Refund Abuse Tactics and How Businesses Can Stop Them

Refund Abuse Tactics and How Businesses Can Stop Them

Refund Abuse Tactics and How Businesses Can Stop Them

Understand refund fraud, return fraud vs refund fraud, common abuse tactics, and how device intelligence helps prevent repeat refund losses.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

A refund request can look like good customer service until the same pattern starts draining margins.

Refund fraud happens when someone manipulates a business into issuing money, credit, replacements, reimbursements, or chargebacks they are not entitled to.

It may be as simple as a customer claiming a delivered order never arrived, receiving a refund, and keeping the product. Multiply that across accounts, devices, payment methods, or support channels, and a policy built for trust becomes a repeat-loss channel.

This guide explores how refund fraud works, how it differs from return fraud, the most common tactics, warning signs, and practical ways to reduce abuse without hurting loyal customers.

What Is Refund Fraud?

Refund fraud is when someone manipulates a business into issuing a refund, replacement, reimbursement, chargeback, store credit, or gift card to which they are not entitled.

Refund fraud can happen across several customer touchpoints:

Online, through eCommerce orders, delivery claims, digital products, or subscription cancellations

In-store, through fake receipts, product swaps, or misrepresented returns

Through customer support, when agents are pressured to approve refunds quickly

Through payment providers, when a buyer disputes a legitimate transaction

Through card issuers, when a refund request turns into a chargeback claim

The cost can add up quickly. Appriss Retail and Deloitte’s 2024 report found that fraudulent returns and claims cost retailers $103 billion in 2024, with 15.14% of all returns deemed fraudulent.

The tricky part is that not every refund request is suspicious. Customers may have real delivery issues, damaged products, billing errors, or service complaints.

Refund fraud prevention starts by spotting repeated patterns and intent, rather than treating every unhappy customer like a fraud risk.

Refund Fraud vs Return Fraud

Refund fraud and return fraud are closely related, but they are not the same. The simplest way to separate them is this: refund fraud focuses on the outcome, while return fraud focuses on the product return process.

Refund Fraud | Return Fraud |

Refund fraud is a broader category where someone manipulates a business into issuing a refund, credit, reimbursement, or replacement to which they are not entitled. | Return fraud is a type of refund fraud where the product return process is manipulated. |

It can happen with physical products, digital goods, subscriptions, deliveries, services, or payment disputes. | It usually involves physical goods being returned, swapped, damaged, used, or misrepresented. |

Example: A customer falsely claims an order never arrived and receives a refund while keeping the product. | Example: A customer returns a counterfeit or older item instead of the original product purchased. |

All return fraud is refund fraud, but not all refund fraud involves a product return.

That distinction matters because refund abuse often starts before anything is returned, and in many cases, there may be no return involved at all.

How Does Refund Fraud Happen?

Refund fraud usually happens when fraudsters find a weak spot in a refund policy or operational workflow, submit a claim that sounds believable, and receive money, credit, or a replacement before the business can verify the full context.

Fraudsters identify a refund policy gap: They look for lenient refund windows, instant refund approvals, weak receipt checks, limited proof-of-delivery review, or refunds issued before returned items are inspected.

They place, fake, or manipulate an order: Some make a real purchase with the intent to refund it later. Others use stolen cards, alter receipts, create fake order confirmations, or spread activity across multiple accounts.

They submit a false refund claim: Common claims include “item not received,” “wrong item delivered,” “product arrived damaged,” “refund not received,” “duplicate charge,” or “unauthorized transaction.”

The business issues the refund: Support teams may approve the request quickly to protect customer experience, especially when delivery, payment, account, and support data sit in separate systems.

The pattern repeats across accounts or channels: Fraudsters may rotate accounts, devices, payment methods, addresses, stores, or support channels to avoid detection.

Once these gaps are understood, the next step is to look at the specific tactics fraudsters use to turn normal refund workflows into repeat abuse channels.

Related Read: How Businesses Detect and Prevent Payment Fraud

What Are the Most Common Refund Fraud Tactics?

Refund fraud usually follows a few repeatable patterns. The details vary by industry, but most tactics exploit the same gaps: weak proof checks, fast refund approvals, disconnected systems, or limited visibility across accounts.

