How to Build a Fraud Risk Framework That Reduces Exposure

How to Build a Fraud Risk Framework That Reduces Exposure

How to Build a Fraud Risk Framework That Reduces Exposure

Learn fraud risk management principles, framework steps, and assessment methods to identify exposure, reduce losses, and strengthen controls.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

Fraud can surface from users, accounts, and workflows that look trustworthy until risk signals start connecting. A user may pass onboarding, complete login, claim offers, move funds, or request refunds before fraud becomes visible.

For fraud and risk teams, this makes fraud risk management a lifecycle discipline that extends beyond post-transaction alerts. A strong program helps teams identify where fraud can occur, assess severity, monitor user and transaction behavior in real time, apply the right controls, and respond before losses become irreversible.

This guide breaks down the core principles, risk categories, assessment methods, and framework steps needed to manage fraud risk effectively across onboarding, authentication, transaction monitoring, and response workflows.

What Is Fraud Risk Management?

Fraud risk management is the process of identifying, assessing, preventing, detecting, and responding to fraud risks across an organization. It brings together governance, internal controls, transaction monitoring, fraud detection, and response workflows to reduce losses, protect customers, and strengthen operational resilience.

Fraud risks usually fall into two broad categories:

Internal fraud risks: Embezzlement, access misuse, control failures, payroll fraud, expense fraud, procurement fraud, and unauthorized activity by employees or vendors.

External fraud risks: Account takeover, synthetic identity fraud, mule accounts, payment fraud, promo abuse, bot attacks, and coordinated fraud rings.

For digital businesses, fraud risk management also needs to account for the activity that happens before the final transaction. Risk may start building through a clean login, new device, beneficiary addition, profile edit, password reset, or unusual session behavior. If those signals are evaluated only after payment execution, the recovery window is often gone.

This is why modern fraud risk management depends on continuous monitoring across identity, device, behavior, account activity, and transaction context. The strongest frameworks help teams detect risk early, apply the right control, and trigger actions such as allow, step-up, block, alert, or case review before losses become difficult to recover.

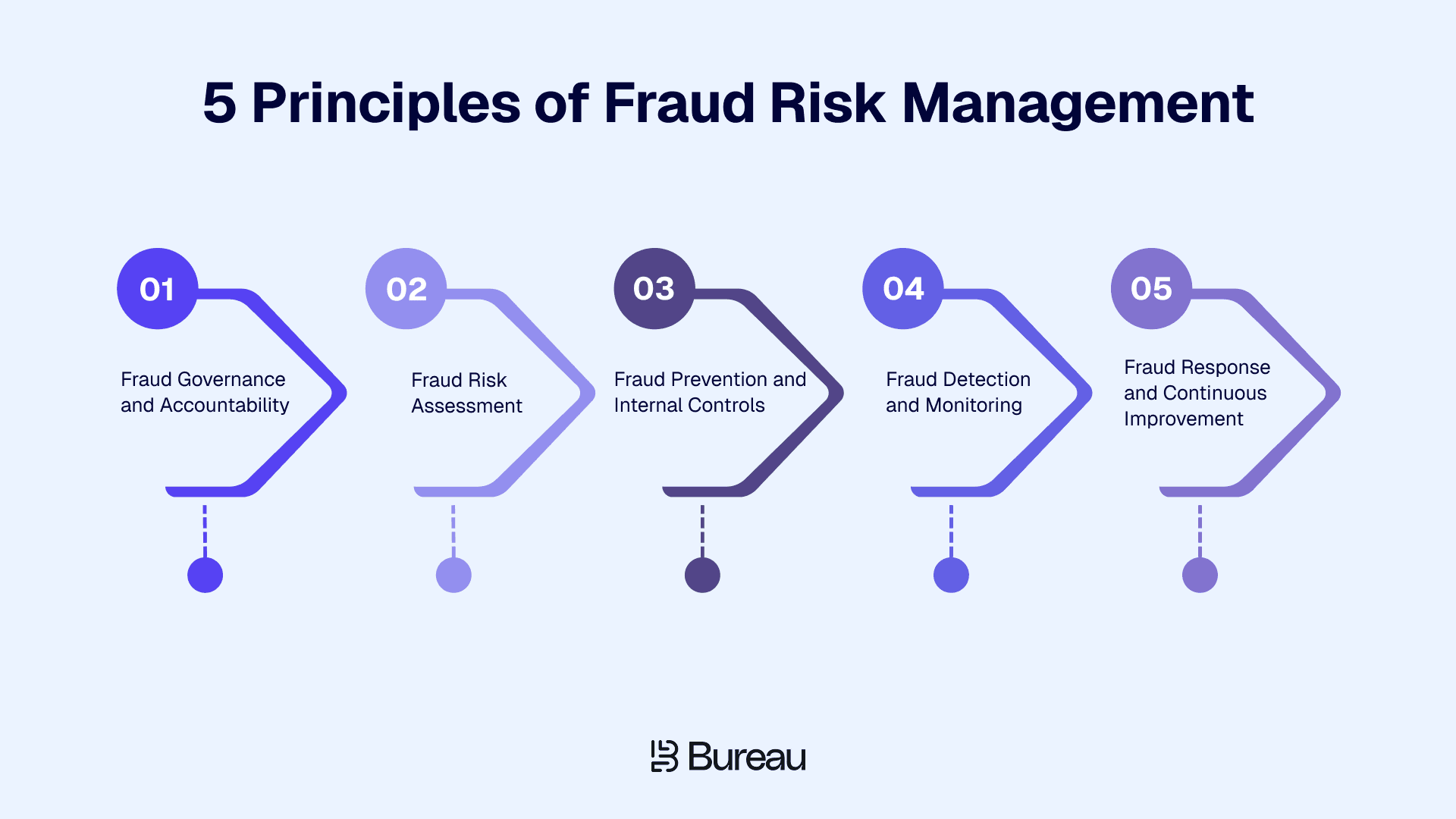

What Are the 5 Principles of Fraud Risk Management?

