6 Best BioCatch Alternatives Compared for Modern Fraud Prevention

6 Best BioCatch Alternatives Compared for Modern Fraud Prevention

6 Best BioCatch Alternatives Compared for Modern Fraud Prevention

Compare BioCatch competitors, including Bureau ID, SHIELD, Feedzai, SEON, Sift, and ThreatMetrix, to find the best fraud prevention platform.

Author

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

BioCatch is one of the most widely evaluated platforms for behavioral biometrics, particularly among banks, fintechs, and other digital businesses.

But as fraud expands beyond individual sessions, many buyers begin researching BioCatch competitors that can also support identity verification, device intelligence, transaction monitoring, account opening protection, anti-money laundering identification, and broader fraud decisioning across the customer lifecycle.

To make this comparison useful, we evaluated 6 platforms by the fraud problems they solve, the signals they use, and the workflows they fit best.

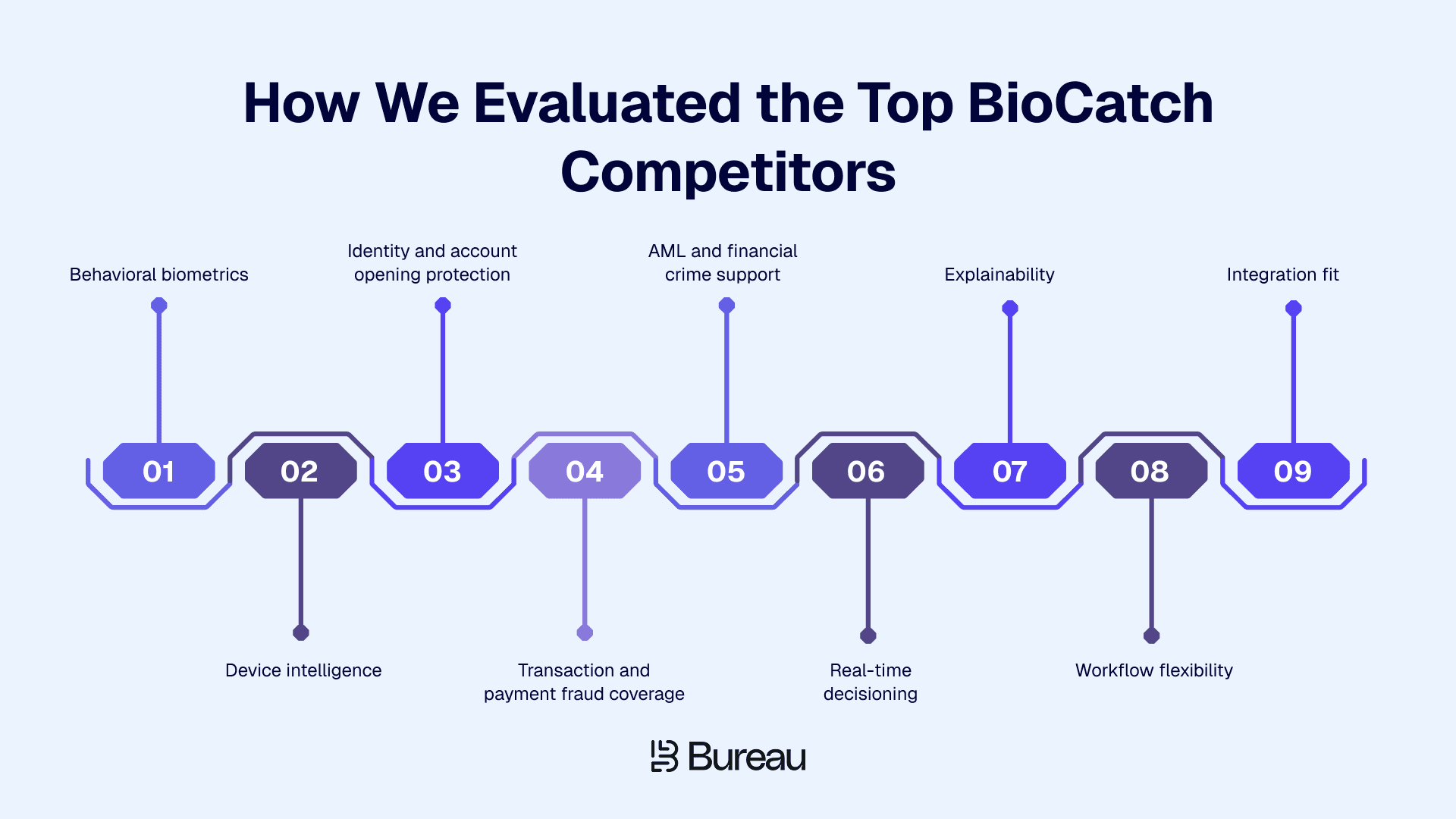

How We Evaluated the Top BioCatch Competitors

For comparing BioCatch competitors effectively, it's necessary to understand how each platform contributes across the fraud lifecycle.

Factors like whether it can connect behavioral signals with device intelligence, identity data, and transaction context to catch fraud early, adapt to evolving attack patterns, and support fast, confident decisions without disrupting genuine users should be considered.

To make the comparison practical, we evaluated every platform using the criteria below.

Behavioral biometrics: Analysis of typing rhythm, mouse movement, touchscreen gestures, device handling, and session behavior to distinguish genuine users from fraudsters.

Device intelligence: Detection of spoofed devices, emulators, VPNs, device resets, bots, browser manipulation, and repeat device usage.

Identity and account opening protection: Coverage for fake accounts, synthetic identities, mule accounts, and onboarding fraud.