1. False Item-Not-Received Claims

Fraudsters claim an order never arrived, even when it was delivered. This is common in eCommerce, food delivery, marketplaces, and logistics-heavy businesses where support teams may not have enough delivery evidence in one place.

For example, a buyer receives a high-value item, tells support that the package never arrived, and gets a refund or replacement before the business verifies proof of delivery.

These claims often target products that are expensive, easy to resell, or shipped through low-verification delivery flows.

2. Wardrobing or Use-and-Return Abuse

Wardrobing happens when someone buys an item, uses it temporarily, and returns it as unused. It is common with fashion, electronics, luxury products, home goods, event purchases, and seasonal items.

Even when the item comes back, the business still loses value. The product may be damaged, opened, out of season, missing packaging, or no longer sellable at full price.

3. Receipt Fraud and Fake Proof

Fraudsters may use fake, altered, stolen, or discarded receipts to claim refunds they do not qualify for. In online flows, they may submit:

Edited screenshots

Fake order emails

Manipulated delivery images

Forged proof of purchase

As AI-generated images and documents become easier to create, high-value refund claims need stronger proof validation. In some cases, businesses may need identity document verification to confirm customer identity, ownership, or supporting evidence before approving refunds.

4. Product Swap and Bricking Fraud

In product swap fraud, a customer buys a genuine item and returns a counterfeit, older, cheaper, damaged, or incomplete version instead. This is especially risky for high-value goods with serial numbers, branded packaging, or resale value.

The loss also extends beyond the refund itself. LiquiDonate’s 2026 Returns Fraud Report found that retailers estimate 15% of all returns are fraudulent, while each return can cost $25 to $30 in shipping, processing, and handling.

Bricking is a common tactic in electronics where a fraudster may remove valuable components, damage the product, or return a non-working item while claiming it arrived defective.

5. Duplicate Refund and Chargeback-Linked Fraud

Some customers request a merchant refund and then file a card chargeback for the same transaction. Others claim the refund was never received and push customer support for a second refund.

This creates a double-loss problem. The business may lose the refunded amount, the product or service value, and additional dispute fees tied to the chargeback.

The MRC’s 2026 Global eCommerce Payments and Fraud Report found that 62% of merchants reported an increase in first-party misuse disputes, while 57% saw refund and policy abuse rise over the past year.

6. Multi-Account Refund Abuse and Refund Rings

Fraudsters often create multiple accounts to bypass refund limits or avoid detection after earlier abuse. They may rotate information to appear like different customers, such as:

Phone numbers

Emails

Delivery addresses

IP (Internet Protocol) addresses

Payment methods

Devices

Organized refund rings can scale this through online communities, Telegram channels, scripts, or “refunding services.” This is where linked signals matter.

What Are the Warning Signs of Refund Fraud and Refund Abuse?

Refund fraud is easier to catch when teams stop reviewing claims one by one and start looking for unusual patterns across accounts, payments, devices, support activity, and refund outcomes.

Key warning signs include:

Refund frequency is higher than the customer’s purchase history supports

Multiple accounts share the same device, address, phone number, payment method, or behavioral pattern

Refund requests come from new accounts with limited order history

Refund-heavy customers contact support through multiple channels to get a different outcome

Refunds are requested to a different payment method, wallet, gift card, or store credit

A denied refund is followed by a payment dispute or chargeback

Return tracking does not match delivery, pickup, carrier, or warehouse data

The same support agent approves an unusually high number of exceptions

Several accounts show similar refund timing, language, navigation behavior, or escalation patterns

None of these signals proves fraud alone, but the risk becomes clearer when they cluster. For example, a new account requesting a refund is not automatically suspicious. But if that account shares a device with several refund-heavy users, uses a different refund method, and shows scripted support behavior, it deserves closer review.

This is where behavioral biometrics can add context by identifying bot-like activity, scripted sessions, fraud farm behavior, and unusual interaction patterns behind refund requests.

How Can Device Intelligence Help Prevent Online Refund Fraud?

Device intelligence helps teams look beyond the account making the refund request and identify the device and session behind it. This makes it easier to detect repeat refund abusers, refund rings, suspicious device behavior, and high-risk refund patterns before approving refunds or replacements.