Most fraud risk management frameworks are built around five connected principles: governance, risk assessment, prevention, detection, and response.

Together, they help organizations move from reactive fraud handling to a structured program that reduces risk over time.

1. Fraud Governance and Accountability

Fraud governance defines ownership, accountability, policies, escalation paths, reporting lines, decision authority, and risk appetite.

For example, a fintech launching a new onboarding flow should define who approves verification rules, reviews high-risk users, escalates suspected mule activity, and updates controls after confirmed fraud.

This ownership should extend across leadership, risk, compliance, finance, product, operations, and fraud teams. Product flows, payment rules, customer support workflows, and onboarding journeys can all affect fraud exposure.

2. Fraud Risk Assessment

Fraud risk assessment is the process of identifying fraud schemes, estimating likelihood and impact, reviewing existing controls, and prioritizing residual risks.

A lending platform may assess synthetic identity fraud by reviewing past fraud cases, suspicious activity reports, audit findings, customer complaints, transaction data, and fraud team interviews.

A strong assessment should answer where fraud could occur, how likely it is, what damage it could cause, what controls exist, and what risk remains after those controls.

3. Fraud Prevention and Internal Controls

Fraud prevention uses controls designed to stop fraud before losses occur.

For instance, a digital bank may use multiple strategies to reduce fake account creation. This includes:

KYC/KYB checks

Device intelligence

Transaction limits

Risk-based onboarding

These controls should also account for pre-transaction risk signals, such as device changes, beneficiary additions, profile edits, and payment authorization attempts, so teams can step up, block, or review suspicious activity before losses occur.

Internal controls may include access controls, approval workflows, segregation of duties, vendor checks, expense approvals, payroll controls, and audit trails. Digital controls may include document verification, device fingerprinting, behavioral analytics, and bot prevention.

4. Fraud Detection and Monitoring

Fraud detection and monitoring identify suspicious activity that prevention controls miss. In digital journeys, that means monitoring more than the final transaction because risk often builds earlier through logins, device changes, beneficiary edits, profile updates, account recovery, or payment authorization attempts.

A user may appear low-risk during onboarding, then show risk later through unusual transaction velocity, location shifts, abnormal session behavior, or linked-account activity.

Connected signals across identity, device, behavior, network, and transactions help teams detect these patterns early and trigger the right action: allow, step up, block, alert, or route for review before funds move.

5. Fraud Response and Continuous Improvement

Fraud response defines what happens after suspicious activity is detected.

For example, a suspicious login may trigger step-up verification, account restrictions, evidence capture, case review, user communication, and escalation if the risk is confirmed.

For high-value journeys, the response should also include real-time actions such as allow, step up, block, alert, or route to review, so suspicious activity can be contained before a transaction, payout, or account change is completed.

A response workflow should define who reviews the alert, what evidence is required, what action should be taken, when compliance or leadership should be notified, and how the case should be documented. Confirmed fraud should feed back into rules, models, workflows, and risk assessments.

Related Read: How Businesses Can Stop AI Identity Fraud With Connected Risk Intelligence

What Types of Fraud Risks Should Organizations Assess?

Organizations should assess both internal and external fraud risks. Internal risks usually come from control gaps, employee misconduct, or weak oversight, while external risks come from fake users, bots, stolen credentials, synthetic identities, abusive transactions, and organized fraud rings.

Key categories include:

Internal Fraud: Embezzlement, payroll fraud, expense fraud, procurement fraud, asset misuse, reporting manipulation, and unauthorized access.

Identity Fraud: Synthetic identities, stolen identities, fake documents, deepfake-assisted checks, fake profiles, and mule account creation.

Account Takeover: Stolen credentials, SIM swaps, phishing, or social engineering are used to access legitimate accounts, making account takeover protection important for suspicious login detection.

Transaction and Payment Fraud: Chargebacks, unauthorized transactions, refund abuse, payment misuse, suspicious fund movement, and pre-transaction risk signals such as beneficiary edits or payment authorization anomalies.

Promo, Bot, and Collusion Risk: Multi-accounting, referral abuse, credential stuffing, fake signups, scraping, and coordinated fraud rings.

The strongest assessment links risks across signup, verification, login, recovery, transactions, promotions, withdrawals, refunds, and monitoring. Bureau ID helps teams connect device, identity, behavioral, network, and transaction signals so risks that look isolated can be assessed as part of a larger fraud pattern.

