How Secure Digital Payments Are Expanding Financial Inclusion Globally

How Secure Digital Payments Are Expanding Financial Inclusion Globally

How Secure Digital Payments Are Expanding Financial Inclusion Globally

RBI's new directions validate Bureau vision of adaptive, risk-based digital payment authentication driving safer digital transactions, greater financial.

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

Every day millions of Indians use digital payments to pay bills, transfer funds, or shop online. These transactions are made possible by a complex web of authentication systems that work behind the scenes, protecting users from fraud and theft. However, Indian users lost about INR 1,087 crore (approx $123 million) during FY 2023-24 and have already lost INR 485 crore (nearly $55 million) by September 2025 to UPI-related fraud alone.

Considering the evolving threat landscape – replete with the risks of phishing, account takeovers, and fraud attempts – the Reserve Bank of India (RBI) has issued directions on digital payment authentication to make every transaction safer. The directions mandate adoption of flexible, technology-agnostic, and risk-based authentication methods to strengthen transaction security, build user trust, and accelerate the adoption of formal digital financial services.

The RBI’s latest directions are a validation of Bureau’s long-standing vision of building products that enable issuers, financial institutions, and payment service providers to move beyond static defense methods and adopt a more unified approach to fraud prevention, strengthening trust without disrupting user experience.