Step 1: Identify Repeat Refund Abusers Across New Accounts

Fraudsters often create new accounts after reaching refund limits or getting flagged for earlier abuse. Device intelligence helps connect these accounts when they originate from the same or related devices. This can reveal patterns such as:

A user creating new accounts after refund limits are reached

Multiple accounts requesting refunds for similar products or reasons

Different identities showing the same device, browser, app, or behavioral signals

A refund-heavy customer repeatedly changing email IDs, phone numbers, or names

With Bureau ID's Device ID, businesses can recognize repeat users even when account-level details keep changing.

Step 2: Detect Device Resets, Spoofing, Emulators, and VPN Use

Refund fraudsters may try to hide behind device resets, incognito browsing, VPNs, proxies, emulators, or spoofed app environments. Device intelligence can flag these signals during refund requests, especially when the claim is high-value or unusual.

Useful signals include:

Device reset before account creation or refund request

VPN, proxy, TOR, or location masking signals

Emulator or virtual device usage

Spoofed app, browser, or SDK signals

Device changes after delivery or right before a refund claim

These signals do not prove fraud on their own, but when they appear alongside refund history, order value, delivery evidence, and payment behavior, they can help teams separate normal customer issues from risky claims.

Step 3: Link Refund Requests to Devices, Accounts, Payments, and Addresses

Device intelligence becomes more useful when it is connected with account, payment, delivery, and transaction data.

Instead of asking, “Does this refund request look valid?”, teams can ask, “Where else have we seen this device, account, address, payment method, or behavior before?”

Bureau ID’s Graph Identity Network can help connect accounts, devices, behaviors, and identities that may look unrelated in isolation, making coordinated refund abuse easier to detect.

Step 4: Score Risky Refund Requests Before Approval

Device intelligence can help create a risk score before money, store credit, or a replacement is issued.

A risk score helps teams decide what should happen next: approve the refund instantly, request more evidence, route the case to fraud review, delay release until inspection, or restrict the refund method. This keeps low-risk refunds fast while giving fraud teams more control over claims that carry higher loss potential.

Step 5: Add Friction Only for High-Risk Refund Claims

The goal is not to make refunds harder for everyone. The goal is to keep refunds fast for genuine customers while applying extra checks only when risk signals appear.

Selective friction can include:

Asking for additional delivery proof only for high-risk claims

Triggering identity or ownership verification for high-value refund requests

Holding refund approval until returned items are inspected

Routing suspicious refund requests to fraud review

Limiting refund methods when device and payment signals do not match

This approach protects revenue without turning every refund into a poor customer experience.

Related Read: How to Detect First-Party Fraud Before Losses Escalate

Device Intelligence Checklist for Refund Fraud PreventionUse this checklist to assess whether your refund fraud prevention process can detect repeat abuse without slowing down genuine customers:

|

How Can Businesses Detect Refund Fraud With Bureau ID?

Bureau ID helps businesses detect refund fraud by acting as a unified risk decisioning layer across user touchpoints. It combines device, identity, behavior, network, and transaction signals to give teams more context before approving refunds, replacements, credits, or chargeback-linked claims.

That helps businesses:

Detect repeat refund abusers even when they create new accounts

Identify linked accounts, shared devices, suspicious behaviors, and refund rings

Score risky refund or chargeback behavior before loss occurs

Apply extra checks only when the risk is high

Keep genuine refunds fast and low-friction

The aim is to understand whether the request fits the customer’s normal behavior, account history, device pattern, payment activity, and connected network before a decision is made.

The impact of this approach becomes clearer when we look at how it works in practice.

Case Study: How a Leading PropTech Saved $1.25M in Chargeback Fraud With Bureau ID

Refund fraud and chargeback fraud often overlap when customers or fraudsters use payment disputes to reverse legitimate transactions. A leading PropTech platform was losing revenue because credit card rent payments created an opportunity for fake chargebacks, with 20% of such payments resulting in disputes.

What Bureau ID implemented:

Used alternate data to strengthen risk assessment

Built custom risk models tailored to chargeback behavior

Enabled real-time decisioning to evaluate users and transactions before payment completion

Results achieved:

Prevented $1.25M in chargeback fraud in three months

Reduced false chargeback rates from 40% to 8%

Stopped 1,200+ high-risk transactions before payment

Flagged 60,000+ users as high-risk for chargeback fraud

Restricted credit card payments for risky users

Read the full case study here → A Leading PropTech Saves $1.25M in Chargeback Fraud

Refund fraud prevention works best when businesses can see the full pattern behind the claim. A single refund request may look harmless, but connected risk signals can reveal whether it is part of a larger abuse cycle.