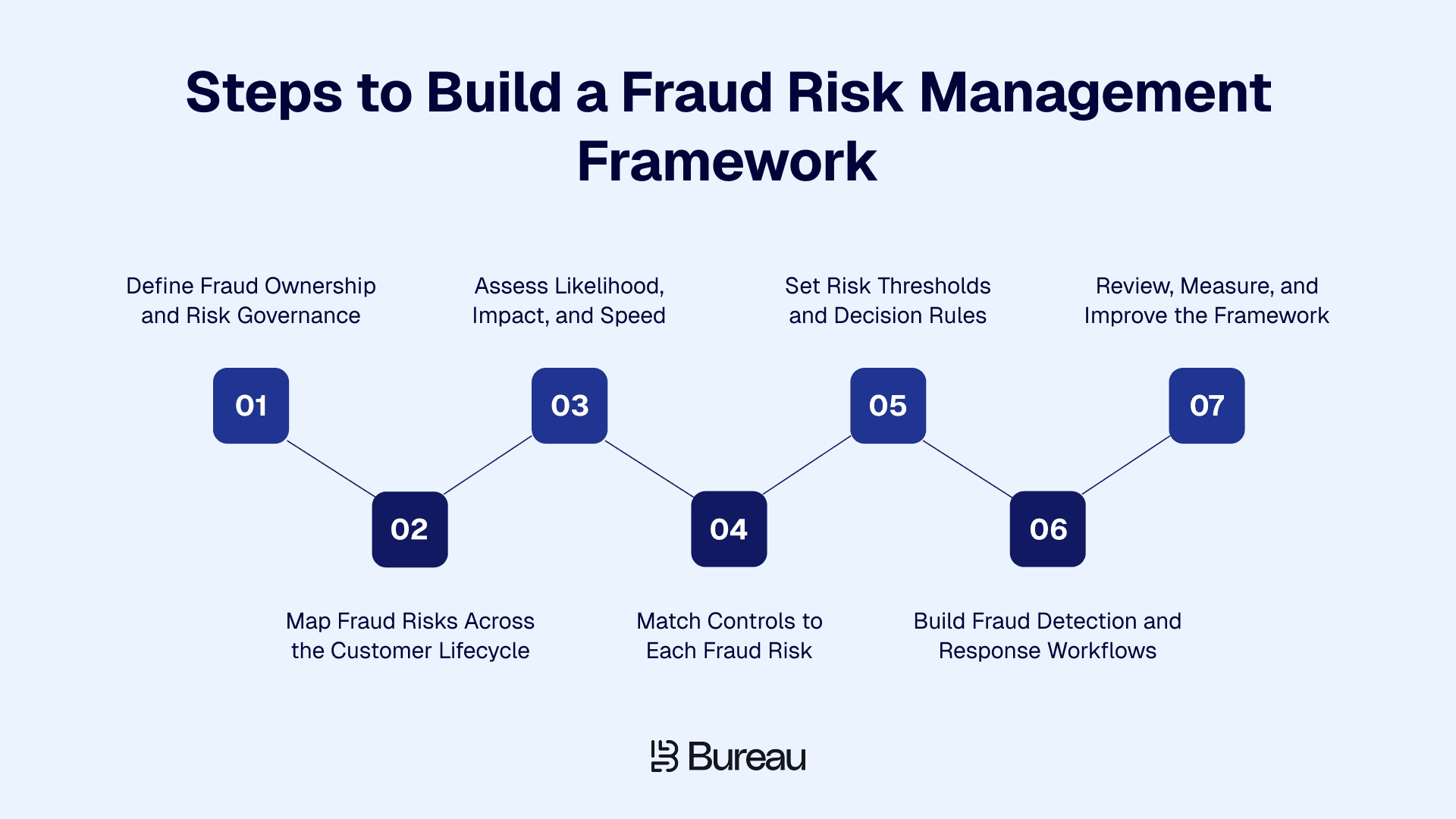

How to Build a Fraud Risk Management Framework?

A fraud risk management framework connects governance, risk assessment, internal controls, monitoring, and response workflows. It gives teams a repeatable way to understand where fraud can happen, what damage it can cause, and which controls reduce exposure.

Step 1: Define Fraud Ownership and Risk Governance

Start by assigning fraud ownership across leadership, risk, compliance, fraud operations, product, engineering, finance, and customer support.

For high-risk businesses, governance should cover strategic oversight and daily decision ownership. Teams may detect fraud quickly but still struggle to act without clear authority.

Define:

Who approves risk thresholds

Who owns manual review

Who handles escalation

Who updates controls after confirmed fraud

What risk levels are acceptable by product, geography, user type, and transaction type

A simple RACI matrix can prevent confusion during high-risk events.

Step 2: Map Fraud Risks Across the Customer Lifecycle

A framework should map fraud risks across every major customer touchpoint.

For example, an eCommerce platform may see fake accounts at signup, promo abuse after account creation, chargeback fraud after purchase, and return-to-origin abuse after fulfillment.

Map risks across:

Onboarding

Identity verification

Login

Account recovery

Transactions

Promotions and referrals

Refunds or withdrawals

Ongoing account activity

Also map pre-transaction events where risk often accumulates before loss, including beneficiary changes, profile edits, device updates, and payout detail changes.

This helps teams see where repeat offenders reappear across accounts, devices, and lifecycle stages. Bureau ID’s Device ID can support this by connecting suspicious device activity across different users and journeys.

Step 3: Assess Likelihood, Impact, and Speed

Fraud risk scoring should look beyond the size of a single loss. A low-value fraud tactic can become high-risk if it scales quickly across thousands of accounts.

Factor | What to assess |

Likelihood | How often could this fraud occur? |

Impact | What financial, customer, regulatory, or operational damage could it cause? |

Speed | How quickly could the fraud scale before detection? |

Exposure | Which products, users, regions, or channels are most affected? |

Speed matters because fraud exposure can grow faster than loss teams expect. The FBI’s 2024 Internet Crime Report recorded more than $16B in reported losses from 859,532 complaints, with losses up 33% from 2023. That kind of increase is why frameworks should assess how quickly a fraud pattern can scale.