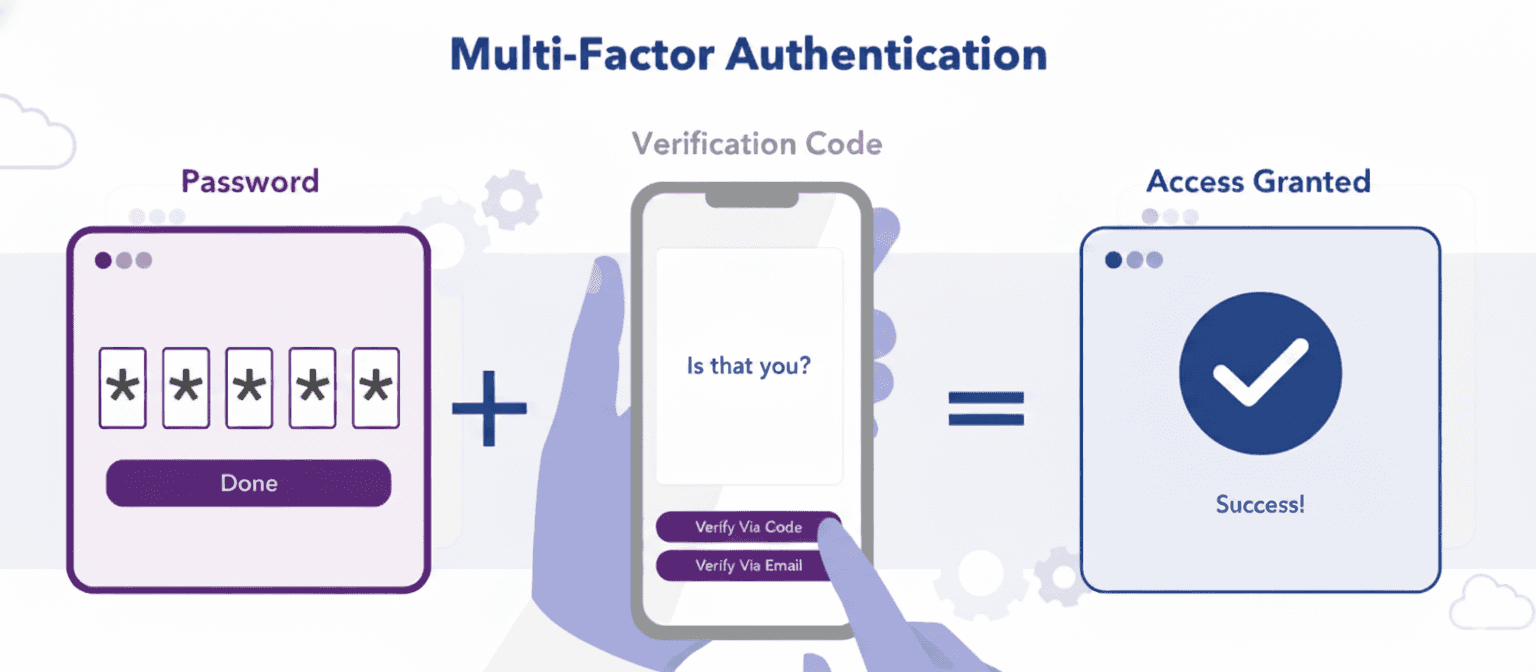

The shift beyond OTPs

For years, SMS-based one-time passwords (OTPs) have served as the primary second factor for authenticating digital transactions in India. Although still being used widely, OTPs are increasingly vulnerable to interception, phishing, and social engineering.

The RBI’s new directions address these vulnerabilities by encouraging the adoption of advanced factors such as:

Biometrics: Fingerprint, facial recognition, or voice as direct and secure identity signals.

Device identity: Binding transactions to trusted devices to reduce compromise risks.

Behavioral signals: Recognizing unique user interaction patterns for silent authentication.

Risk-based authentication: Adapting checks in real-time based on transaction value, context, and anomalies.

This shift from static to adaptive authentication aligns closely with Bureau’s approach, as its unified risk-based decisioning platform integrates device, behavioral, and contextual intelligence to proactively deter fraud, step up verification checks when risk profile changes, and strengthen user trust.

Building trust and expanding access

Beyond securing digital payments, the RBI’s directions will have a larger impact on financial inclusion and access to credit. Many first-time users, particularly in semi-urban and rural areas, remain hesitant about adopting digital payments due to security concerns. By moving beyond the one-size-fits-all approach, financial institutions will be able to verify each user according to their unique risk profiles and establish trust at every stage of the customer journey.

This shift from a single point of failure to real-time risk-based decisioning will result in:

Greater confidence: In everyday transactions such as fund transfers, bill payments, and merchant purchases.

Establishing trust: Among users who feel safe transacting digitally for the first time.

Financial inclusion: Secure digital transactions encourage adoption of formal financial channels.

Credit access: With the ability to offer custom credit limits and products, based on a user’s risk profile.

Implementing these measures, however, will require operational readiness, which businesses must prioritize.

Operational implications for financial institutions

While the directions provide clear guidance, financial institutions and fintechs will need to make strategic adjustments to align with them. Experts believe that to implement the RBI’s vision, businesses will need to “strengthen two-factor authentication with biometrics, passkeys, and AI-driven risk-based authentication, while ensuring interoperability and accessibility across applications.”