Transaction and payment fraud coverage: Support for payment fraud, withdrawals, beneficiary changes, transfers, chargebacks, and suspicious fund movement.

AML and financial crime support: Capabilities for anti-money laundering identification, transaction monitoring, mule detection, audit trails, sanctions workflows, and investigations.

Real-time decisioning: Risk scoring across onboarding, login, account recovery, transactions, and ongoing activity.

Explainability: Clear risk signals and contextual explanations for flagged actions.

Workflow flexibility: Ability to configure rules, thresholds, step-up actions, and review workflows without heavy engineering effort.

Integration fit: APIs, SDKs, webhooks, and seamless integration into existing fraud, risk, and compliance stacks.

Bureau ID's 2026 India Fraud Report found that 58% of organizations identified decision errors as their dominant identity risk, highlighting why many buyers are moving beyond isolated behavioral signals toward platforms that evaluate identity, device, behavioral, and transaction intelligence together.

With these criteria in mind, compare leading BioCatch alternatives side by side to highlight where each platform stands and how they differ in real-world fraud prevention scenarios.

Top 6 BioCatch Competitors and Alternatives

The top BioCatch competitors include Bureau ID, SHIELD, LexisNexis ThreatMetrix, Feedzai, SEON, and Sift.

These BioCatch alternatives address different fraud prevention priorities, from behavioral biometrics and device intelligence to digital identity, account opening protection, transaction monitoring, AML risk, and unified fraud decisioning across the customer lifecycle.

Tool | Best For | Core Strength | Key Consideration |

Bureau ID | Unified fraud risk decisioning | Identity, device, behavior, network, and transaction intelligence | Best fit when teams want broader lifecycle coverage instead of point tools |

SHIELD | Device intelligence and multi-accounting prevention | Device fingerprinting, device risk, emulator detection, fake account detection | Strong when device manipulation, repeated signups, promo abuse, or multi-accounting are major fraud patterns |

LexisNexis ThreatMetrix | Digital identity intelligence | Device, identity, network, and risk signals | Better fit for enterprise risk stacks and digital identity use cases |

Feedzai | Enterprise fraud and financial crime prevention | Transaction fraud, scam detection, and risk operations | Best suited for large financial institutions and payment-heavy workflows |

SEON | Fraud checks and AML enrichment | Email, phone, IP, device, digital footprint, and AML signals | Strong when enrichment and fast fraud checks are the priority |

Sift | Digital fraud prevention | Account abuse, payment fraud, account takeover, and dispute workflows | Strong for marketplaces, ecommerce, subscription businesses, and digital platforms |

These six platforms were selected because they consistently appear across buyer research, analyst reports, review sites, and competitive searches for companies like BioCatch.

While some focus primarily on behavioral biometrics or device intelligence, others extend into digital identity, financial crime prevention, fraud orchestration, or broader anti-fraud solutions.

Below, we break down each BioCatch alternative by what it does, when buyers choose it, what to consider, best-fit use cases, and pricing expectations.

1. Bureau ID

Bureau ID is an AI-powered Unified Risk Decisioning Platform that helps businesses make fraud decisions across onboarding, authentication, transactions, and ongoing account activity. It brings multiple fraud signals together into a single decisioning layer to support more consistent and efficient risk decisions.

Bureau ID is used to protect businesses across the entire customer lifecycle, including onboarding, authentication, transactions, and ongoing account activity.

When buyers choose Bureau ID over BioCatch:

Organizations typically evaluate Bureau ID when behavioral biometrics alone is not enough to address the fraud challenges they face. Instead of focusing primarily on user behavior during a session, Bureau combines identity, device, behavioral, network, and transaction signals to deliver explainable risk decisions throughout the customer lifecycle.

Buyers commonly choose Bureau ID when they need to:

Protect onboarding, login, transactions, and ongoing account activity within one platform.

Detect synthetic identities, repeat devices, mule networks, and connected fraud rings using relationship-based intelligence.

Configure fraud workflows, approval rules, and step-up verification without extensive engineering effort.

Reduce fraud while minimizing false positives and unnecessary friction for legitimate users.

Key strengths:

Unified risk decisioning: Enables consistent fraud detection and decision-making across onboarding, authentication, transactions, and ongoing account activity.

Device intelligence and behavioral biometrics: Helps identify trusted and risky devices over time, even when fraudsters attempt to evade detection.

Graph identity network: Connects identities, devices, behaviors, and transactions to reveal coordinated fraud rings and mule networks that may not be visible through isolated signals.

Mule detection and AML support: Provides scoring and workflows that assist with identifying mule accounts and supporting financial crime investigations.

Explainable real-time decisions: Delivers transparent risk assessments that help analysts understand why users, devices, or transactions are flagged.

Configurable workflows: Allows teams to adapt fraud rules and decision logic using no-code and low-code tools, reducing reliance on engineering resources.

A good example of this broader approach comes from a leading insurer that improved onboarding efficiency while reducing fraudulent applications.

How Bureau ID helped a leading insurer improve onboarding and reduce fraud

A leading insurer was facing high levels of fraudulent applications during onboarding, which forced them to introduce stricter checks that slowed down legitimate customers. They needed a way to balance fraud prevention with a smoother onboarding experience.

Bureau ID helped by combining identity verification with device and behavioral intelligence within a unified decisioning workflow, allowing the insurer to detect risky applications more accurately while reducing friction for genuine users.

Results achieved:

30% faster onboarding for legitimate customers

Significant reduction in fraudulent applications

Improved approval rates without increasing risk

Read the full case study here → Insurer Cuts Fraud for 30% Faster Onboarding

Things to consider:

Designed for organizations consolidating fraud prevention across onboarding, authentication, transactions, and ongoing account activity rather than deploying a standalone behavioral biometrics solution.