This makes prioritization more practical, especially when fraud teams must choose which risks need immediate controls.

Step 4: Match Controls to Each Fraud Risk

Each fraud risk should have controls matched to how it appears.

For account takeover, preventive controls may include MFA and device recognition. Detective controls may include behavioral anomaly detection. Corrective controls may include step-up verification, temporary account holds, and user notifications.

Controls should also map to the stage where risk appears. A beneficiary addition or device change may call for step-up verification, while a high-risk payment attempt may require a block, hold, or case review before the transaction is completed.

Use four control types:

Preventive controls: Stop fraud before it happens, such as KYC, KYB, access controls, and device checks.

Detective controls: Identify suspicious activity through anomaly alerts, transaction monitoring, and velocity checks.

Corrective controls: Limit damage through account freezes, transaction holds, and case escalation.

Continuous controls: Improve rules, models, and workflows through feedback loops.

For connected risks, Bureau ID’s Graph Identity Network can help surface relationships across accounts, devices, identities, and behaviors.

Step 5: Set Risk Thresholds and Decision Rules

Risk thresholds define what happens at different levels of suspicion. Every suspicious signal should not become an automatic block.

A new device, unusual location, or velocity spike may require review, step-up verification, or monitoring before rejection.

Risk level | Typical action |

Low | Approve |

Medium | Step-up verification or monitor |

High | Manual review or transaction limits |

Critical | Block, freeze, reject, or escalate |

These thresholds should apply to both financial and non-financial events, so teams can score risk during logins, profile edits, device updates, beneficiary changes, and payment authorization instead of waiting for a completed transaction.

A unified risk decisioning platform supports this approach by helping teams turn connected risk signals into explainable decisions.

Step 6: Build Fraud Detection and Response Workflows

Response workflows define how teams act when suspicious activity appears. They should cover both transaction events and pre-transaction signals, such as suspicious logins, device updates, beneficiary changes, profile edits, and payment authorization attempts.

A typical workflow may look like this:

Suspicious login → Behavioral anomaly detected → Step-up verification triggered → Failed verification → Account temporarily restricted → Case reviewed → Rule updated

For high-risk journeys, workflows should trigger the right action based on risk state: allow trusted activity, step up suspicious users, block high-risk attempts, alert fraud operations, or route cases for review before funds move or account details change.

Define alert routing, required evidence, response SLAs, escalation rules, and documentation standards. Confirmed fraud cases should feed future decisions instead of staying inside case notes.

Bureau ID’s configurable workflows help teams adjust rules, thresholds, and verification steps as new patterns appear, while supporting real-time actions across allow, step-up, block, alerts, and governed case workflows.

Step 7: Review, Measure, and Improve the Framework

A fraud risk management framework should improve as fraud patterns change. That only happens when teams measure both fraud outcomes and control performance.

Track metrics such as:

Fraud loss rate

Fraud prevented before loss

False positive rate

False negative rate

Manual review rate

Alert-to-action time

Onboarding pass rate

Chargeback or dispute rate

Repeat offender rate

Customer friction caused by fraud checks

Measurement should include both losses and prevented losses. UK Finance reported £1.17 billion stolen through authorized and unauthorized fraud in 2024, while banks prevented £1.45 billion of unauthorized fraud through security systems. That distinction helps teams evaluate whether controls are reducing exposure before losses materialize.

Review the framework after product launches, market expansion, major fraud incidents, regulatory changes, or sudden spikes in suspicious activity.

A Template to Conduct a Fraud Risk Assessment

A fraud risk assessment helps your teams move from assumptions to a clear view of organizational exposure. The primary objective is to catalog the most relevant fraud scenarios, score their prospective risk levels, review existing controls, and isolate the exact gaps that require architectural change.

The following fraud risk assessment matrix provides a condensed, high-level structural template to track core vulnerabilities across your platform:

Fraud Risk Scenario | Journey Stage | Risk Level | Existing Controls | Core Control Gap |

Synthetic Identity Fraud | Onboarding | High | Document Verification, KYC | Weak Device and Network Checks |

Account Takeover | Login & Account Changes | High | Password, MFA | Limited Behavioral and Device Monitoring |

Promo Abuse | Signup & Referral | Medium | Referral Limits | Repeat Devices Not Detected |

Chargeback Fraud | Payment Authorization & Transaction | High | Payment Review | Limited Pre-Transaction Risk Scoring |

Mule Account Activity | Onboarding & Transact | Critical | KYC, Transaction Rules | Weak Network Link Analysis |

Start with risks that affect revenue, compliance, customer trust, or workload. Score likelihood and impact as low, medium, or high. Prioritize high-impact risks with weak controls, then assign an owner and next action.

How Bureau ID Supports Fraud Risk Management

Bureau ID helps businesses strengthen fraud risk management by connecting identity, device, behavior, network, and transaction signals in one risk decisioning layer. The platform helps risk teams evaluate the full context behind each user action, from onboarding and login to transactions, account activity, and reviews.

Its role is especially relevant for high-risk digital businesses that face synthetic identity fraud, account takeover, mule activity, chargeback fraud, promo abuse, bot attacks, and repeat abuse across the customer lifecycle.

Bureau ID supports this through:

Device ID: Identifies suspicious devices, spoofed environments, emulators, VPN usage, repeat offenders, and device-account relationships.