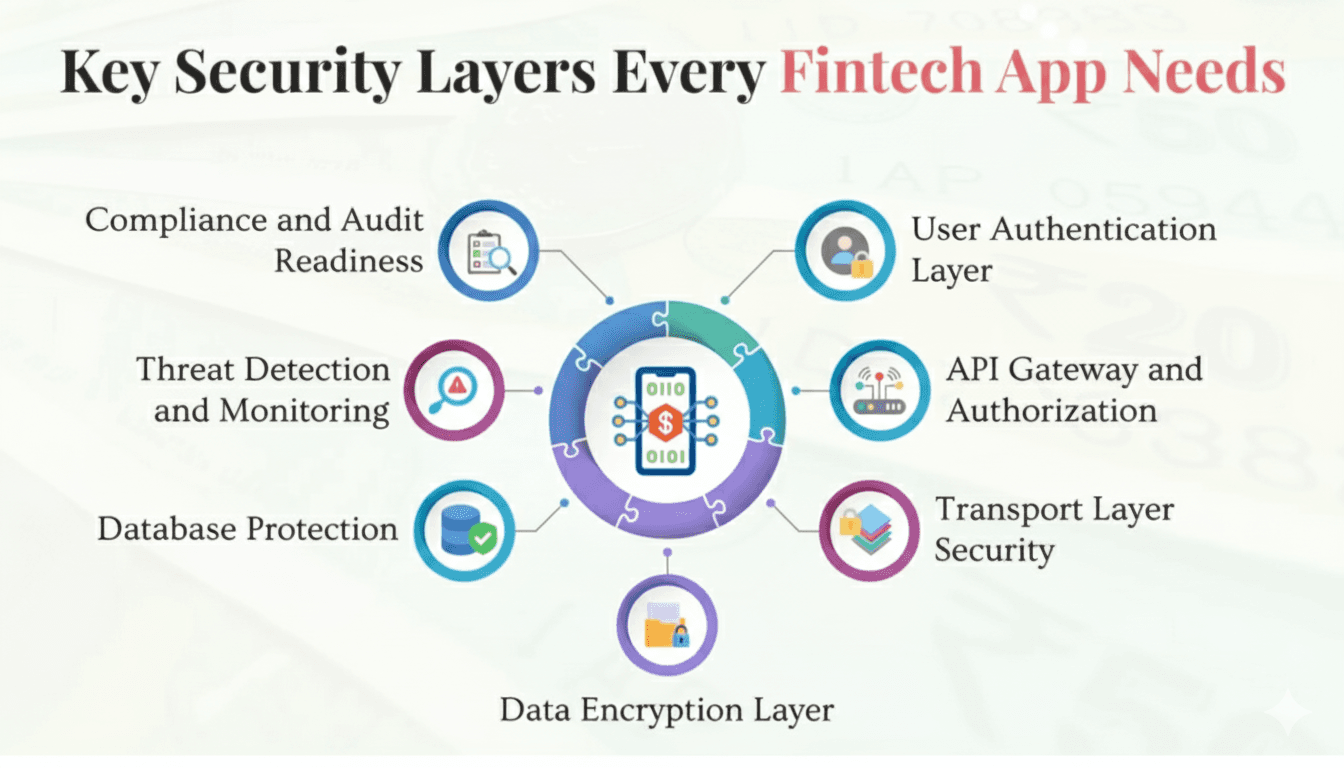

To meet the operational needs and gain real-time decisioning, they will need advanced technology and techniques that not only strengthen authentication but also preserve seamless user experience. Key considerations include:

Technology upgrades: Deploying biometrics, device fingerprinting, and behavioral authentication at scale.

Risk-based models: Adaptive authentication will require real-time decisioning capabilities to ensure friction is applied only when needed.

User experience: Not compromising usability while catering to diverse user bases, from advanced smartphone users to feature phone users.

Fraud intelligence: Using integrated systems, such as Bureau’s unified risk decisioning platform, that combine authentication with fraud detection and identity decisioning.

A global benchmark in the making

Driven by the success of platforms like UPI, India is already a global leader in digital transaction volumes. With these new authentication directions, India has an opportunity to set a global benchmark for secure, scalable, and inclusive payment authentication. India can play a pioneering role in:

Cross-border safety: While applicable only to domestic transactions, these directions also provide guidance for international card payments from India and specific cross-border card transactions, in line with the Statement on Developmental and Regulatory Policies of February 2025, to ensure a similar level of safety for cross-border payments.

Emerging markets: Countries in Asia, Africa, and Latin America face similar challenges in securing digital payments for a rapidly digitizing population without creating barriers to adoption. If implemented effectively, India’s model of multi-factor, risk-based, and technology-agnostic authentication could serve as a blueprint for these regions.

Global adoption: By demonstrating secure scalable systems that balance security with friction, Indian regulators and financial institutions can shape next-generation authentication standards.