Protect Your Revenue From Refund Fraud

Refund fraud often looks like a frustrated customer, a missing package, a refund delay, or a one-time exception that support approves to keep the experience smooth.

Bureau ID connects device, identity, behavior, network, and transaction signals so teams can see whether a refund request fits normal customer behavior or points to repeat abuse. This helps businesses detect:

Linked accounts

Refund rings

Risky claims

Repeated refund requests

Frequent claims

If refund abuse is becoming harder to separate from genuine customer issues, it may be time to review where your current workflows are missing context. Schedule a demo with Bureau ID to see how unified risk decisioning can help protect revenue without slowing down trusted customers.

FAQs

1. What is refund fraud?

Refund fraud is when someone manipulates a business into issuing a refund, replacement, store credit, chargeback, or reimbursement to which they are not entitled. It can happen through false claims, fake proof, product swaps, duplicate refunds, or repeated refund abuse.

2. What are common examples of refund fraud?

Common refund fraud examples include false item-not-received claims, wardrobing, fake receipts, empty box scams, product swaps, bricking, duplicate refund requests, and chargeback-linked fraud. These tactics exploit gaps in refund policies, delivery checks, payment workflows, or customer support processes.

3. What is the difference between return fraud and refund fraud?

Return fraud is a type of refund fraud that involves manipulating the product return process. Refund fraud is broader and can involve returns, chargebacks, digital products, subscriptions, delivery claims, store credits, or reimbursements where no physical return happens.

4. How can businesses prevent refund fraud?

Businesses can prevent refund fraud by using clear refund policies, purchase matching, delivery verification, return inspection, chargeback monitoring, support training, device intelligence, and risk-based decisioning. The goal is to review risky claims without making refunds harder for genuine customers.

5. What are signs of refund abuse?

Signs of refund abuse include unusually high refund frequency, multiple accounts sharing the same device or payment method, refund requests from new accounts, repeated support escalations, refund requests to different payment methods, and chargebacks after denied refund claims.

6. How does device intelligence help with refund fraud prevention?

Device intelligence helps businesses identify the device and session behind a refund request. This makes it easier to detect repeat refund abusers, linked accounts, suspicious device behavior, VPN or emulator use, and refund rings even when fraudsters change visible account details.

A refund request can look like good customer service until the same pattern starts draining margins.

Refund fraud happens when someone manipulates a business into issuing money, credit, replacements, reimbursements, or chargebacks they are not entitled to.

It may be as simple as a customer claiming a delivered order never arrived, receiving a refund, and keeping the product. Multiply that across accounts, devices, payment methods, or support channels, and a policy built for trust becomes a repeat-loss channel.

This guide explores how refund fraud works, how it differs from return fraud, the most common tactics, warning signs, and practical ways to reduce abuse without hurting loyal customers.

What Is Refund Fraud?

Refund fraud is when someone manipulates a business into issuing a refund, replacement, reimbursement, chargeback, store credit, or gift card to which they are not entitled.

Refund fraud can happen across several customer touchpoints:

Online, through eCommerce orders, delivery claims, digital products, or subscription cancellations

In-store, through fake receipts, product swaps, or misrepresented returns

Through customer support, when agents are pressured to approve refunds quickly

Through payment providers, when a buyer disputes a legitimate transaction

Through card issuers, when a refund request turns into a chargeback claim

The cost can add up quickly. Appriss Retail and Deloitte’s 2024 report found that fraudulent returns and claims cost retailers $103 billion in 2024, with 15.14% of all returns deemed fraudulent.

The tricky part is that not every refund request is suspicious. Customers may have real delivery issues, damaged products, billing errors, or service complaints.

Refund fraud prevention starts by spotting repeated patterns and intent, rather than treating every unhappy customer like a fraud risk.

Refund Fraud vs Return Fraud

Refund fraud and return fraud are closely related, but they are not the same. The simplest way to separate them is this: refund fraud focuses on the outcome, while return fraud focuses on the product return process.