Identity Document Verification: Validates user authenticity through document checks, biometric matching, liveness detection, and onboarding risk checks.

Behavioral Biometrics: Looks at how users interact with devices to spot bots, scripted behavior, fraud farms, impersonation, and suspicious sessions.

Alternate Data: Adds more context to user and transaction trust using digital footprint, email quality, phone intelligence, and other risk indicators.

Configurable Workflows: Risk teams can configure rules, thresholds, review flows, and step-up actions without depending on engineering for every change.

Explainable Decisions: Fraud investigators get context behind risk scores, which helps with investigations, audit trails, compliance reviews, and control tuning.

For fraud and risk teams, this means moving from isolated checks to a connected view of risk. Teams can see how identity, device, behavior, network, and transaction signals interact in real time.

Case Study: How Bureau ID Helped a PropTech Company Prevent $1.25M in Chargeback Fraud

A leading PropTech company was facing chargeback fraud on credit card rent payments. The challenge was to stop high-risk transactions before payment without disrupting legitimate renters or damaging the smooth payment experience.

The company implemented Bureau’s alternate data, custom risk models, and real-time decisioning to assess user and transaction risk before payment. Bureau ID evaluated 200+ live signals, including telco metadata, UPI integrity, email quality, identity consistency, transaction attributes, and digital footprint.

In three months, the company was able to:

Prevent $1.25M in chargeback fraud.

Reduce false chargeback rates from 40% to 8%.

Stop 1,200+ high-risk transactions before payment.

Flag 60,000+ users as high-risk for chargeback fraud.

Restrict credit card rent payments for risky users.

Read the full case study here → A Leading PropTech Saves $1.25M in Chargeback Fraud

A simple takeaway from this case study is that fraud risk management works best when risk decisions happen before losses occur. Businesses that connect identity, device, behavior, network, and transaction signals can reduce exposure while keeping trusted users moving.

Build a Stronger Fraud Risk Management Program

The most dangerous fraud pattern is often the one that looks legitimate until signals connect across the customer lifecycle.

As fraud moves across onboarding, login, payments, refunds, promotions, and ongoing account activity, the next step is to evaluate whether your controls work together or operate in silos.

By connecting identity, device, behavior, network, and transaction signals in a single decisioning layer, Bureau ID helps teams detect fraud earlier and respond with more precision. That means fewer broad rules, fewer unnecessary reviews, and stronger controls where the risk is real.

If you want to see how unified risk decisioning can help your team strengthen controls, reduce false positives, and adapt faster, book a demo with Bureau ID today.

FAQs

1. What is the main purpose of fraud risk management?

Fraud risk management helps organizations identify where fraud can occur, assess how serious the risk is, and apply the right controls. Its goal is to reduce losses, protect customers, and respond faster when suspicious activity appears.

2. What are the 5 principles of fraud risk management?

The five principles are fraud governance, risk assessment, prevention, detection, and response. Together, they help organizations define ownership, understand exposure, set controls, monitor suspicious activity, and improve the program as fraud patterns change.

3. How is fraud risk management different from fraud detection?

Fraud detection focuses on identifying suspicious activity. Fraud risk management is broader. It includes governance, risk assessment, internal controls, prevention, real-time transaction monitoring, pre-transaction risk evaluation, investigation, response, reporting, and continuous improvement across the organization.

4. How often should an organization assess fraud risk?

Organizations should assess fraud risk at least once a year. High-risk businesses should also reassess after product launches, market expansion, regulatory changes, major fraud incidents, or sudden increases in chargebacks, fake accounts, or suspicious transactions.

5. What are common fraud risks for digital businesses?

Common fraud risks include synthetic identity fraud, account takeover, promo abuse, chargeback fraud, bot attacks, mule accounts, fake profiles, and transaction fraud. These risks often appear across onboarding, login, payment, referral, refund, and monitoring workflows.

6. What should a fraud risk management framework include?

A fraud risk management framework should include clear ownership, fraud risk assessment, preventive controls, detection systems, response workflows, reporting processes, and performance metrics. It should also be updated regularly as fraud tactics and business risks evolve.

Fraud can surface from users, accounts, and workflows that look trustworthy until risk signals start connecting. A user may pass onboarding, complete login, claim offers, move funds, or request refunds before fraud becomes visible.

For fraud and risk teams, this makes fraud risk management a lifecycle discipline that extends beyond post-transaction alerts. A strong program helps teams identify where fraud can occur, assess severity, monitor user and transaction behavior in real time, apply the right controls, and respond before losses become irreversible.

This guide breaks down the core principles, risk categories, assessment methods, and framework steps needed to manage fraud risk effectively across onboarding, authentication, transaction monitoring, and response workflows.

What Is Fraud Risk Management?

Fraud risk management is the process of identifying, assessing, preventing, detecting, and responding to fraud risks across an organization. It brings together governance, internal controls, transaction monitoring, fraud detection, and response workflows to reduce losses, protect customers, and strengthen operational resilience.

Fraud risks usually fall into two broad categories:

Internal fraud risks: Embezzlement, access misuse, control failures, payroll fraud, expense fraud, procurement fraud, and unauthorized activity by employees or vendors.

External fraud risks: Account takeover, synthetic identity fraud, mule accounts, payment fraud, promo abuse, bot attacks, and coordinated fraud rings.

For digital businesses, fraud risk management also needs to account for the activity that happens before the final transaction. Risk may start building through a clean login, new device, beneficiary addition, profile edit, password reset, or unusual session behavior. If those signals are evaluated only after payment execution, the recovery window is often gone.