Delivers the most value when buyers clearly map the workflows they want to unify across the customer journey before implementation.

Pricing: Platform-based custom pricing based on modules, use cases, and transaction volume.

2. SHIELD

SHIELD is a device-first fraud intelligence platform that helps businesses identify risky devices before fraud occurs. It specializes in persistent device identification, fake account detection, multi-accounting prevention, and bot mitigation, making it a strong BioCatch alternative for organizations that want deeper device intelligence across mobile and web environments.

When buyers choose SHIELD over BioCatch:

Organizations often evaluate SHIELD when device manipulation is a larger fraud challenge than session behavior alone. Buyers commonly choose SHIELD when they need to:

Detect fake accounts, repeat devices, and multi-accounting before they impact onboarding or promotions.

Identify fraudsters using emulators, cloned apps, VPNs, factory resets, or other device evasion techniques.

Reduce promo abuse, referral fraud, and bot-driven attacks through device-level intelligence.

Key strengths:

Stops fraud before accounts are created: Persistent device identification helps expose risky devices before onboarding, payments, or KYC checks are completed.

Detects sophisticated device manipulation: Identifies emulators, cloned apps, device tampering, VPN usage, and other techniques commonly used to evade detection.

Reduces multi-account abuse: Connects repeat devices across accounts to uncover referral abuse, fake accounts, and coordinated fraud activity.

Supports real-time fraud decisions: Delivers device risk signals with low latency so teams can act during onboarding, login, or payment flows.

Integrates quickly across digital channels: SDKs and APIs support deployment across web, Android, iOS, and other environments with centralized monitoring.

Things to consider:

Organizations may still require complementary solutions for identity verification, AML workflows, transaction monitoring, or broader fraud orchestration.

Some reviewers note that advanced integrations and custom configurations can require technical expertise, particularly for teams without dedicated engineering resources.

Pricing: Custom pricing based on use case, deployment scope, and transaction volume.

3. LexisNexis ThreatMetrix

LexisNexis ThreatMetrix is a digital identity intelligence platform that helps businesses assess trust using device, identity, network, and behavioral signals. It is a strong BioCatch alternative for organizations that need broader digital identity intelligence and enterprise-scale fraud prevention beyond behavioral biometrics alone.

When buyers choose LexisNexis ThreatMetrix over BioCatch:

Organizations typically evaluate ThreatMetrix when fraud decisions require more than session-level behavioral analysis. Buyers commonly choose the platform when they need to:

Build richer risk profiles using device, identity, location, and network intelligence.

Protect account opening, authentication, and payment journeys with connected digital identity signals.

Leverage enterprise-grade fraud intelligence across multiple business units or regions.

Key strengths:

Builds trusted digital identities: Connects identity, device, location, and network signals to evaluate user trust throughout the customer lifecycle.

Improves account opening protection: Detects suspicious identities and high-risk onboarding attempts before accounts are created.

Strengthens account takeover detection: Combines device reputation and behavioral risk signals to identify anomalous login activity.

Supports enterprise fraud operations: Integrates with large-scale fraud, compliance, and authentication ecosystems across financial institutions.

Enables cross-channel risk decisions: Applies consistent risk intelligence across web, mobile, and digital banking experiences.

Things to consider:

ThreatMetrix is designed primarily for enterprise organizations, so implementation effort and operational complexity may exceed the needs of smaller businesses.

Implementation and integration can require significant planning, particularly in complex enterprise environments.

Pricing: Enterprise custom pricing.

4. Feedzai

Feedzai is an enterprise financial crime prevention platform that helps banks and payment providers detect fraud across payments, transfers, and digital banking. It is a strong BioCatch alternative for organizations that prioritize transaction monitoring, scam detection, and AML workflows alongside fraud prevention.

When buyers choose Feedzai over BioCatch:

Organizations often evaluate Feedzai when fraud is concentrated around money movement rather than user sessions. Buyers commonly choose Feedzai when they need to:

Detect payment fraud, scams, and suspicious transactions in real time.

Combine fraud prevention with AML monitoring and financial crime investigations.

Support large-scale fraud operations across banking and payment ecosystems.

Key strengths:

Detects payment fraud in real time: Uses AI and machine learning to identify suspicious transactions before funds leave the institution.

Strengthens financial crime operations: Combines fraud detection with AML monitoring, scam prevention, and investigation workflows.

Supports enterprise-scale decisioning: Processes high transaction volumes across banks, payment processors, and financial institutions.

Improves analyst efficiency: Provides case management and investigation tools that help fraud teams prioritize high-risk events.

Adapts to evolving fraud patterns: Machine learning models continuously evaluate new fraud behaviors instead of relying solely on static rules.

Things to consider:

Feedzai is designed primarily for enterprise financial institutions, so it may offer more functionality than smaller fintechs or digital businesses require.

Implementation can be time-consuming because the platform requires careful model configuration and integration with existing banking systems.

Pricing: Enterprise custom pricing.

5. SEON

SEON is a fraud prevention platform that combines digital footprint analysis, device intelligence, identity enrichment, and AML capabilities to assess user risk. It is a strong BioCatch alternative for organizations looking for fast fraud screening across onboarding, payments, and account activity without relying primarily on behavioral biometrics.

When buyers choose SEON over BioCatch:

Organizations often evaluate SEON when they want broader identity enrichment alongside fraud detection. Buyers commonly choose SEON when they need to:

Verify users using email, phone, IP, device, and digital footprint intelligence.

Add AML screening and fraud scoring within the same workflow.