Refund Fraud | Return Fraud |

Refund fraud is a broader category where someone manipulates a business into issuing a refund, credit, reimbursement, or replacement to which they are not entitled. | Return fraud is a type of refund fraud where the product return process is manipulated. |

It can happen with physical products, digital goods, subscriptions, deliveries, services, or payment disputes. | It usually involves physical goods being returned, swapped, damaged, used, or misrepresented. |

Example: A customer falsely claims an order never arrived and receives a refund while keeping the product. | Example: A customer returns a counterfeit or older item instead of the original product purchased. |

All return fraud is refund fraud, but not all refund fraud involves a product return.

That distinction matters because refund abuse often starts before anything is returned, and in many cases, there may be no return involved at all.

How Does Refund Fraud Happen?

Refund fraud usually happens when fraudsters find a weak spot in a refund policy or operational workflow, submit a claim that sounds believable, and receive money, credit, or a replacement before the business can verify the full context.

Fraudsters identify a refund policy gap: They look for lenient refund windows, instant refund approvals, weak receipt checks, limited proof-of-delivery review, or refunds issued before returned items are inspected.

They place, fake, or manipulate an order: Some make a real purchase with the intent to refund it later. Others use stolen cards, alter receipts, create fake order confirmations, or spread activity across multiple accounts.

They submit a false refund claim: Common claims include “item not received,” “wrong item delivered,” “product arrived damaged,” “refund not received,” “duplicate charge,” or “unauthorized transaction.”

The business issues the refund: Support teams may approve the request quickly to protect customer experience, especially when delivery, payment, account, and support data sit in separate systems.

The pattern repeats across accounts or channels: Fraudsters may rotate accounts, devices, payment methods, addresses, stores, or support channels to avoid detection.

Once these gaps are understood, the next step is to look at the specific tactics fraudsters use to turn normal refund workflows into repeat abuse channels.

Related Read: How Businesses Detect and Prevent Payment Fraud

What Are the Most Common Refund Fraud Tactics?

Refund fraud usually follows a few repeatable patterns. The details vary by industry, but most tactics exploit the same gaps: weak proof checks, fast refund approvals, disconnected systems, or limited visibility across accounts.

1. False Item-Not-Received Claims

Fraudsters claim an order never arrived, even when it was delivered. This is common in eCommerce, food delivery, marketplaces, and logistics-heavy businesses where support teams may not have enough delivery evidence in one place.

For example, a buyer receives a high-value item, tells support that the package never arrived, and gets a refund or replacement before the business verifies proof of delivery.

These claims often target products that are expensive, easy to resell, or shipped through low-verification delivery flows.

2. Wardrobing or Use-and-Return Abuse

Wardrobing happens when someone buys an item, uses it temporarily, and returns it as unused. It is common with fashion, electronics, luxury products, home goods, event purchases, and seasonal items.

Even when the item comes back, the business still loses value. The product may be damaged, opened, out of season, missing packaging, or no longer sellable at full price.

3. Receipt Fraud and Fake Proof

Fraudsters may use fake, altered, stolen, or discarded receipts to claim refunds they do not qualify for. In online flows, they may submit:

Edited screenshots

Fake order emails

Manipulated delivery images

Forged proof of purchase

As AI-generated images and documents become easier to create, high-value refund claims need stronger proof validation. In some cases, businesses may need identity document verification to confirm customer identity, ownership, or supporting evidence before approving refunds.

4. Product Swap and Bricking Fraud

In product swap fraud, a customer buys a genuine item and returns a counterfeit, older, cheaper, damaged, or incomplete version instead. This is especially risky for high-value goods with serial numbers, branded packaging, or resale value.

The loss also extends beyond the refund itself. LiquiDonate’s 2026 Returns Fraud Report found that retailers estimate 15% of all returns are fraudulent, while each return can cost $25 to $30 in shipping, processing, and handling.

Bricking is a common tactic in electronics where a fraudster may remove valuable components, damage the product, or return a non-working item while claiming it arrived defective.

5. Duplicate Refund and Chargeback-Linked Fraud

Some customers request a merchant refund and then file a card chargeback for the same transaction. Others claim the refund was never received and push customer support for a second refund.

This creates a double-loss problem. The business may lose the refunded amount, the product or service value, and additional dispute fees tied to the chargeback.