Fintech experts believe that the RBI’s directions “align with global best practices and will strengthen India's position in the international digital payments landscape. The move will foster a more robust and compliant ecosystem, ensuring smoother and more secure cross-border transactions for all.”

Bureau’s approach to strengthening payment security

Bureau has long advocated the principles underlying the RBI’s new authentication directions. By providing the tools and intelligence needed to implement adaptive, scalable, and secure authentication systems, Bureau has been supporting financial institutions to secure digital payments, build trust in formal financial channels, and support accessibility for first-time digital users.

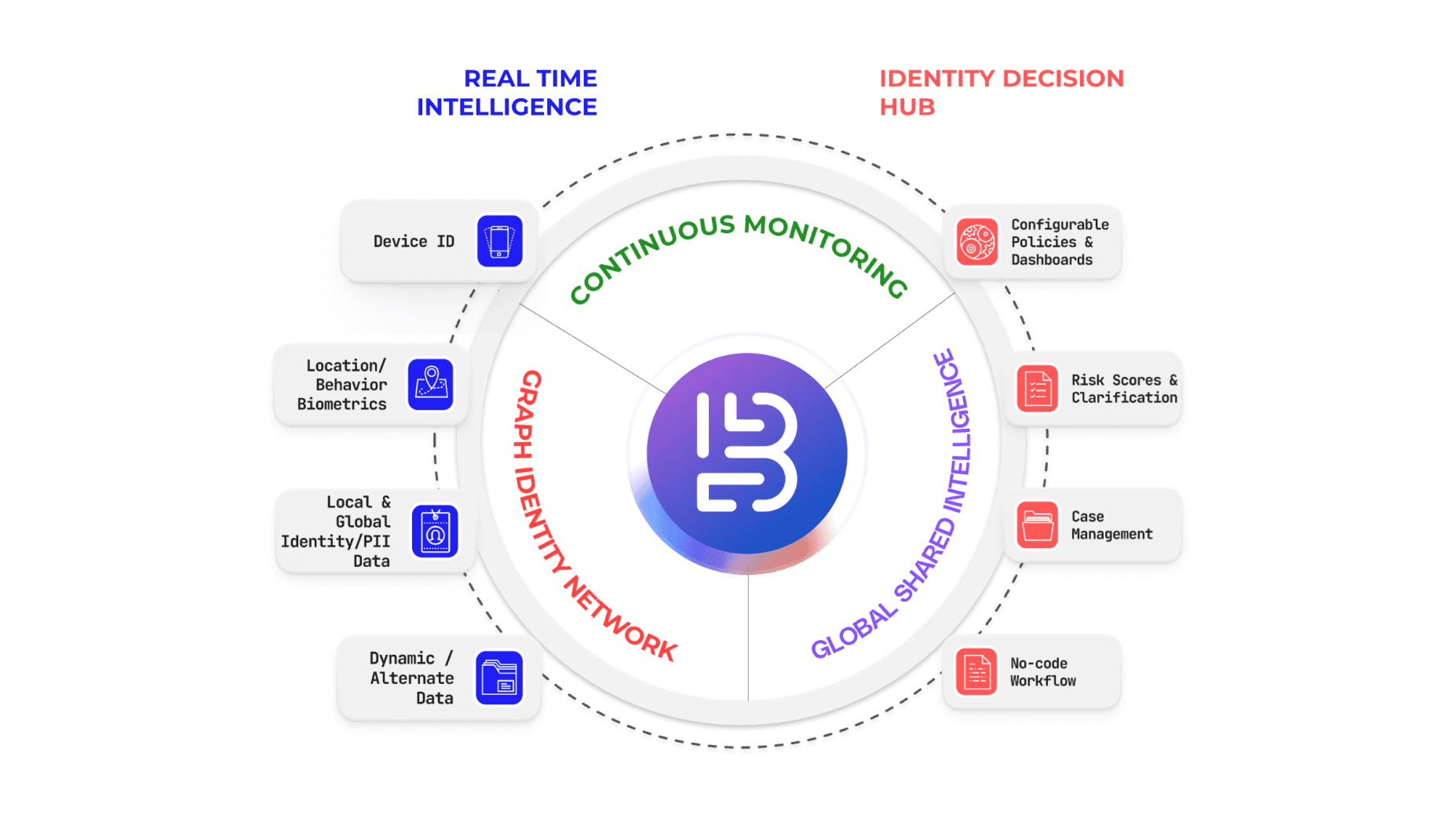

With its unified risk decisioning platform, Bureau delivers:

Multi-layered authentication using device intelligence, behavioral biometrics, and other digital insights.

Risk-based decisioning using contextual assessment of each transaction and stepping up authentication, only when needed.

Interoperability and inclusion by ensuring authentication works across different devices, channels, and connectivity levels.

Real-time fraud detection and identity decisioning for end-to-end protection across the customer journey.

Conclusion

The future of authentication is multi-layered, adaptive, and inclusive. The RBI’s authentication directions represent this pivotal shift in India’s digital payments landscape. They set forth a forward-looking framework with multi-factor, risk-based authentication that balances security with usability, inclusion, and accessibility.

For India, this is more than a regulatory change, it is an opportunity to redefine global benchmarks for digital payment security. For financial institutions, it is both a challenge and an opportunity to modernize their authentication systems, enhance trust, and expand access to digital payments and credit.

Bureau’s vision aligns with this new mandate, as it continues to empower financial institutions to secure digital transactions at scale, build user trust, and drive financial inclusion through its advanced and adaptive authentication solutions.

Every day millions of Indians use digital payments to pay bills, transfer funds, or shop online. These transactions are made possible by a complex web of authentication systems that work behind the scenes, protecting users from fraud and theft. However, Indian users lost about INR 1,087 crore (approx $123 million) during FY 2023-24 and have already lost INR 485 crore (nearly $55 million) by September 2025 to UPI-related fraud alone.