Deploy flexible fraud checks across fintech, ecommerce, gaming, crypto, or marketplace platforms.

Key strengths:

Enriches user profiles instantly: Combines email, phone, IP, device, and digital footprint signals to build a more complete risk profile.

Reduces onboarding fraud: Identifies suspicious accounts before they progress through verification or payment flows.

Supports AML and compliance workflows: Integrates AML screening alongside fraud scoring to simplify risk assessments.

Provides flexible risk controls: Enables teams to configure fraud rules, risk thresholds, and decision logic without extensive development work.

Deploys quickly across digital channels: API-first architecture helps businesses integrate fraud checks into existing customer journeys with minimal disruption.

Things to consider:

SEON focuses on enrichment and fraud intelligence rather than dedicated behavioral biometrics, so organizations with advanced session-level fraud requirements may need complementary technologies.

Some users note that investigation workflows would benefit from stronger case management capabilities.

Pricing: Usage-based pricing with custom enterprise plans available.

6. Sift

Sift is a digital fraud prevention platform that helps businesses detect account abuse, payment fraud, account takeover, and policy abuse across the customer lifecycle. It is a strong BioCatch alternative for marketplaces, ecommerce companies, and subscription businesses that need fraud protection beyond behavioral biometrics.

When buyers choose Sift over BioCatch:

Organizations often evaluate Sift when fraud extends beyond authentication into payments, disputes, and account abuse. Buyers commonly choose Sift when they need to:

Detect account takeover, fake accounts, and payment fraud from a unified platform.

Protect marketplaces, subscription businesses, and digital communities from policy abuse and chargebacks.

Connect fraud decisions across user behavior, account activity, and transaction risk.

Key strengths:

Protects the entire customer journey: Helps detect fraud across onboarding, account activity, payments, disputes, and trust and safety workflows.

Reduces account abuse: Identifies fake accounts, account takeover attempts, promo abuse, and other forms of platform abuse before they scale.

Improves payment fraud detection: Combines machine learning with behavioral and transaction signals to identify high-risk payments in real time.

Supports trust and safety teams: Provides case management, automation, and investigation tools for fraud operations at scale.

Integrates into growing digital platforms: Flexible APIs enable deployment across marketplaces, ecommerce, subscription services, and online communities.

Things to consider:

Sift is designed as a broad digital fraud prevention platform rather than a dedicated behavioral biometrics solution, so organizations requiring deep behavioral analytics may need complementary capabilities.

Some reviewers mention that investigation workflows could be improved with stronger case management capabilities, such as note-taking and grouping related device activity for complex fraud investigations.

Pricing: Custom pricing based on business size, use case, and transaction volume.

Which BioCatch Alternative Is Right for Your Use Case?

The best BioCatch alternative depends on where fraud occurs in your customer journey. For instance:

A bank dealing with account takeover and scam activity may prioritize behavioral biometrics and digital identity intelligence.

A fintech fighting synthetic identities and mule accounts may need stronger identity, device, and network intelligence.

Meanwhile, ecommerce businesses and marketplaces often focus on account abuse, payment fraud, promo abuse, and chargebacks.

According to the INTERPOL 2026 Global Financial Fraud Threat Assessment, AI-enhanced financial fraud is now 4.5 times more profitable than traditional methods, and financial fraud has entered the top 5 global crime threats.

Before shortlisting a platform, take a quick, structured approach to understand your needs and avoid mismatches.

Map where fraud occurs across your lifecycle, from onboarding and login to transactions, withdrawals, and ongoing monitoring.

Identify the key signal gap you need to address, such as behavioral, device, identity, transaction, AML, network, or workflow intelligence.

Evaluate operational fit, including explainability, case management, rules, step-up flows, and implementation complexity.

Test each platform against your real fraud scenarios, false positives, and genuine user behavior before making a decision.

BioCatch Alternatives by Use Case

Use Case or Priority | Best-Fit Tools |

Need unified risk decisioning across onboarding, login, transactions, and monitoring | Bureau ID, LexisNexis ThreatMetrix, Feedzai |

Need behavioral biometrics and session-level fraud detection | Bureau ID, LexisNexis ThreatMetrix |

Need device intelligence, repeat device detection, and multi-accounting protection | Bureau ID, SHIELD, SEON |

Need account opening protection and synthetic identity detection | Bureau ID, LexisNexis ThreatMetrix, SEON |

Need transaction fraud, scam detection, and financial crime workflows | Feedzai, Bureau ID, LexisNexis ThreatMetrix |

Need enrichment-led fraud checks across email, phone, IP, and device | SEON, Sift |

Need account abuse, payment fraud, and marketplace or ecommerce fraud protection | Sift, SEON, Bureau ID |

Need AML-adjacent signals, mule risk, and compliance-heavy review support | Bureau ID, Feedzai, SEON |

For many of Bureau ID's core customers, fraud is rarely confined to a single event. Banks, fintechs, lenders, marketplaces, gaming companies, payment providers, and ecommerce platforms often need to evaluate trust across multiple stages of the customer journey rather than at a single checkpoint.

Bureau ID is a strong fit for organizations that want to combine device intelligence, behavioral biometrics, identity verification, network intelligence, transaction monitoring, and configurable fraud workflows within a unified risk decisioning platform instead of managing separate point solutions.

Stop Fraud Across the Entire Customer Journey

The right BioCatch alternative is the one that aligns with where fraud occurs in your business.

If your biggest challenge is session-level fraud, a behavioral biometrics platform may be enough. But if fraud spans onboarding, authentication, account activity, transactions, mule networks, and manual review, a broader risk decisioning platform can provide better visibility and more consistent decisions.