The MRC’s 2026 Global eCommerce Payments and Fraud Report found that 62% of merchants reported an increase in first-party misuse disputes, while 57% saw refund and policy abuse rise over the past year.

6. Multi-Account Refund Abuse and Refund Rings

Fraudsters often create multiple accounts to bypass refund limits or avoid detection after earlier abuse. They may rotate information to appear like different customers, such as:

Phone numbers

Emails

Delivery addresses

IP (Internet Protocol) addresses

Payment methods

Devices

Organized refund rings can scale this through online communities, Telegram channels, scripts, or “refunding services.” This is where linked signals matter.

What Are the Warning Signs of Refund Fraud and Refund Abuse?

Refund fraud is easier to catch when teams stop reviewing claims one by one and start looking for unusual patterns across accounts, payments, devices, support activity, and refund outcomes.

Key warning signs include:

Refund frequency is higher than the customer’s purchase history supports

Multiple accounts share the same device, address, phone number, payment method, or behavioral pattern

Refund requests come from new accounts with limited order history

Refund-heavy customers contact support through multiple channels to get a different outcome

Refunds are requested to a different payment method, wallet, gift card, or store credit

A denied refund is followed by a payment dispute or chargeback

Return tracking does not match delivery, pickup, carrier, or warehouse data

The same support agent approves an unusually high number of exceptions

Several accounts show similar refund timing, language, navigation behavior, or escalation patterns

None of these signals proves fraud alone, but the risk becomes clearer when they cluster. For example, a new account requesting a refund is not automatically suspicious. But if that account shares a device with several refund-heavy users, uses a different refund method, and shows scripted support behavior, it deserves closer review.

This is where behavioral biometrics can add context by identifying bot-like activity, scripted sessions, fraud farm behavior, and unusual interaction patterns behind refund requests.

