an expert now.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.