Bureau ID brings identity, device, behavioral, network, and transaction intelligence together into a single decisioning layer, helping fraud, risk, compliance, and product teams detect connected fraud, reduce false positives, and protect the entire customer journey.

If you're curious how unified risk decisioning can strengthen your fraud prevention, onboarding, compliance, and transaction monitoring workflows, schedule a demo with Bureau ID today.

FAQs

1. Who are BioCatch's biggest competitors?

Some of the top BioCatch competitors include Bureau ID, SHIELD, LexisNexis ThreatMetrix, Feedzai, SEON, and Sift. Each platform focuses on different strengths, such as behavioral biometrics, device intelligence, digital identity, transaction monitoring, or unified fraud risk decisioning.

2. What is the best BioCatch alternative for banks and fintechs?

The best alternative depends on your fraud challenges. Banks and fintechs focused on account takeover may prioritize behavioral biometrics, while organizations dealing with onboarding fraud, mule accounts, and transaction risk often need broader platforms combining identity, device, network, and transaction intelligence.

3. How does Bureau ID compare to BioCatch?

Bureau ID and BioCatch both help detect fraud using behavioral signals, but Bureau ID extends beyond behavioral biometrics by combining identity, device, network, and transaction intelligence. This makes it well-suited for organizations seeking a more unified approach to fraud risk decisioning across the entire customer journey.

4. What should I compare when evaluating BioCatch alternatives?

Look beyond behavioral biometrics. Compare device intelligence, identity verification, account opening protection, transaction monitoring, AML capabilities, explainability, workflow flexibility, integrations, and how effectively each platform supports your fraud operations from onboarding through ongoing account activity.

5. Which BioCatch alternative is best for preventing account takeover?

If account takeover is primarily driven by abnormal user behavior, behavioral biometrics platforms may be sufficient. If attackers also exploit stolen devices, synthetic identities, or mule accounts, consider platforms that combine behavioral, device, identity, and transaction intelligence.

6. How do I choose the right BioCatch alternative for my business?

Start by identifying where fraud occurs in your customer journey and the signals you need to detect it. Then evaluate each platform using your own fraud scenarios, operational workflows, integration requirements, and false-positive tolerance before making a decision.

BioCatch is one of the most widely evaluated platforms for behavioral biometrics, particularly among banks, fintechs, and other digital businesses.

But as fraud expands beyond individual sessions, many buyers begin researching BioCatch competitors that can also support identity verification, device intelligence, transaction monitoring, account opening protection, anti-money laundering identification, and broader fraud decisioning across the customer lifecycle.

To make this comparison useful, we evaluated 6 platforms by the fraud problems they solve, the signals they use, and the workflows they fit best.

How We Evaluated the Top BioCatch Competitors

For comparing BioCatch competitors effectively, it's necessary to understand how each platform contributes across the fraud lifecycle.

Factors like whether it can connect behavioral signals with device intelligence, identity data, and transaction context to catch fraud early, adapt to evolving attack patterns, and support fast, confident decisions without disrupting genuine users should be considered.

To make the comparison practical, we evaluated every platform using the criteria below.

Behavioral biometrics: Analysis of typing rhythm, mouse movement, touchscreen gestures, device handling, and session behavior to distinguish genuine users from fraudsters.

Device intelligence: Detection of spoofed devices, emulators, VPNs, device resets, bots, browser manipulation, and repeat device usage.

Identity and account opening protection: Coverage for fake accounts, synthetic identities, mule accounts, and onboarding fraud.

Transaction and payment fraud coverage: Support for payment fraud, withdrawals, beneficiary changes, transfers, chargebacks, and suspicious fund movement.

AML and financial crime support: Capabilities for anti-money laundering identification, transaction monitoring, mule detection, audit trails, sanctions workflows, and investigations.

Real-time decisioning: Risk scoring across onboarding, login, account recovery, transactions, and ongoing activity.

Explainability: Clear risk signals and contextual explanations for flagged actions.

Workflow flexibility: Ability to configure rules, thresholds, step-up actions, and review workflows without heavy engineering effort.

Integration fit: APIs, SDKs, webhooks, and seamless integration into existing fraud, risk, and compliance stacks.

Bureau ID's 2026 India Fraud Report found that 58% of organizations identified decision errors as their dominant identity risk, highlighting why many buyers are moving beyond isolated behavioral signals toward platforms that evaluate identity, device, behavioral, and transaction intelligence together.

With these criteria in mind, compare leading BioCatch alternatives side by side to highlight where each platform stands and how they differ in real-world fraud prevention scenarios.

Top 6 BioCatch Competitors and Alternatives

The top BioCatch competitors include Bureau ID, SHIELD, LexisNexis ThreatMetrix, Feedzai, SEON, and Sift.

These BioCatch alternatives address different fraud prevention priorities, from behavioral biometrics and device intelligence to digital identity, account opening protection, transaction monitoring, AML risk, and unified fraud decisioning across the customer lifecycle.

Tool | Best For | Core Strength | Key Consideration |

Bureau ID | Unified fraud risk decisioning | Identity, device, behavior, network, and transaction intelligence | Best fit when teams want broader lifecycle coverage instead of point tools |

SHIELD | Device intelligence and multi-accounting prevention | Device fingerprinting, device risk, emulator detection, fake account detection | Strong when device manipulation, repeated signups, promo abuse, or multi-accounting are major fraud patterns |

LexisNexis ThreatMetrix | Digital identity intelligence | Device, identity, network, and risk signals | Better fit for enterprise risk stacks and digital identity use cases |

Feedzai | Enterprise fraud and financial crime prevention | Transaction fraud, scam detection, and risk operations | Best suited for large financial institutions and payment-heavy workflows |

SEON | Fraud checks and AML enrichment | Email, phone, IP, device, digital footprint, and AML signals | Strong when enrichment and fast fraud checks are the priority |

Sift | Digital fraud prevention | Account abuse, payment fraud, account takeover, and dispute workflows | Strong for marketplaces, ecommerce, subscription businesses, and digital platforms |

These six platforms were selected because they consistently appear across buyer research, analyst reports, review sites, and competitive searches for companies like BioCatch.