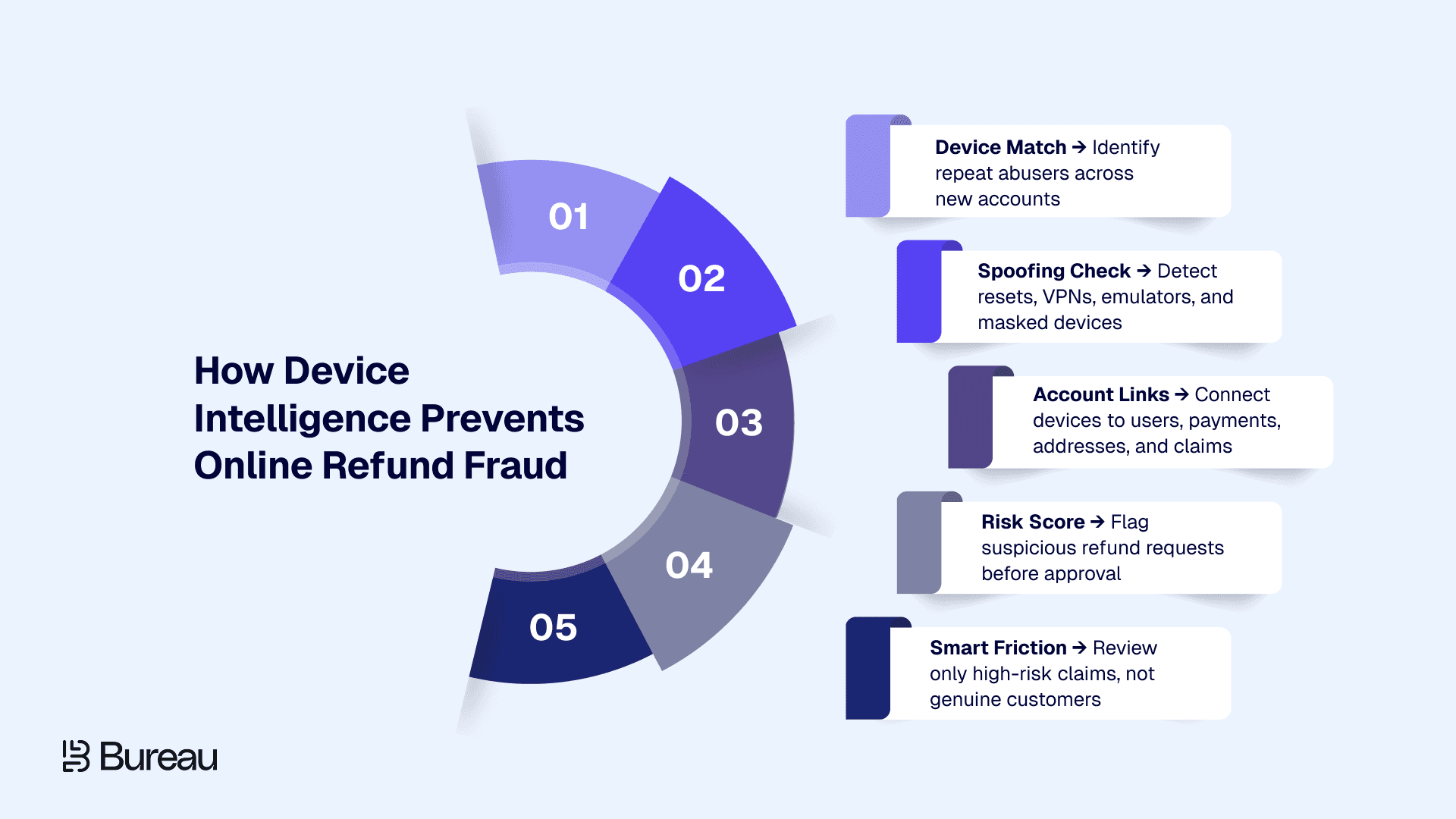

How Can Device Intelligence Help Prevent Online Refund Fraud?

Device intelligence helps teams look beyond the account making the refund request and identify the device and session behind it. This makes it easier to detect repeat refund abusers, refund rings, suspicious device behavior, and high-risk refund patterns before approving refunds or replacements.

Step 1: Identify Repeat Refund Abusers Across New Accounts

Fraudsters often create new accounts after reaching refund limits or getting flagged for earlier abuse. Device intelligence helps connect these accounts when they originate from the same or related devices. This can reveal patterns such as:

A user creating new accounts after refund limits are reached

Multiple accounts requesting refunds for similar products or reasons

Different identities showing the same device, browser, app, or behavioral signals

A refund-heavy customer repeatedly changing email IDs, phone numbers, or names

With Bureau ID's Device ID, businesses can recognize repeat users even when account-level details keep changing.

Step 2: Detect Device Resets, Spoofing, Emulators, and VPN Use

Refund fraudsters may try to hide behind device resets, incognito browsing, VPNs, proxies, emulators, or spoofed app environments. Device intelligence can flag these signals during refund requests, especially when the claim is high-value or unusual.

Useful signals include:

Device reset before account creation or refund request

VPN, proxy, TOR, or location masking signals

Emulator or virtual device usage

Spoofed app, browser, or SDK signals

Device changes after delivery or right before a refund claim

These signals do not prove fraud on their own, but when they appear alongside refund history, order value, delivery evidence, and payment behavior, they can help teams separate normal customer issues from risky claims.

Step 3: Link Refund Requests to Devices, Accounts, Payments, and Addresses

Device intelligence becomes more useful when it is connected with account, payment, delivery, and transaction data.

Instead of asking, “Does this refund request look valid?”, teams can ask, “Where else have we seen this device, account, address, payment method, or behavior before?”

Bureau ID’s Graph Identity Network can help connect accounts, devices, behaviors, and identities that may look unrelated in isolation, making coordinated refund abuse easier to detect.

Step 4: Score Risky Refund Requests Before Approval

Device intelligence can help create a risk score before money, store credit, or a replacement is issued.

A risk score helps teams decide what should happen next: approve the refund instantly, request more evidence, route the case to fraud review, delay release until inspection, or restrict the refund method. This keeps low-risk refunds fast while giving fraud teams more control over claims that carry higher loss potential.

Step 5: Add Friction Only for High-Risk Refund Claims

The goal is not to make refunds harder for everyone. The goal is to keep refunds fast for genuine customers while applying extra checks only when risk signals appear.

Selective friction can include:

Asking for additional delivery proof only for high-risk claims

Triggering identity or ownership verification for high-value refund requests

Holding refund approval until returned items are inspected

Routing suspicious refund requests to fraud review

Limiting refund methods when device and payment signals do not match

This approach protects revenue without turning every refund into a poor customer experience.