Considering the evolving threat landscape – replete with the risks of phishing, account takeovers, and fraud attempts – the Reserve Bank of India (RBI) has issued directions on digital payment authentication to make every transaction safer. The directions mandate adoption of flexible, technology-agnostic, and risk-based authentication methods to strengthen transaction security, build user trust, and accelerate the adoption of formal digital financial services.

The RBI’s latest directions are a validation of Bureau’s long-standing vision of building products that enable issuers, financial institutions, and payment service providers to move beyond static defense methods and adopt a more unified approach to fraud prevention, strengthening trust without disrupting user experience.

The shift beyond OTPs

For years, SMS-based one-time passwords (OTPs) have served as the primary second factor for authenticating digital transactions in India. Although still being used widely, OTPs are increasingly vulnerable to interception, phishing, and social engineering.

The RBI’s new directions address these vulnerabilities by encouraging the adoption of advanced factors such as:

Biometrics: Fingerprint, facial recognition, or voice as direct and secure identity signals.

Device identity: Binding transactions to trusted devices to reduce compromise risks.

Behavioral signals: Recognizing unique user interaction patterns for silent authentication.

Risk-based authentication: Adapting checks in real-time based on transaction value, context, and anomalies.

This shift from static to adaptive authentication aligns closely with Bureau’s approach, as its unified risk-based decisioning platform integrates device, behavioral, and contextual intelligence to proactively deter fraud, step up verification checks when risk profile changes, and strengthen user trust.

Building trust and expanding access

Beyond securing digital payments, the RBI’s directions will have a larger impact on financial inclusion and access to credit. Many first-time users, particularly in semi-urban and rural areas, remain hesitant about adopting digital payments due to security concerns. By moving beyond the one-size-fits-all approach, financial institutions will be able to verify each user according to their unique risk profiles and establish trust at every stage of the customer journey.