While some focus primarily on behavioral biometrics or device intelligence, others extend into digital identity, financial crime prevention, fraud orchestration, or broader anti-fraud solutions.

Below, we break down each BioCatch alternative by what it does, when buyers choose it, what to consider, best-fit use cases, and pricing expectations.

1. Bureau ID

Bureau ID is an AI-powered Unified Risk Decisioning Platform that helps businesses make fraud decisions across onboarding, authentication, transactions, and ongoing account activity. It brings multiple fraud signals together into a single decisioning layer to support more consistent and efficient risk decisions.

Bureau ID is used to protect businesses across the entire customer lifecycle, including onboarding, authentication, transactions, and ongoing account activity.

When buyers choose Bureau ID over BioCatch:

Organizations typically evaluate Bureau ID when behavioral biometrics alone is not enough to address the fraud challenges they face. Instead of focusing primarily on user behavior during a session, Bureau combines identity, device, behavioral, network, and transaction signals to deliver explainable risk decisions throughout the customer lifecycle.

Buyers commonly choose Bureau ID when they need to:

Protect onboarding, login, transactions, and ongoing account activity within one platform.

Detect synthetic identities, repeat devices, mule networks, and connected fraud rings using relationship-based intelligence.

Configure fraud workflows, approval rules, and step-up verification without extensive engineering effort.

Reduce fraud while minimizing false positives and unnecessary friction for legitimate users.

Key strengths:

Unified risk decisioning: Enables consistent fraud detection and decision-making across onboarding, authentication, transactions, and ongoing account activity.

Device intelligence and behavioral biometrics: Helps identify trusted and risky devices over time, even when fraudsters attempt to evade detection.

Graph identity network: Connects identities, devices, behaviors, and transactions to reveal coordinated fraud rings and mule networks that may not be visible through isolated signals.

Mule detection and AML support: Provides scoring and workflows that assist with identifying mule accounts and supporting financial crime investigations.

Explainable real-time decisions: Delivers transparent risk assessments that help analysts understand why users, devices, or transactions are flagged.

Configurable workflows: Allows teams to adapt fraud rules and decision logic using no-code and low-code tools, reducing reliance on engineering resources.

A good example of this broader approach comes from a leading insurer that improved onboarding efficiency while reducing fraudulent applications.

How Bureau ID helped a leading insurer improve onboarding and reduce fraud

A leading insurer was facing high levels of fraudulent applications during onboarding, which forced them to introduce stricter checks that slowed down legitimate customers. They needed a way to balance fraud prevention with a smoother onboarding experience.

Bureau ID helped by combining identity verification with device and behavioral intelligence within a unified decisioning workflow, allowing the insurer to detect risky applications more accurately while reducing friction for genuine users.

Results achieved:

30% faster onboarding for legitimate customers

Significant reduction in fraudulent applications

Improved approval rates without increasing risk

Read the full case study here → Insurer Cuts Fraud for 30% Faster Onboarding

Things to consider:

Designed for organizations consolidating fraud prevention across onboarding, authentication, transactions, and ongoing account activity rather than deploying a standalone behavioral biometrics solution.

Delivers the most value when buyers clearly map the workflows they want to unify across the customer journey before implementation.

Pricing: Platform-based custom pricing based on modules, use cases, and transaction volume.

2. SHIELD

SHIELD is a device-first fraud intelligence platform that helps businesses identify risky devices before fraud occurs. It specializes in persistent device identification, fake account detection, multi-accounting prevention, and bot mitigation, making it a strong BioCatch alternative for organizations that want deeper device intelligence across mobile and web environments.

When buyers choose SHIELD over BioCatch:

Organizations often evaluate SHIELD when device manipulation is a larger fraud challenge than session behavior alone. Buyers commonly choose SHIELD when they need to:

Detect fake accounts, repeat devices, and multi-accounting before they impact onboarding or promotions.

Identify fraudsters using emulators, cloned apps, VPNs, factory resets, or other device evasion techniques.

Reduce promo abuse, referral fraud, and bot-driven attacks through device-level intelligence.

Key strengths:

Stops fraud before accounts are created: Persistent device identification helps expose risky devices before onboarding, payments, or KYC checks are completed.

Detects sophisticated device manipulation: Identifies emulators, cloned apps, device tampering, VPN usage, and other techniques commonly used to evade detection.

Reduces multi-account abuse: Connects repeat devices across accounts to uncover referral abuse, fake accounts, and coordinated fraud activity.

Supports real-time fraud decisions: Delivers device risk signals with low latency so teams can act during onboarding, login, or payment flows.

Integrates quickly across digital channels: SDKs and APIs support deployment across web, Android, iOS, and other environments with centralized monitoring.

Things to consider:

Organizations may still require complementary solutions for identity verification, AML workflows, transaction monitoring, or broader fraud orchestration.

Some reviewers note that advanced integrations and custom configurations can require technical expertise, particularly for teams without dedicated engineering resources.

Pricing: Custom pricing based on use case, deployment scope, and transaction volume.