Related Read: How to Detect First-Party Fraud Before Losses Escalate

Device Intelligence Checklist for Refund Fraud PreventionUse this checklist to assess whether your refund fraud prevention process can detect repeat abuse without slowing down genuine customers:

|

How Can Businesses Detect Refund Fraud With Bureau ID?

Bureau ID helps businesses detect refund fraud by acting as a unified risk decisioning layer across user touchpoints. It combines device, identity, behavior, network, and transaction signals to give teams more context before approving refunds, replacements, credits, or chargeback-linked claims.

That helps businesses:

Detect repeat refund abusers even when they create new accounts

Identify linked accounts, shared devices, suspicious behaviors, and refund rings

Score risky refund or chargeback behavior before loss occurs

Apply extra checks only when the risk is high

Keep genuine refunds fast and low-friction

The aim is to understand whether the request fits the customer’s normal behavior, account history, device pattern, payment activity, and connected network before a decision is made.

The impact of this approach becomes clearer when we look at how it works in practice.

Case Study: How a Leading PropTech Saved $1.25M in Chargeback Fraud With Bureau ID

Refund fraud and chargeback fraud often overlap when customers or fraudsters use payment disputes to reverse legitimate transactions. A leading PropTech platform was losing revenue because credit card rent payments created an opportunity for fake chargebacks, with 20% of such payments resulting in disputes.

What Bureau ID implemented:

Used alternate data to strengthen risk assessment

Built custom risk models tailored to chargeback behavior

Enabled real-time decisioning to evaluate users and transactions before payment completion

Results achieved:

Prevented $1.25M in chargeback fraud in three months

Reduced false chargeback rates from 40% to 8%

Stopped 1,200+ high-risk transactions before payment

Flagged 60,000+ users as high-risk for chargeback fraud

Restricted credit card payments for risky users

Read the full case study here → A Leading PropTech Saves $1.25M in Chargeback Fraud

Refund fraud prevention works best when businesses can see the full pattern behind the claim. A single refund request may look harmless, but connected risk signals can reveal whether it is part of a larger abuse cycle.

Protect Your Revenue From Refund Fraud

Refund fraud often looks like a frustrated customer, a missing package, a refund delay, or a one-time exception that support approves to keep the experience smooth.

Bureau ID connects device, identity, behavior, network, and transaction signals so teams can see whether a refund request fits normal customer behavior or points to repeat abuse. This helps businesses detect:

Linked accounts

Refund rings

Risky claims

Repeated refund requests

Frequent claims

If refund abuse is becoming harder to separate from genuine customer issues, it may be time to review where your current workflows are missing context. Schedule a demo with Bureau ID to see how unified risk decisioning can help protect revenue without slowing down trusted customers.

FAQs

1. What is refund fraud?

Refund fraud is when someone manipulates a business into issuing a refund, replacement, store credit, chargeback, or reimbursement to which they are not entitled. It can happen through false claims, fake proof, product swaps, duplicate refunds, or repeated refund abuse.

2. What are common examples of refund fraud?

Common refund fraud examples include false item-not-received claims, wardrobing, fake receipts, empty box scams, product swaps, bricking, duplicate refund requests, and chargeback-linked fraud. These tactics exploit gaps in refund policies, delivery checks, payment workflows, or customer support processes.

3. What is the difference between return fraud and refund fraud?

Return fraud is a type of refund fraud that involves manipulating the product return process. Refund fraud is broader and can involve returns, chargebacks, digital products, subscriptions, delivery claims, store credits, or reimbursements where no physical return happens.

4. How can businesses prevent refund fraud?

Businesses can prevent refund fraud by using clear refund policies, purchase matching, delivery verification, return inspection, chargeback monitoring, support training, device intelligence, and risk-based decisioning. The goal is to review risky claims without making refunds harder for genuine customers.

5. What are signs of refund abuse?

Signs of refund abuse include unusually high refund frequency, multiple accounts sharing the same device or payment method, refund requests from new accounts, repeated support escalations, refund requests to different payment methods, and chargebacks after denied refund claims.

6. How does device intelligence help with refund fraud prevention?

Device intelligence helps businesses identify the device and session behind a refund request. This makes it easier to detect repeat refund abusers, linked accounts, suspicious device behavior, VPN or emulator use, and refund rings even when fraudsters change visible account details.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.