This shift from a single point of failure to real-time risk-based decisioning will result in:

Greater confidence: In everyday transactions such as fund transfers, bill payments, and merchant purchases.

Establishing trust: Among users who feel safe transacting digitally for the first time.

Financial inclusion: Secure digital transactions encourage adoption of formal financial channels.

Credit access: With the ability to offer custom credit limits and products, based on a user’s risk profile.

Implementing these measures, however, will require operational readiness, which businesses must prioritize.

Operational implications for financial institutions

While the directions provide clear guidance, financial institutions and fintechs will need to make strategic adjustments to align with them. Experts believe that to implement the RBI’s vision, businesses will need to “strengthen two-factor authentication with biometrics, passkeys, and AI-driven risk-based authentication, while ensuring interoperability and accessibility across applications.”

To meet the operational needs and gain real-time decisioning, they will need advanced technology and techniques that not only strengthen authentication but also preserve seamless user experience. Key considerations include:

Technology upgrades: Deploying biometrics, device fingerprinting, and behavioral authentication at scale.

Risk-based models: Adaptive authentication will require real-time decisioning capabilities to ensure friction is applied only when needed.

User experience: Not compromising usability while catering to diverse user bases, from advanced smartphone users to feature phone users.

Fraud intelligence: Using integrated systems, such as Bureau’s unified risk decisioning platform, that combine authentication with fraud detection and identity decisioning.

A global benchmark in the making

Driven by the success of platforms like UPI, India is already a global leader in digital transaction volumes. With these new authentication directions, India has an opportunity to set a global benchmark for secure, scalable, and inclusive payment authentication. India can play a pioneering role in:

Cross-border safety: While applicable only to domestic transactions, these directions also provide guidance for international card payments from India and specific cross-border card transactions, in line with the Statement on Developmental and Regulatory Policies of February 2025, to ensure a similar level of safety for cross-border payments.

Emerging markets: Countries in Asia, Africa, and Latin America face similar challenges in securing digital payments for a rapidly digitizing population without creating barriers to adoption. If implemented effectively, India’s model of multi-factor, risk-based, and technology-agnostic authentication could serve as a blueprint for these regions.

Global adoption: By demonstrating secure scalable systems that balance security with friction, Indian regulators and financial institutions can shape next-generation authentication standards.

Fintech experts believe that the RBI’s directions “align with global best practices and will strengthen India's position in the international digital payments landscape. The move will foster a more robust and compliant ecosystem, ensuring smoother and more secure cross-border transactions for all.”

Bureau’s approach to strengthening payment security

Bureau has long advocated the principles underlying the RBI’s new authentication directions. By providing the tools and intelligence needed to implement adaptive, scalable, and secure authentication systems, Bureau has been supporting financial institutions to secure digital payments, build trust in formal financial channels, and support accessibility for first-time digital users.

With its unified risk decisioning platform, Bureau delivers:

Multi-layered authentication using device intelligence, behavioral biometrics, and other digital insights.

Risk-based decisioning using contextual assessment of each transaction and stepping up authentication, only when needed.

Interoperability and inclusion by ensuring authentication works across different devices, channels, and connectivity levels.

Real-time fraud detection and identity decisioning for end-to-end protection across the customer journey.

Conclusion

The future of authentication is multi-layered, adaptive, and inclusive. The RBI’s authentication directions represent this pivotal shift in India’s digital payments landscape. They set forth a forward-looking framework with multi-factor, risk-based authentication that balances security with usability, inclusion, and accessibility.

For India, this is more than a regulatory change, it is an opportunity to redefine global benchmarks for digital payment security. For financial institutions, it is both a challenge and an opportunity to modernize their authentication systems, enhance trust, and expand access to digital payments and credit.

Bureau’s vision aligns with this new mandate, as it continues to empower financial institutions to secure digital transactions at scale, build user trust, and drive financial inclusion through its advanced and adaptive authentication solutions.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.