3. LexisNexis ThreatMetrix

LexisNexis ThreatMetrix is a digital identity intelligence platform that helps businesses assess trust using device, identity, network, and behavioral signals. It is a strong BioCatch alternative for organizations that need broader digital identity intelligence and enterprise-scale fraud prevention beyond behavioral biometrics alone.

When buyers choose LexisNexis ThreatMetrix over BioCatch:

Organizations typically evaluate ThreatMetrix when fraud decisions require more than session-level behavioral analysis. Buyers commonly choose the platform when they need to:

Build richer risk profiles using device, identity, location, and network intelligence.

Protect account opening, authentication, and payment journeys with connected digital identity signals.

Leverage enterprise-grade fraud intelligence across multiple business units or regions.

Key strengths:

Builds trusted digital identities: Connects identity, device, location, and network signals to evaluate user trust throughout the customer lifecycle.

Improves account opening protection: Detects suspicious identities and high-risk onboarding attempts before accounts are created.

Strengthens account takeover detection: Combines device reputation and behavioral risk signals to identify anomalous login activity.

Supports enterprise fraud operations: Integrates with large-scale fraud, compliance, and authentication ecosystems across financial institutions.

Enables cross-channel risk decisions: Applies consistent risk intelligence across web, mobile, and digital banking experiences.

Things to consider:

ThreatMetrix is designed primarily for enterprise organizations, so implementation effort and operational complexity may exceed the needs of smaller businesses.

Implementation and integration can require significant planning, particularly in complex enterprise environments.

Pricing: Enterprise custom pricing.

4. Feedzai

Feedzai is an enterprise financial crime prevention platform that helps banks and payment providers detect fraud across payments, transfers, and digital banking. It is a strong BioCatch alternative for organizations that prioritize transaction monitoring, scam detection, and AML workflows alongside fraud prevention.

When buyers choose Feedzai over BioCatch:

Organizations often evaluate Feedzai when fraud is concentrated around money movement rather than user sessions. Buyers commonly choose Feedzai when they need to:

Detect payment fraud, scams, and suspicious transactions in real time.

Combine fraud prevention with AML monitoring and financial crime investigations.

Support large-scale fraud operations across banking and payment ecosystems.

Key strengths:

Detects payment fraud in real time: Uses AI and machine learning to identify suspicious transactions before funds leave the institution.

Strengthens financial crime operations: Combines fraud detection with AML monitoring, scam prevention, and investigation workflows.

Supports enterprise-scale decisioning: Processes high transaction volumes across banks, payment processors, and financial institutions.

Improves analyst efficiency: Provides case management and investigation tools that help fraud teams prioritize high-risk events.

Adapts to evolving fraud patterns: Machine learning models continuously evaluate new fraud behaviors instead of relying solely on static rules.

Things to consider:

Feedzai is designed primarily for enterprise financial institutions, so it may offer more functionality than smaller fintechs or digital businesses require.

Implementation can be time-consuming because the platform requires careful model configuration and integration with existing banking systems.

Pricing: Enterprise custom pricing.

5. SEON

SEON is a fraud prevention platform that combines digital footprint analysis, device intelligence, identity enrichment, and AML capabilities to assess user risk. It is a strong BioCatch alternative for organizations looking for fast fraud screening across onboarding, payments, and account activity without relying primarily on behavioral biometrics.

When buyers choose SEON over BioCatch:

Organizations often evaluate SEON when they want broader identity enrichment alongside fraud detection. Buyers commonly choose SEON when they need to:

Verify users using email, phone, IP, device, and digital footprint intelligence.

Add AML screening and fraud scoring within the same workflow.

Deploy flexible fraud checks across fintech, ecommerce, gaming, crypto, or marketplace platforms.

Key strengths:

Enriches user profiles instantly: Combines email, phone, IP, device, and digital footprint signals to build a more complete risk profile.

Reduces onboarding fraud: Identifies suspicious accounts before they progress through verification or payment flows.

Supports AML and compliance workflows: Integrates AML screening alongside fraud scoring to simplify risk assessments.

Provides flexible risk controls: Enables teams to configure fraud rules, risk thresholds, and decision logic without extensive development work.

Deploys quickly across digital channels: API-first architecture helps businesses integrate fraud checks into existing customer journeys with minimal disruption.

Things to consider:

SEON focuses on enrichment and fraud intelligence rather than dedicated behavioral biometrics, so organizations with advanced session-level fraud requirements may need complementary technologies.

Some users note that investigation workflows would benefit from stronger case management capabilities.

Pricing: Usage-based pricing with custom enterprise plans available.

6. Sift

Sift is a digital fraud prevention platform that helps businesses detect account abuse, payment fraud, account takeover, and policy abuse across the customer lifecycle. It is a strong BioCatch alternative for marketplaces, ecommerce companies, and subscription businesses that need fraud protection beyond behavioral biometrics.

When buyers choose Sift over BioCatch:

Organizations often evaluate Sift when fraud extends beyond authentication into payments, disputes, and account abuse. Buyers commonly choose Sift when they need to:

Detect account takeover, fake accounts, and payment fraud from a unified platform.

Protect marketplaces, subscription businesses, and digital communities from policy abuse and chargebacks.

Connect fraud decisions across user behavior, account activity, and transaction risk.

Key strengths:

Protects the entire customer journey: Helps detect fraud across onboarding, account activity, payments, disputes, and trust and safety workflows.

Reduces account abuse: Identifies fake accounts, account takeover attempts, promo abuse, and other forms of platform abuse before they scale.

Improves payment fraud detection: Combines machine learning with behavioral and transaction signals to identify high-risk payments in real time.

Supports trust and safety teams: Provides case management, automation, and investigation tools for fraud operations at scale.

Integrates into growing digital platforms: Flexible APIs enable deployment across marketplaces, ecommerce, subscription services, and online communities.