This is why modern fraud risk management depends on continuous monitoring across identity, device, behavior, account activity, and transaction context. The strongest frameworks help teams detect risk early, apply the right control, and trigger actions such as allow, step-up, block, alert, or case review before losses become difficult to recover.

What Are the 5 Principles of Fraud Risk Management?

Most fraud risk management frameworks are built around five connected principles: governance, risk assessment, prevention, detection, and response.

Together, they help organizations move from reactive fraud handling to a structured program that reduces risk over time.

1. Fraud Governance and Accountability

Fraud governance defines ownership, accountability, policies, escalation paths, reporting lines, decision authority, and risk appetite.

For example, a fintech launching a new onboarding flow should define who approves verification rules, reviews high-risk users, escalates suspected mule activity, and updates controls after confirmed fraud.

This ownership should extend across leadership, risk, compliance, finance, product, operations, and fraud teams. Product flows, payment rules, customer support workflows, and onboarding journeys can all affect fraud exposure.

2. Fraud Risk Assessment

Fraud risk assessment is the process of identifying fraud schemes, estimating likelihood and impact, reviewing existing controls, and prioritizing residual risks.

A lending platform may assess synthetic identity fraud by reviewing past fraud cases, suspicious activity reports, audit findings, customer complaints, transaction data, and fraud team interviews.

A strong assessment should answer where fraud could occur, how likely it is, what damage it could cause, what controls exist, and what risk remains after those controls.

3. Fraud Prevention and Internal Controls

Fraud prevention uses controls designed to stop fraud before losses occur.

For instance, a digital bank may use multiple strategies to reduce fake account creation. This includes:

KYC/KYB checks

Device intelligence

Transaction limits

Risk-based onboarding

These controls should also account for pre-transaction risk signals, such as device changes, beneficiary additions, profile edits, and payment authorization attempts, so teams can step up, block, or review suspicious activity before losses occur.

Internal controls may include access controls, approval workflows, segregation of duties, vendor checks, expense approvals, payroll controls, and audit trails. Digital controls may include document verification, device fingerprinting, behavioral analytics, and bot prevention.

4. Fraud Detection and Monitoring

Fraud detection and monitoring identify suspicious activity that prevention controls miss. In digital journeys, that means monitoring more than the final transaction because risk often builds earlier through logins, device changes, beneficiary edits, profile updates, account recovery, or payment authorization attempts.

A user may appear low-risk during onboarding, then show risk later through unusual transaction velocity, location shifts, abnormal session behavior, or linked-account activity.

Connected signals across identity, device, behavior, network, and transactions help teams detect these patterns early and trigger the right action: allow, step up, block, alert, or route for review before funds move.

5. Fraud Response and Continuous Improvement

Fraud response defines what happens after suspicious activity is detected.

For example, a suspicious login may trigger step-up verification, account restrictions, evidence capture, case review, user communication, and escalation if the risk is confirmed.

For high-value journeys, the response should also include real-time actions such as allow, step up, block, alert, or route to review, so suspicious activity can be contained before a transaction, payout, or account change is completed.

A response workflow should define who reviews the alert, what evidence is required, what action should be taken, when compliance or leadership should be notified, and how the case should be documented. Confirmed fraud should feed back into rules, models, workflows, and risk assessments.

Related Read: How Businesses Can Stop AI Identity Fraud With Connected Risk Intelligence

What Types of Fraud Risks Should Organizations Assess?

Organizations should assess both internal and external fraud risks. Internal risks usually come from control gaps, employee misconduct, or weak oversight, while external risks come from fake users, bots, stolen credentials, synthetic identities, abusive transactions, and organized fraud rings.

Key categories include:

Internal Fraud: Embezzlement, payroll fraud, expense fraud, procurement fraud, asset misuse, reporting manipulation, and unauthorized access.

Identity Fraud: Synthetic identities, stolen identities, fake documents, deepfake-assisted checks, fake profiles, and mule account creation.

Account Takeover: Stolen credentials, SIM swaps, phishing, or social engineering are used to access legitimate accounts, making account takeover protection important for suspicious login detection.

Transaction and Payment Fraud: Chargebacks, unauthorized transactions, refund abuse, payment misuse, suspicious fund movement, and pre-transaction risk signals such as beneficiary edits or payment authorization anomalies.

Promo, Bot, and Collusion Risk: Multi-accounting, referral abuse, credential stuffing, fake signups, scraping, and coordinated fraud rings.

The strongest assessment links risks across signup, verification, login, recovery, transactions, promotions, withdrawals, refunds, and monitoring. Bureau ID helps teams connect device, identity, behavioral, network, and transaction signals so risks that look isolated can be assessed as part of a larger fraud pattern.

How to Build a Fraud Risk Management Framework?

A fraud risk management framework connects governance, risk assessment, internal controls, monitoring, and response workflows. It gives teams a repeatable way to understand where fraud can happen, what damage it can cause, and which controls reduce exposure.

Step 1: Define Fraud Ownership and Risk Governance

Start by assigning fraud ownership across leadership, risk, compliance, fraud operations, product, engineering, finance, and customer support.

For high-risk businesses, governance should cover strategic oversight and daily decision ownership. Teams may detect fraud quickly but still struggle to act without clear authority.

Define:

Who approves risk thresholds

Who owns manual review

Who handles escalation

Who updates controls after confirmed fraud

What risk levels are acceptable by product, geography, user type, and transaction type

A simple RACI matrix can prevent confusion during high-risk events.

Step 2: Map Fraud Risks Across the Customer Lifecycle

A framework should map fraud risks across every major customer touchpoint.

For example, an eCommerce platform may see fake accounts at signup, promo abuse after account creation, chargeback fraud after purchase, and return-to-origin abuse after fulfillment.

Map risks across:

Onboarding

Identity verification

Login

Account recovery

Transactions

Promotions and referrals

Refunds or withdrawals

Ongoing account activity

Also map pre-transaction events where risk often accumulates before loss, including beneficiary changes, profile edits, device updates, and payout detail changes.

This helps teams see where repeat offenders reappear across accounts, devices, and lifecycle stages. Bureau ID’s Device ID can support this by connecting suspicious device activity across different users and journeys.

Step 3: Assess Likelihood, Impact, and Speed

Fraud risk scoring should look beyond the size of a single loss. A low-value fraud tactic can become high-risk if it scales quickly across thousands of accounts.

Factor | What to assess |

Likelihood | How often could this fraud occur? |

Impact | What financial, customer, regulatory, or operational damage could it cause? |

Speed | How quickly could the fraud scale before detection? |

Exposure | Which products, users, regions, or channels are most affected? |

Speed matters because fraud exposure can grow faster than loss teams expect. The FBI’s 2024 Internet Crime Report recorded more than $16B in reported losses from 859,532 complaints, with losses up 33% from 2023. That kind of increase is why frameworks should assess how quickly a fraud pattern can scale.

This makes prioritization more practical, especially when fraud teams must choose which risks need immediate controls.

Step 4: Match Controls to Each Fraud Risk

Each fraud risk should have controls matched to how it appears.

For account takeover, preventive controls may include MFA and device recognition. Detective controls may include behavioral anomaly detection. Corrective controls may include step-up verification, temporary account holds, and user notifications.

Controls should also map to the stage where risk appears. A beneficiary addition or device change may call for step-up verification, while a high-risk payment attempt may require a block, hold, or case review before the transaction is completed.

Use four control types:

Preventive controls: Stop fraud before it happens, such as KYC, KYB, access controls, and device checks.

Detective controls: Identify suspicious activity through anomaly alerts, transaction monitoring, and velocity checks.

Corrective controls: Limit damage through account freezes, transaction holds, and case escalation.

Continuous controls: Improve rules, models, and workflows through feedback loops.

For connected risks, Bureau ID’s Graph Identity Network can help surface relationships across accounts, devices, identities, and behaviors.

Step 5: Set Risk Thresholds and Decision Rules

Risk thresholds define what happens at different levels of suspicion. Every suspicious signal should not become an automatic block.

A new device, unusual location, or velocity spike may require review, step-up verification, or monitoring before rejection.

Risk level | Typical action |

Low | Approve |

Medium | Step-up verification or monitor |

High | Manual review or transaction limits |

Critical | Block, freeze, reject, or escalate |

These thresholds should apply to both financial and non-financial events, so teams can score risk during logins, profile edits, device updates, beneficiary changes, and payment authorization instead of waiting for a completed transaction.

A unified risk decisioning platform supports this approach by helping teams turn connected risk signals into explainable decisions.

Step 6: Build Fraud Detection and Response Workflows

Response workflows define how teams act when suspicious activity appears. They should cover both transaction events and pre-transaction signals, such as suspicious logins, device updates, beneficiary changes, profile edits, and payment authorization attempts.

A typical workflow may look like this:

Suspicious login → Behavioral anomaly detected → Step-up verification triggered → Failed verification → Account temporarily restricted → Case reviewed → Rule updated

For high-risk journeys, workflows should trigger the right action based on risk state: allow trusted activity, step up suspicious users, block high-risk attempts, alert fraud operations, or route cases for review before funds move or account details change.

Define alert routing, required evidence, response SLAs, escalation rules, and documentation standards. Confirmed fraud cases should feed future decisions instead of staying inside case notes.

Bureau ID’s configurable workflows help teams adjust rules, thresholds, and verification steps as new patterns appear, while supporting real-time actions across allow, step-up, block, alerts, and governed case workflows.

Step 7: Review, Measure, and Improve the Framework

A fraud risk management framework should improve as fraud patterns change. That only happens when teams measure both fraud outcomes and control performance.

Track metrics such as:

Fraud loss rate

Fraud prevented before loss

False positive rate

False negative rate

Manual review rate

Alert-to-action time

Onboarding pass rate

Chargeback or dispute rate

Repeat offender rate

Customer friction caused by fraud checks

Measurement should include both losses and prevented losses. UK Finance reported £1.17 billion stolen through authorized and unauthorized fraud in 2024, while banks prevented £1.45 billion of unauthorized fraud through security systems. That distinction helps teams evaluate whether controls are reducing exposure before losses materialize.

Review the framework after product launches, market expansion, major fraud incidents, regulatory changes, or sudden spikes in suspicious activity.

A Template to Conduct a Fraud Risk Assessment

A fraud risk assessment helps your teams move from assumptions to a clear view of organizational exposure. The primary objective is to catalog the most relevant fraud scenarios, score their prospective risk levels, review existing controls, and isolate the exact gaps that require architectural change.