Things to consider:

Sift is designed as a broad digital fraud prevention platform rather than a dedicated behavioral biometrics solution, so organizations requiring deep behavioral analytics may need complementary capabilities.

Some reviewers mention that investigation workflows could be improved with stronger case management capabilities, such as note-taking and grouping related device activity for complex fraud investigations.

Pricing: Custom pricing based on business size, use case, and transaction volume.

Which BioCatch Alternative Is Right for Your Use Case?

The best BioCatch alternative depends on where fraud occurs in your customer journey. For instance:

A bank dealing with account takeover and scam activity may prioritize behavioral biometrics and digital identity intelligence.

A fintech fighting synthetic identities and mule accounts may need stronger identity, device, and network intelligence.

Meanwhile, ecommerce businesses and marketplaces often focus on account abuse, payment fraud, promo abuse, and chargebacks.

According to the INTERPOL 2026 Global Financial Fraud Threat Assessment, AI-enhanced financial fraud is now 4.5 times more profitable than traditional methods, and financial fraud has entered the top 5 global crime threats.

Before shortlisting a platform, take a quick, structured approach to understand your needs and avoid mismatches.

Map where fraud occurs across your lifecycle, from onboarding and login to transactions, withdrawals, and ongoing monitoring.

Identify the key signal gap you need to address, such as behavioral, device, identity, transaction, AML, network, or workflow intelligence.

Evaluate operational fit, including explainability, case management, rules, step-up flows, and implementation complexity.

Test each platform against your real fraud scenarios, false positives, and genuine user behavior before making a decision.

BioCatch Alternatives by Use Case

Use Case or Priority | Best-Fit Tools |

Need unified risk decisioning across onboarding, login, transactions, and monitoring | Bureau ID, LexisNexis ThreatMetrix, Feedzai |

Need behavioral biometrics and session-level fraud detection | Bureau ID, LexisNexis ThreatMetrix |

Need device intelligence, repeat device detection, and multi-accounting protection | Bureau ID, SHIELD, SEON |

Need account opening protection and synthetic identity detection | Bureau ID, LexisNexis ThreatMetrix, SEON |

Need transaction fraud, scam detection, and financial crime workflows | Feedzai, Bureau ID, LexisNexis ThreatMetrix |

Need enrichment-led fraud checks across email, phone, IP, and device | SEON, Sift |

Need account abuse, payment fraud, and marketplace or ecommerce fraud protection | Sift, SEON, Bureau ID |

Need AML-adjacent signals, mule risk, and compliance-heavy review support | Bureau ID, Feedzai, SEON |

For many of Bureau ID's core customers, fraud is rarely confined to a single event. Banks, fintechs, lenders, marketplaces, gaming companies, payment providers, and ecommerce platforms often need to evaluate trust across multiple stages of the customer journey rather than at a single checkpoint.

Bureau ID is a strong fit for organizations that want to combine device intelligence, behavioral biometrics, identity verification, network intelligence, transaction monitoring, and configurable fraud workflows within a unified risk decisioning platform instead of managing separate point solutions.

Stop Fraud Across the Entire Customer Journey

The right BioCatch alternative is the one that aligns with where fraud occurs in your business.

If your biggest challenge is session-level fraud, a behavioral biometrics platform may be enough. But if fraud spans onboarding, authentication, account activity, transactions, mule networks, and manual review, a broader risk decisioning platform can provide better visibility and more consistent decisions.

Bureau ID brings identity, device, behavioral, network, and transaction intelligence together into a single decisioning layer, helping fraud, risk, compliance, and product teams detect connected fraud, reduce false positives, and protect the entire customer journey.

If you're curious how unified risk decisioning can strengthen your fraud prevention, onboarding, compliance, and transaction monitoring workflows, schedule a demo with Bureau ID today.

FAQs

1. Who are BioCatch's biggest competitors?

Some of the top BioCatch competitors include Bureau ID, SHIELD, LexisNexis ThreatMetrix, Feedzai, SEON, and Sift. Each platform focuses on different strengths, such as behavioral biometrics, device intelligence, digital identity, transaction monitoring, or unified fraud risk decisioning.

2. What is the best BioCatch alternative for banks and fintechs?

The best alternative depends on your fraud challenges. Banks and fintechs focused on account takeover may prioritize behavioral biometrics, while organizations dealing with onboarding fraud, mule accounts, and transaction risk often need broader platforms combining identity, device, network, and transaction intelligence.

3. How does Bureau ID compare to BioCatch?

Bureau ID and BioCatch both help detect fraud using behavioral signals, but Bureau ID extends beyond behavioral biometrics by combining identity, device, network, and transaction intelligence. This makes it well-suited for organizations seeking a more unified approach to fraud risk decisioning across the entire customer journey.

4. What should I compare when evaluating BioCatch alternatives?

Look beyond behavioral biometrics. Compare device intelligence, identity verification, account opening protection, transaction monitoring, AML capabilities, explainability, workflow flexibility, integrations, and how effectively each platform supports your fraud operations from onboarding through ongoing account activity.

5. Which BioCatch alternative is best for preventing account takeover?

If account takeover is primarily driven by abnormal user behavior, behavioral biometrics platforms may be sufficient. If attackers also exploit stolen devices, synthetic identities, or mule accounts, consider platforms that combine behavioral, device, identity, and transaction intelligence.

6. How do I choose the right BioCatch alternative for my business?

Start by identifying where fraud occurs in your customer journey and the signals you need to detect it. Then evaluate each platform using your own fraud scenarios, operational workflows, integration requirements, and false-positive tolerance before making a decision.

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.