The following fraud risk assessment matrix provides a condensed, high-level structural template to track core vulnerabilities across your platform:

Fraud Risk Scenario | Journey Stage | Risk Level | Existing Controls | Core Control Gap |

Synthetic Identity Fraud | Onboarding | High | Document Verification, KYC | Weak Device and Network Checks |

Account Takeover | Login & Account Changes | High | Password, MFA | Limited Behavioral and Device Monitoring |

Promo Abuse | Signup & Referral | Medium | Referral Limits | Repeat Devices Not Detected |

Chargeback Fraud | Payment Authorization & Transaction | High | Payment Review | Limited Pre-Transaction Risk Scoring |

Mule Account Activity | Onboarding & Transact | Critical | KYC, Transaction Rules | Weak Network Link Analysis |

Start with risks that affect revenue, compliance, customer trust, or workload. Score likelihood and impact as low, medium, or high. Prioritize high-impact risks with weak controls, then assign an owner and next action.

How Bureau ID Supports Fraud Risk Management

Bureau ID helps businesses strengthen fraud risk management by connecting identity, device, behavior, network, and transaction signals in one risk decisioning layer. The platform helps risk teams evaluate the full context behind each user action, from onboarding and login to transactions, account activity, and reviews.

Its role is especially relevant for high-risk digital businesses that face synthetic identity fraud, account takeover, mule activity, chargeback fraud, promo abuse, bot attacks, and repeat abuse across the customer lifecycle.

Bureau ID supports this through:

Device ID: Identifies suspicious devices, spoofed environments, emulators, VPN usage, repeat offenders, and device-account relationships.

Identity Document Verification: Validates user authenticity through document checks, biometric matching, liveness detection, and onboarding risk checks.

Behavioral Biometrics: Looks at how users interact with devices to spot bots, scripted behavior, fraud farms, impersonation, and suspicious sessions.

Alternate Data: Adds more context to user and transaction trust using digital footprint, email quality, phone intelligence, and other risk indicators.

Configurable Workflows: Risk teams can configure rules, thresholds, review flows, and step-up actions without depending on engineering for every change.

Explainable Decisions: Fraud investigators get context behind risk scores, which helps with investigations, audit trails, compliance reviews, and control tuning.

For fraud and risk teams, this means moving from isolated checks to a connected view of risk. Teams can see how identity, device, behavior, network, and transaction signals interact in real time.

Case Study: How Bureau ID Helped a PropTech Company Prevent $1.25M in Chargeback Fraud

A leading PropTech company was facing chargeback fraud on credit card rent payments. The challenge was to stop high-risk transactions before payment without disrupting legitimate renters or damaging the smooth payment experience.

The company implemented Bureau’s alternate data, custom risk models, and real-time decisioning to assess user and transaction risk before payment. Bureau ID evaluated 200+ live signals, including telco metadata, UPI integrity, email quality, identity consistency, transaction attributes, and digital footprint.

In three months, the company was able to:

Prevent $1.25M in chargeback fraud.

Reduce false chargeback rates from 40% to 8%.

Stop 1,200+ high-risk transactions before payment.

Flag 60,000+ users as high-risk for chargeback fraud.

Restrict credit card rent payments for risky users.

Read the full case study here → A Leading PropTech Saves $1.25M in Chargeback Fraud

A simple takeaway from this case study is that fraud risk management works best when risk decisions happen before losses occur. Businesses that connect identity, device, behavior, network, and transaction signals can reduce exposure while keeping trusted users moving.

Build a Stronger Fraud Risk Management Program

The most dangerous fraud pattern is often the one that looks legitimate until signals connect across the customer lifecycle.

As fraud moves across onboarding, login, payments, refunds, promotions, and ongoing account activity, the next step is to evaluate whether your controls work together or operate in silos.

By connecting identity, device, behavior, network, and transaction signals in a single decisioning layer, Bureau ID helps teams detect fraud earlier and respond with more precision. That means fewer broad rules, fewer unnecessary reviews, and stronger controls where the risk is real.

If you want to see how unified risk decisioning can help your team strengthen controls, reduce false positives, and adapt faster, book a demo with Bureau ID today.

FAQs

1. What is the main purpose of fraud risk management?

Fraud risk management helps organizations identify where fraud can occur, assess how serious the risk is, and apply the right controls. Its goal is to reduce losses, protect customers, and respond faster when suspicious activity appears.

2. What are the 5 principles of fraud risk management?

The five principles are fraud governance, risk assessment, prevention, detection, and response. Together, they help organizations define ownership, understand exposure, set controls, monitor suspicious activity, and improve the program as fraud patterns change.

3. How is fraud risk management different from fraud detection?

Fraud detection focuses on identifying suspicious activity. Fraud risk management is broader. It includes governance, risk assessment, internal controls, prevention, real-time transaction monitoring, pre-transaction risk evaluation, investigation, response, reporting, and continuous improvement across the organization.

4. How often should an organization assess fraud risk?

Organizations should assess fraud risk at least once a year. High-risk businesses should also reassess after product launches, market expansion, regulatory changes, major fraud incidents, or sudden increases in chargebacks, fake accounts, or suspicious transactions.

5. What are common fraud risks for digital businesses?

Common fraud risks include synthetic identity fraud, account takeover, promo abuse, chargeback fraud, bot attacks, mule accounts, fake profiles, and transaction fraud. These risks often appear across onboarding, login, payment, referral, refund, and monitoring workflows.

6. What should a fraud risk management framework include?

A fraud risk management framework should include clear ownership, fraud risk assessment, preventive controls, detection systems, response workflows, reporting processes, and performance metrics. It should also be updated regularly as fraud tactics and business risks evolve.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.